.png)

The first thing the lender will do when the appraisal is received is determine the property’s “value” for LTV purposes. This is not as simple as just using the number printed at the top of the appraisal – it can in fact be different. DSCR Lenders apply specific rules for determining value depending on whether the loan is for a purchase or a refinance, the type of property and recent ownership history.

For acquisitions, DSCR Lenders will calculate LTV using the lower of purchase price and appraisal as-is market value.

At first glance, it’s tempting to assume the purchase price is the best measure of a property’s value, after all, it’s the number a willing buyer and seller agreed on. But in DSCR lending, that assumption can be risky. Individual transactions can be shaped by unique motivations, relationships or tactics that don’t reflect a broadly supportable market value. To protect against these risks, lenders use the lower of purchase price or appraised value when calculating LTV.

This safeguard addresses several things that could prevent purchase price from being an accurate equivalent to market value. One example is emotional overbids, as some buyers are willing to pay more than market value simply to win a competitive bidding war, secure a dream property or outmaneuver other investors in pressure-filled situations, letting feelings overcome facts. While that premium might be acceptable to the buyer, it doesn’t add to the resale value the lender could achieve if they had to take the property back. In addition, some purchases involve strategic overpays, or when an investor may knowingly pay above market because the property creates synergy with an existing portfolio, such as owning both sides of a duplex, consolidating neighboring parcels or controlling a specific rental market segment. Those advantages are real for the buyer but have no extra value to the lender or to the general market, which is a DSCR Lender’s primary concern when thinking about value (how much they would be able to sell it to the market if needed after foreclosure), not wanting to “count on” lightning striking twice, and finding another buyer willing to overpay for specific, strategic reasons.

Additionally, DSCR Lenders are always on the lookout for Non-Arm’s-Length & Inflated-Value Transactions. Deals between related parties, business partners, or entities under common ownership, as well as distressed sales or deliberately inflated contracts — often fail to reflect true market competition. In some cases, buyer and seller may even collude to overstate the sales price to qualify for a larger loan and pull out excess cash. Using the lower of purchase price or appraised value is a fraud prevention measure that helps ensure the lender isn’t lending against an artificially high number, whether the distortion is intentional or simply the result of off-market motivations.

The result is a more conservative valuation methodology that protects the DSCR Lender and eventual note holder against potential fraud or inflated prices. However, it's important to note that in practice, the vast majority of appraisal values for DSCR Loan acquisition transactions will be equivalent to purchase price or very close (within 5%), making valuation issues for DSCR Loans for acquisitions a relative rarity.

Refinances, especially cash-out refinances, are viewed through a different lens by DSCR Lenders because there’s no live-market transaction to validate the property’s value. In a purchase, the contract price serves as a second opinion alongside the appraiser’s estimate. In a refinance, the lender is relying entirely on a single appraiser’s opinion, which is inherently more subjective and potentially more volatile. That extra uncertainty is why lenders apply additional restrictions and safeguards around valuation for refinance DSCR Loans, particularly when the property has been owned for less than a year. They are protecting against both fraud risk and valuation uncertainty due to the absence of an ongoing market transaction.

The intensity of these restrictions is typically much higher for cash-out refinances than for rate-term refinances. From the lender’s perspective, a rate-term refinance, where no equity is being pulled out, carries far less incentive for fraudulent behavior. Fraudsters aren’t generally interested in refinancing into the same or similar loan amount if it doesn’t generate cash in their pocket. Cash-out refinances, on the other hand, create the possibility of extracting large sums of equity based solely on an inflated appraisal, making them far more attractive to bad actors.

There’s also a behavioral and risk-based reason lenders treat cash-out refinances more conservatively: borrower commitment. Investors who have significant capital left in a property, i.e. “skin in the game”, are generally more motivated to keep the property performing, stay current on payments, and weather temporary downturns in rental income. Conversely, after a large cash-out event, an investor may be operating with “house money” and have less personal financial stake in protecting the asset. For the DSCR Lender, that translates into higher default probability in a stress scenario, so they offset that risk with tighter LTV limits and seasoning requirements specifically on cash-out transactions.

