.png)

The DSCR ratio in many cases can only be finalized once the appraisal comes in. While the DSCR ratio formula is fairly simple for DSCR Loans (DSCR = Rental Revenue ÷ PITIA), getting and confirming the final numbers that go into each spot in the equation can be complex and come from a variety of sources. Further, different DSCR Lenders can have different rules and methodologies for the all-important numerator in the equation (i.e. the revenue portion of the formula) and the number may not just come from one source document, but a combination of multiple docs that arrive at different stages of the loan process. However, once the appraisal has arrived, and unless the borrower has been tardy on the needs list or delays have occurred from third party vendors, all the data should be available to arrive at a final DSCR number.

One somewhat fair criticism sometimes lobbed at DSCR Loans is the looseness or relatively aggressive underwriting of the rental revenue of the properties secured by these mortgage loans. This means that the revenue number utilized by DSCR Lenders in general tends to be pretty optimistic (i.e. on the higher end of what’s likely to manifest) and much less “conservative” than revenue projections used by most commercial real estate lenders or conventional lenders that lend for rental properties.

The purpose of underwriting rental revenue from the lender’s perspective is to determine a reliable and conservative expectation of the revenue the property will earn annually over the next couple of years. Even though DSCR loans are almost always 30 years in term, because most borrowers pay off within five or ten years, and because over the long-term, rents generally increase year over year with inflation, projecting ahead for the next year or two is the inherently conservative approach taken by DSCR Lenders.

Overly “aggressive” or not, the underwriting methodology of rental revenue by DSCR Lenders is generally a huge win for real estate investors (borrowers) to enjoy easier qualification and optimized terms. The best strategy for real estate investors is to fully understand how DSCR Lenders underwrite rental revenues for every scenario, while being mindful to always underwrite their own deals to their own projections and risk tolerances as well.

The most basic or traditional DSCR Loan is for a single-family residence that’s rented out on a traditional 12-month long-term lease (the proverbial “Single Family Rental”). In these cases, whether the loan is for an acquisition or a refinance, the industry standard is for DSCR Lenders to use the lower of the lease amount and market rent, where market rent is sourced from the 1007 schedule of the appraisal or equivalent 1025 form for 2-4 unit properties.

Why do DSCR Lenders use the lower of the market rent and lease amount, instead of the actual, in-place lease amount, since that amount is what will actually be received versus just the “theoretical” market rent? Wouldn’t it be more accurate to use the actual amounts coming in every month on the actual lease? Well, there are multiple reasons for this conservative lender methodology.

For one, the leases that are considered “long term” for residential real estate investment properties, i.e. the types of properties securing DSCR Loans, are for 12 months, considered pretty short in most other contexts. For a comparison point, typical commercial leases for office, retail and industrial tenants range from five to ten years. Additionally, many DSCR Loans originated on properties with long-term leases are closed when the current lease or leases at the properties are in different stages of the 12-month term (i.e. with a few months left) or even month-to-month (“MTM”). Also, many long-term leases on residential real estate revert to “month-to-month” after the initial 12-month term ends, where either the landlord or tenant can terminate any month they choose after the initial lease year has passed. As such, there is no guarantee for the DSCR Lender that the lease amount is going to be the monthly amount each month for the following year, as rarely would an in-place lease cover the full 12 months following the loan’s closing date.

Q: What does MTM mean in real estate investing?

A: In real estate investing, MTM stands for “month-to-month” and refers to a rental agreement where the lease automatically renews each month until either the landlord or tenant gives proper notice to end it. MTM leases offer flexibility but can allow quicker rent adjustments or tenant changes compared to fixed-term leases.

Similar to how DSCR Lenders work hard to prevent underwriting the value of a property at an inflated amount, DSCR Lenders are similarly wary of projecting too high of rents and cash flow on a property they are lending on. In-place rents can be “overstated” versus actual reasonable expectations moving forward for a variety of reasons. For one, rental rates are pretty volatile, and can go up and down quite a bit; there is always a chance that the market rental rates when the lease was signed was higher in the past than what it will be when renewal comes up or the property needs to be re-tenanted. Second, just like buyers, tenants can sometimes overpay and emotionally fall in love with a unit, with a low likelihood of the landlord finding another case of this “lightning in a bottle” when renting it out next.