A key factor for the valuation utilized by DSCR Lenders on refinance transactions is the concept of seasoning, which in the context of DSCR Loans refers to how long (typically expressed in months) the investor (borrower) has owned the property. Seasoning requirements are utilized for both fraud-prevention (fraudsters will want to move quickly on cash-out refis as more time waiting gives the lender more time to uncover any funny business) and for the psychological commitment variable that makes a difference (investors with skin in the game only for a few months on a property can be more likely to walk away quicker when times get tough).

While the vast majority of DSCR Lenders only have seasoning valuation rules around cash-out refinances and not rate-term refinances, in recent years a handful of DSCR Lenders have also implemented seasoning restrictions on rate-term refinances as well, likely due to the uncertainty caused by the low-transaction volume housing market in the mid-2020s, making value determinations harder in general. Simply, with far fewer sales transactions happening, there are fewer and less robust “comps” for appraisers, and less precise value estimates.

Q: What does “seasoning” mean for a DSCR Loan?

A: In DSCR lending, seasoning is how long a borrower has owned a property, usually measured in months. DSCR loan seasoning is most often used to set valuation rules for refinances, especially cash-out refinances, but also applies to timelines for credit events or mortgage lates before they stop impacting eligibility. In short, it’s the aging period until certain restrictions expire.

So how do seasoning rules work for DSCR Loan cash-out refinances? This is another area where there is significant diversity among DSCR Lenders in valuation methodology for cash-out refinances, however generally the rules are based on different seasoning “buckets” or ranges as follows:

Universally among DSCR Lenders, valuation is based simply on the appraised market value for cash-out refinance transactions with seasoning greater than 12 months (owned for a full year or more). Once you’ve reached a full year of ownership, the appraised value will be the value utilized for calculating the LTV on the DSCR Loan (excepting rare situations such as CDA variances >10% or large loan amounts (i.e. >$2M) requiring the lower of two appraised values.

While in the past (late 2010s and early 2020s) a lot of DSCR Lenders carried seasoning requirements for properties owned greater than six months but not yet a full year of ownership, many DSCR Lenders have relaxed or abandoned seasoning requirements for this range in recent years (2023-2025). The reasons for this are likely to become more competitive for a limited range of deals (challenging market) and also potentially a response to a 2023 update from Fannie Mae that essentially banned cash-out refinances for conventional loans with under 12 months seasoning, giving DSCR Lenders a competitive opportunity for these specific seasoning scenarios.

While some DSCR Lenders still have seasoning requirements in this range, DSCR Loans industry standard has transitioned to no seasoning restrictions for refinances with 6-12 months ownership and will also simply use the appraised market value for the LTV ratio calculation.

Some more conservative DSCR lender holdouts however will implement the traditional refinance valuation restriction for short-seasoned properties for this seasoning time range. This valuation methodology is typically referred to as “purchase price + documented improvements” where the valuation is the lower of appraised value and purchase price + documented improvements, or the original purchase price plus the documented costs of any renovations post-purchase. This can also be referred to as the investors “cost basis” in the property. Because the vast majority (and whole reason behind) real estate investors buying and renovating a property is to create value above the cost of the project (typically referred to in the industry as “forced appreciation”), the valuation under this methodology would typically be the purchase price + documented improvements, as cost basis would be presumably lower than the new appraised market value.

Q: What counts as documented improvements for a DSCR Loan?

A: For DSCR loans, “documented improvements” generally include most applicable renovation costs, both materials and labor, that add value to the property. Lenders’ requirements are often fairly flexible: you typically don’t need detailed receipts or work orders for every item, but should provide a clear, organized record that appears reasonable for the scope of work. If the amounts line up with market costs and the appraisal photos clearly show the completed upgrades, underwriting will usually accept them without issue.

Of course, many real estate investors, especially investors focused on the BRRRR Method, put maximizing leverage as the centerpiece of their real estate returns strategy, and if LTV calculation (and thus max loan amount) is determined by the conservative cost basis figure instead of the enhanced market value (appraised value), this can severely impair returns and activity. However, the good news is that there are plenty of DSCR Lenders in the current environment that will use the appraised value to calculate LTV with seasoning greater than six months, so BRRRR investors can find solid DSCR Loan options.

Q: What is forced appreciation in real estate investing?

A: Forced appreciation is the increase in a property’s market value that exceeds the cost of improvements, i.e., when the value added by renovations/repairs is greater than what you spent to do them. In simple terms: if value rises by $60,000 and you spent $35,000 on rehab, you created $25,000 of forced appreciation.

Q: What is cost basis in real estate investing?A: In real estate investing, cost basis represents the total capital invested in acquiring and improving a property, combining the purchase price with renovation costs, or simply “how much you’ve invested in the property.”

This seasoning range, properties owned between three months and six months, is where the most DSCR Loan cash-out refinance seasoning requirements come into play. This is because the ownership period is short enough to trigger lender concerns over potential fraud and investor psychology, in addition to the inherent refinance valuation uncertainty with no market transaction occurring. It also is a frequently important range because many real estate investors that use a renovation or forced appreciation-based investing strategy (buying properties in need of rehab and renovating to either flip “fix and flip” or refinance “BRRRR method”), have renovation project timeline plans of a few months, generally in this same range (3-6 months). Many investors utilize high-interest rate hard money loans (with rates typically in double digits), so they are eager to refinance as quickly as possible, as each month can bring a high interest cost that takes a big bite out of returns.

The three to six month seasoning range sits at the confluence of these factors and is where the DSCR Loan seasoning requirements are typically implemented, with the industry standard in 2025 to still use the lower of appraised value and purchase price + documented improvements (cost basis) as the “official” value (i.e. used for LTV) for cash-out refinances with seasoning between 3-6 months.

However, some DSCR Lenders, especially those that target the BRRRR investor niche, have relaxed seasoning requirements for this refinance range (3-6 months). These lenders will offer cash-out refinance DSCR loans with 3-6 months seasoning using the appraised market value for the LTV calculation with some restrictions such as higher minimum qualifying credit scores and some limits on loan amount and LTV.

Restrictions for DSCR Lenders that offer this typically include:

Typically, if all of these factors are satisfied, certain BRRRR-friendly DSCR Lenders will allow cash-out refinances with short seasoning (or seasoning between three and six months).

Note, that for these “short-seasoned” cash-out refinance DSCR Loans, it’s important to understand how these factors all would have to be satisfied, so for example if the property was bought for $100,000 and renovation costs were $30,000 (total cost basis of $100,000 + $30,000 = $130,000) and the appraised value was $200,000 (for forced appreciation of $70,000), then a borrower (with a credit score over 720) might be capped at a LTV of 65.0% instead of 70.0% because the maximum loan amount would be $130,000, or the cost basis, which results in a 65.0% LTV ($130,000 / $200,000 = 65%) which overrides the program maximum LTV of 70.0%. Note that DSCR Lenders vary significantly in their rules and restrictions around short-seasoned cash-out refinances so it’s imperative to know how all the rules work specifically for a particular lender, the above is just an illustrative example of what it might look like.

Some real estate investors can be interested in an ultra-quick cash-out refinance DSCR Loan, or a refinance with less than three months seasoning. Generally, refinances with less than 3 months seasoning are ineligible for DSCR Loans. The reasoning from lenders is the same as for all the refinance valuation concerns we’ve discussed, but supercharged, especially around fraud risk. Refinancing with this speed is typically a large and blaring red flag for DSCR Loans.