It is also important to note that DSCR Lenders don’t underwrite tenant quality and someone paying higher than market rents may actually be a sign that the tenant has a poor credit history and have been forced to pay more because they have a history of missed rents and higher likelihood to fall behind. In these situations, the “actual” in-place rents might be more like zero!

Finally, there is always the specter of potential fraud, and leases are not too difficult to forge or set up with a shady associate – a lease that is significantly above market rent can be an indicator of a fake lease, a relatively easy document to fake. A DSCR Lender’s methodology of not “giving credit” for this higher rent, i.e. using the lower market rent, prevents this sort of fraud scheme from having much utility. Some DSCR Lenders require verification of rents collected (such as two months documented receipts traced to bank accounts) but most DSCR Lenders do not have this requirement and choose to lighten the documentation requirements in this area to be more competitive and borrower-friendly.

For all those reasons, the majority of DSCR Lenders follow the straightforward policy for properties with long-term rental agreements in place: to use the lower of in-place and market. However, sometimes different methodologies apply for both instances of higher market rents than in-place rents and instances of higher in-place rents than market rents.

Q: Do DSCR Lenders require proof or verification of rental receipts for underwriting?

A: Most DSCR Lenders do not require formal verification of rent payments, such as bank statements showing deposits, in order to qualify a property’s income. Instead, the industry standard is to underwrite to the lower of the current lease amount and the appraiser’s market rent estimate, which reduces the need for rent receipt documentation. Some conservative lenders, however, require rent receipt verification on every loan with a lease, and others will ask for 2–3 months of proof only when in-place rents are significantly above market or when making exceptions to use higher rents, primarily as a fraud-prevention measure.

For properties with in-place rents that are higher than market rents some DSCR Lenders will allow the DSCR Loan to qualify with rents higher than the (lower) market rent amount with some restrictions. These lenders (still a minority of DSCR Lenders, most will strictly still use the lower market rent amount), will typically use up to 125% or 120% of the market rent. However, this comes with the caveat that in these cases, the qualifying rents will never exceed the actual in-place rents, such that if the in-place rent was $9,900 per month and the market rent was $9,000 per month, they would still cap the qualifying rent at just $9,900 per month, or 110% percent of market rent in this example, i.e. there would never be a qualifying rental revenue number above both the in-place rent and market rent. Additionally, in these cases, the DSCR Lender will likely require 2-3 months of rent receipt documentation (even if otherwise not required when using standard lower of in-place or market), primarily as a fraud prevention measure to ensure the significantly higher in-place rent is legitimate.

Similarly, for properties with market rents that are higher than in-place rents, a minority of lenders will also allow the use of market rents or up to 120% or 125% of in-place rents, but this is rarer and likely needs a legitimate reason. One scenario that makes “common sense” is for acquisition transactions in which the existing under-market lease (rents significantly less than market rent) are on a month-to-month lease. A frequent acquisition transaction financed by DSCR Loans occurs when a real estate investor targets a rental property that the current owner (seller) is poorly managing or not optimizing (typically through not charging high enough rents), with the plan to bring rents up to market post-acquisition.

Many DSCR Lenders still lean to the side of conservatism when these leases have a few months left since when acquirers of rental properties with valid leases take over the property, they also take over the lease and they typically can’t just terminate with the tenant because ownership changes. As such, the actual rents are what is likely to come in, at least for the first few months of the DSCR Loan term. However, most DSCR Lenders will be okay with using market rent when the buyer (borrower) is acquiring a property with a MTM lease, since the seller can immediately evict the tenant or raise rents to market upon acquisition. If using market rent to qualify in this situation, the DSCR Lender may ask for a short LOE from the borrower affirming this plan.

One thing that can be a surprise for some real estate investors, especially those used to investing in larger multifamily or commercial real estate properties, is that vacant properties are okay and eligible for DSCR Loans, albeit typically for acquisitions only. This makes logical sense, as most residential real estate properties are sold vacant or from an owner that was previously living in the property and is planning to move out. In these cases, the best way to underwrite the rents in the DSCR ratio is to use market rent as the expectation, assuming that upon purchase, the new buyer (i.e. the borrower on the loan) will rent the property out and achieve a lease at market rent (ipso facto – putting the property on the “market” for “rent”). So, in cases of vacant acquisitions, for both single family residences or condos with one unit, or even with properties up to four (even if all vacant) units, the DSCR Lender will use the market rent to determine rental revenue in the DSCR sourced from the appraisal’s applicable market rent form.