Sometimes, especially in situations where an investor that is forced to buy a turnkey rental property or light fixer upper with all cash in order to win the deal but would prefer to use financing, an investor wants to close the purchase first (without the standard DSCR loan cycle that typically takes at least three weeks), and then “refinance” the property by adding debt as soon as possible after gaining ownership of the asset. These cases are sometimes referred to as “Delayed Financing” DSCR Loans in which the loans are functionally more like acquisitions, as the loan is closed slightly after the purchase (instead of at the same time), than true cash-out refinances.

There has unfortunately been a lot of confusion around the topic of Delayed Financing and DSCR Loans. While some investors have become excited at the opportunity for the handful of DSCR Lenders that allow delayed financing, or refinances with less than three months seasoning, the reality is pretty misleading. In these cases, the loan is still treated as a cash-out refinance, not an acquisition – meaning the LTV restrictions (typically 5% or even 10% lower than maximum for acquisitions) and pricing (somewhat higher interest rates and/or closing fees) for cash-out refinances are still applied. Additionally, the valuation would always be limited to purchase price for cash-out refinances (not even purchase price plus documented improvements), and the appraised value only used if it somehow comes in lower than acquisition cost. Bottom line, even if eligible, DSCR Loans for Delayed Financing don’t really provide investors much benefit since they are treated by almost all DSCR Lenders that do them as cash-out refinances with maximum seasoning restrictions around value.

Q: How does delayed financing work for DSCR Loans?

A: In DSCR lending, delayed financing is when an investor buys a property with cash and then quickly refinances to add debt, often within weeks of purchase. Even if a lender allows it with less than three months of ownership, the loan is still treated as a cash-out refinance, not a purchase, which means lower maximum LTVs, higher rates or fees, and value limited to the purchase price (or the appraised value if it’s lower). For most investors, this makes delayed financing in DSCR loans far less advantageous than it might sound.

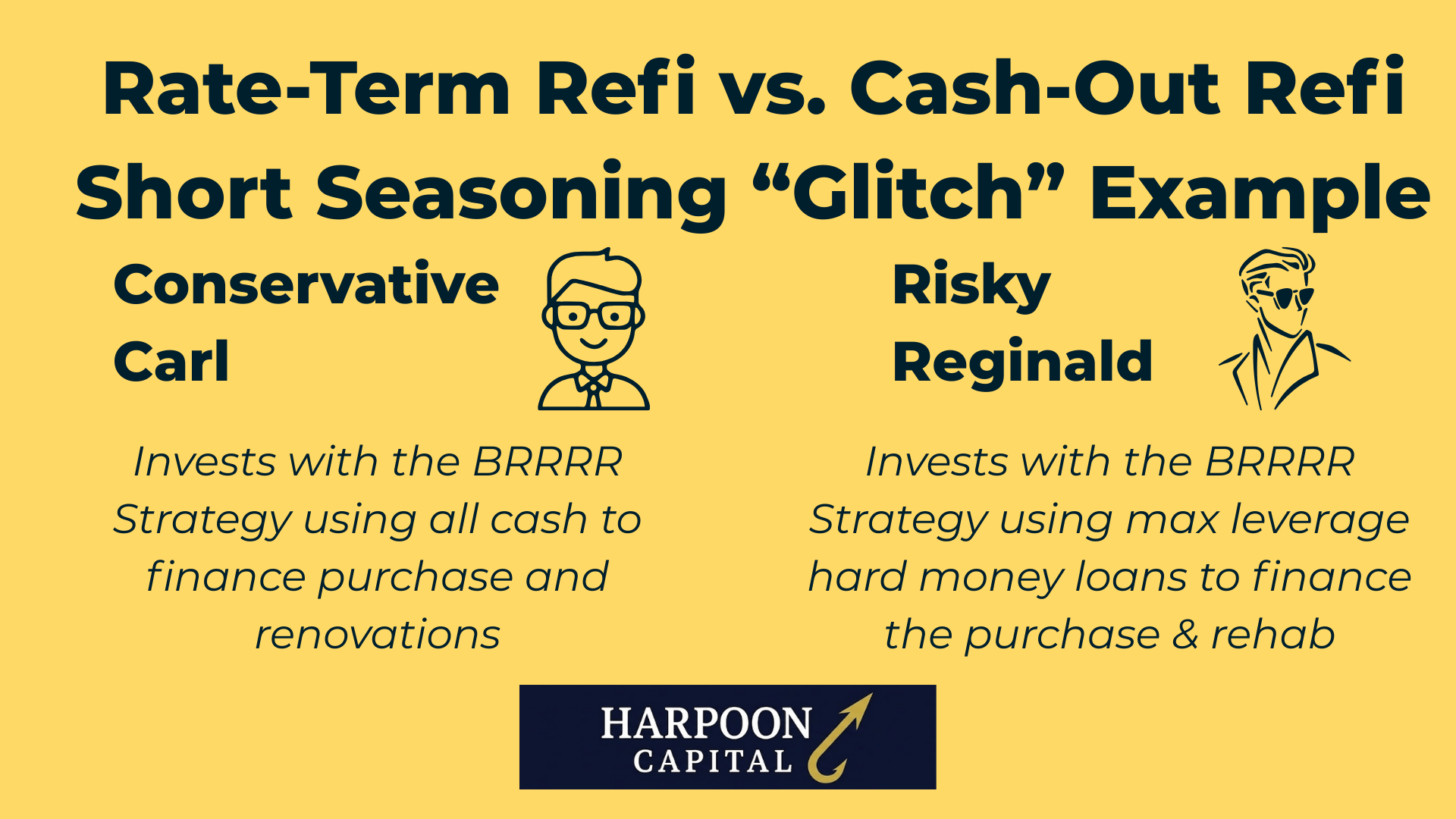

While the vast majority of DSCR Lenders only have seasoning valuation rules around cash-out refinances and not rate-term refinances, in recent years a handful of lenders have begun to apply seasoning rules and restrictions to short-seasoned rate-term refinances too. While the same fraud and borrower psychology risks don’t appear to apply if no cash is being taken out by the borrower, and thus why traditionally there have been no seasoning restrictions on rate and term refis, there is some solid reasoning behind this recent lender adaptation as some investors have noticed a “glitch” in typical DSCR underwriting guidelines in this area. These investors realized they could get maximum leverages and lightning speed refinances for BRRRR deals as long as no cash-out occurred, such as getting 80.0% LTVs DSCR Loans within only a few months of ownership.

For the BRRRR strategy (Buy -> Rehab -> Rent -> Refinance -> Repeat), investors can choose to finance the first two steps (i.e. the purchase price and renovation costs) either with their own cash or choose to use a hard money loan. To illustrate these two choices, let’s look at an example for two investors pursuing the BRRRR method on a fixer-upper property, one, Conservative Carl, utilizing cash on hand and avoiding high-priced hard money, and two Risky Reginald, taking out a hard money loan with max leverage to minimize cash down.

In this example, investor one, Conservative Carl, buys a $100,000 distressed property in need of a $50,000 of renovations and finances the entire purchase and renovation with his own cash ($150,000). He completes the rehab in four months, with the newly rejuvenated property appraised at a market value of $200,000. With most DSCR Lenders, in order to do the refinance at the four-month mark (when property is fully rehabbed), Carl would only be eligible for a cash-out refinance likely maxed at 75.0% of cost basis of the $150,000 that he spent, meaning his new DSCR Loan would be capped at only $112,500 (75% * $150,000) and carry the least favorable pricing and terms since the loan purpose is cash-out refinance.

Alternatively, he could wait an extra two months to refinance to hit the six-month seasoning mark, delaying access to that precious capital to start his next project. Even if he was working with a “BRRRR-friendly” DSCR Lender that allows cash-out refinances with values based on appraisal-determined market value with seasoning less than six months, he would still likely be limited to a $130,000 loan amount (70.0% LTV) and the somewhat elevated interest rate that comes with cash-out refinances (also assuming he has the credit score to qualify).

Now, however let’s look at investor two, Risky Reginald who buys an exactly similar $100,000 distressed property in need of $50,000 in renovations, but instead of funding the purchase and renovation with his cash, he takes out a hard money loan at aggressively risky leverage, 95.0% LTC or “loan-to-cost” ratio. Note: a LTC ratio is a term used in hard money lending (similar to LTV in DSCR lending) that represents the total loan amount in relation to the cost of the project (purchase price plus renovation budget). So, in this case, Reginald is taking a loan of $142,500 (95% * $150,000) to finance this project and he is only required to put a paltry $7,500 of his own cash “down” or into the purchase and rehab. Assuming the project has similar results, i.e. the renovation is finished in four months and the rehab yielded an appraised market value of $200,000, then Reginald, carrying a loan balance of $142,500 and with little “skin in the game” somehow has a much better set of DSCR Loan refinance options awaiting him!

Almost all DSCR Lenders will allow rate-term refinances up to 80.0% LTV and with no seasoning restrictions, so a rate-term refinance loan would theoretically be immediately available to Reginald at up to $160,000 loan amount (80% * $200,000) with no seasoning or elevated credit requirements to worry about. Note that technically, in this example, since to be a rate-term refinance, it needs less than $2,000 cash back to the borrower, his loan would likely be limited at around $150,000 (assuming at least $5,500 in closing costs and escrows to get the total amount subtracted from the new loan at the closing table to $148,000 ($142,500 + $5,500). However, the loan’s LTV would still be calculated based on appraised value (so would be 75.0%) and he would also get better pricing (lower rate/fees) since the loan purpose is rate-term refinance, not cash-out.

So, in summary, Conservative Carl who uses all cash to fund his purchase and rehab faces strict LTV restrictions, lower potential loan amounts and higher rates than Risky Reginald, who maxed leverage to the gills (only $7,500 cash used, versus $150,000 or 20x more by Carl), faces no seasoning restrictions and qualifies for a higher LTV, higher loan amount and even gets better rates and terms! This can be described as a “glitch” because the DSCR Loan refinance rules are rewarding a higher-risk borrower with better rates and terms, higher leverage options and no seasoning rules – the exact opposite of how it should be!

Unfortunately, as with many good things, savvy strategies can attract unscrupulous fraudsters who realized this “glitch” in underwriting methodology. Some have adjusted their unsavory schemes to take advantage of less lender scrutiny if the deals could be reworked to be “rate-term refinances.” A few DSCR Lenders have taken note of the potential fraud risk here, and also maybe just the illogic of these particular rules. So, in response, these DSCR Lenders have now put the same seasoning rules on rate-term refinances and cash-out refinances. However, as of 2026, there are still a sizable amount of DSCR Lenders that allow investors who max leverage their BRRRR transactions to take advantage of this pricing and eligibility “glitch.”

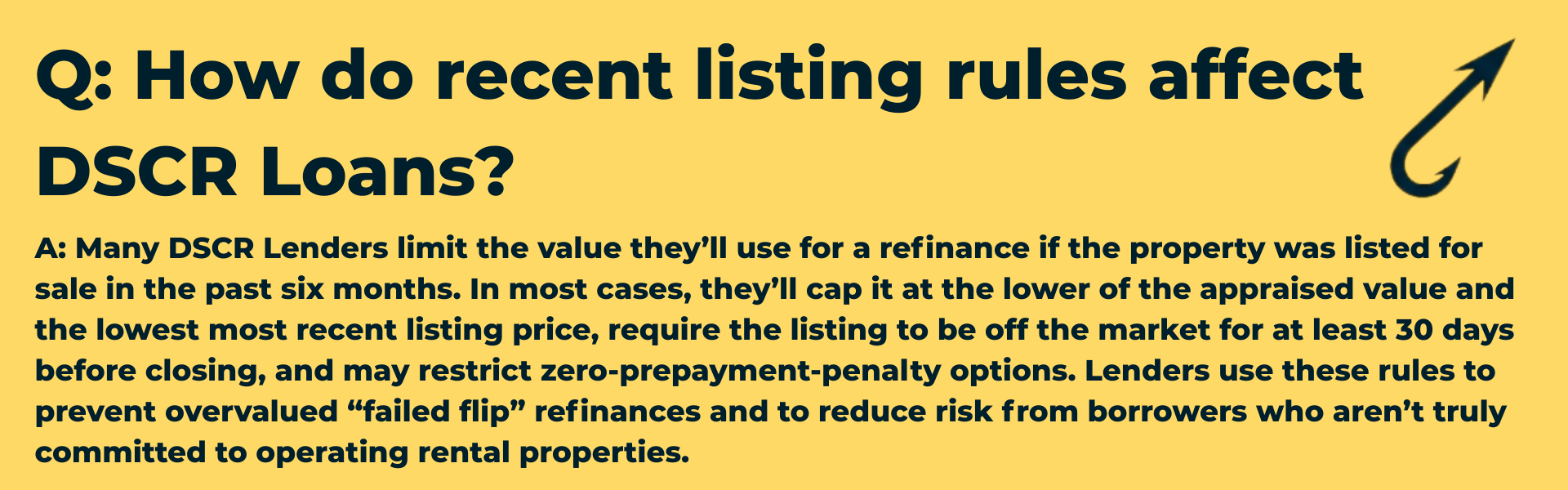

If a property was recently listed for sale and then taken off the market, many DSCR Lenders will cap the valuation at the lower of the appraised value and the most recent minimum listing price, unless the listing was removed well before the refinance application.

The logic behind this is straightforward: if a property was actively listed at a certain price and did not sell, its market value cannot reasonably be considered higher than that list price. In a competitive, transparent market, a truly willing buyer would have purchased it if it were in fact worth more, despite the appraiser’s opinion. Typically, lenders apply this restriction to any property listed within the past six months before the refinance, and they often require the listing to have been withdrawn for at least 30 days before the closing date as well. This ensures there’s a clear break between the failed sale effort and the refinance closing.

Some DSCR Lenders also extend their concerns beyond valuation. They may prohibit zero prepayment penalty options on DSCR Loans for properties that were recently listed and then pulled from the market. This is likely to make sure that proper protections are in place for the DSCR Lender if the borrower goes right back to selling the property post-refinance and was only using the DSCR Loan to buy time.

Beyond the pure valuation logic, many DSCR Lenders see recent listings as a possible sign of a “failed flip” — where selling the property was the owner’s original goal, but after not finding a buyer, they pivot to a refinance (often under a BRRRR-type plan B). From the DSCR Lender’s perspective, borrowers in these situations can be riskier, they may not be experienced landlords or prepared for long-term property management. They also may lack the systems or resilience to handle vacancies, repairs, or tenant issues over time. There is also a likely concern that psychologically, their underlying intent wasn’t to operate the property as an income-producing asset, meaning there’s more uncertainty about their commitment to the investment. And finally, there is the fraud risk that most DSCR Lenders are always on the lookout for, wanting to make sure that a DSCR Loan is not just being used to “buy time” to continue to attempt to sell the property.

For these reasons, recent listing rules act as both a valuation safeguard and a borrower quality filter, protecting lenders from overvalued collateral and from borrowers who may be less committed to the property’s ongoing performance and more likely to default or cause servicing headaches.

Q: How do recent listing rules affect DSCR Loans?

A: Many DSCR Lenders limit the value they’ll use for a refinance if the property was listed for sale in the past six months. In most cases, they’ll cap it at the lower of the appraised value and the lowest most recent listing price, require the listing to be off the market for at least 30 days before closing, and may restrict zero-prepayment-penalty options. Lenders use these rules to prevent overvalued “failed flip” refinances and to reduce risk from borrowers who aren’t truly committed to operating rental properties.

Up Next: How DSCR Lenders Calculate the Revenue Number (Numerator) DSCR Ratio in Final Underwriting

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.