On the other hand, real estate investors from time to time inquire if they can get a DSCR Loan for a vacant property that is a refinance. Unfortunately for these investors, the answer is typically no; refinances of vacant properties are typically not eligible for DSCR Loans. The logic makes sense from the lender’s perspective: while it makes perfect sense to use market rent on acquisitions, as the new buyer should be capable of renting the property out at market rates, when it comes to refinances, it begs the questions; if the borrower already owns the property (and it is otherwise eligible, “turnkey” and in good rentable condition), a) why is it not rented? and b) if it can’t be rented easily at market rates; is the true “market rent” lower than what the appraiser determined?

In essence, it is hard to find a “good reason” for why a property sits vacant or has a vacant unit at time of a new refinance. And even if there is no fraud going on (such as a borrower secretly planning to occupy the property while claiming it is a rental), it is usually reasonable for the lender to just require the borrower to rent the property prior to close (which again, theoretically, should be relatively quick and easy to do at market rents: if the market rent number is correct and everything is above board).

There are very rare exceptions where some DSCR Lenders may do a vacant refinance. One type of scenario where it may be doable are cases of larger “build-to-rent” portfolios, where one borrower is refinancing a large batch of newly built properties, and renting them over time, and has a proven track record of this. Another might be a case of a multi-unit property that may have one unit vacant with the other(s) rented and providing revenue. This could make particular sense for multi-unit properties at the very high end, such as brownstone duplexes in New York City, where a borrower may care more about ensuring tenant quality than immediate cash flow, as there are higher risks that a bad tenant would not properly care for a high-end property and the Big Apple has notorious tenant-friendly laws in disputes, which could be financially devastating. However, these situations, where it may be justifiable for a DCSR Lender to do a refinance on a vacant property are few and far between.

Q: Can you get a DSCR Loan for a vacant property refinance?

A: In most cases, DSCR Lenders will not approve a refinance on a vacant property, since the lack of tenants raises concerns about the true market rent and the property’s ability to generate income, as well as concerns over occupancy fraud. While market rent is commonly used for acquisitions, lenders expect an already-owned property to be rented before closing. Rare exceptions exist, such as large build-to-rent portfolio refinances, multi-unit properties with only partial vacancy, or unique high-value rentals where tenant selection is critical, but these are uncommon and typically require a strong track record with the lender.

Q: Do DSCR Loan lenders apply credit loss or vacancy loss in underwriting?

A: DSCR Lenders do not apply a separate credit loss or vacancy loss factor when underwriting long-term rental properties. DSCR is typically calculated using gross rent from the lease or market rent, without an additional vacancy adjustment.

The use of DSCR Loans to finance short-term rentals (STRs) skyrocketed in recent years and the rental revenue qualification for these STRs has required different methodologies and rules, as the absence of long-term leases have made utilizing in-place rents not feasible. Additionally, as a general rule of thumb: well-run STRs can generate twice the gross rental revenue of an equivalent LTR, so relying on 1007 market rents for “vacant” properties (or STRs or planned STRs that don’t have leases in place) didn’t work well either, especially in vacation markets where short-term stays are the norm.

While some short-term rentals could qualify for DSCR Loans under this standard methodology, i.e. considering the property vacant and underwriting the rental revenue at the long-term appraiser-determined market rent, as both STR investing and DSCR Loans gained popularity and usage in the late 2010s, many DSCR Lenders adapted to the qualification of rental revenue for STRs with new methodologies. First to arrive was the utilization of “TTM Actuals” or the trailing twelve months of short-term rents to qualify the rental revenue for DSCR Loan refinances of short-term rental properties. This methodology meant that if the borrower had been operating the property as a STR for at least twelve months, the rental revenue in the DSCR calculation would be the amount of gross revenue earned from the property. This required full documentation, typically downloaded straight from airbnb or a property manager’s systems, and could only be used on refinances of properties owned for at least a year, but it was a gamechanger for many investors, particularly early adopters to the STR trend.

However, the TTM Actuals methodology is limited. For one, it applies to refinances only, as rental revenue from acquisitions still had to be qualified with appraisal-determined market rents (typically based on how much the property would earn as a long-term rental). Generally, even if borrowers were buying a true turnkey STR, i.e. the seller had been using the property as a short term rental and could provide twelve months of operating history, TTM Actuals couldn’t be used, as only history from the borrower themselves could be used to qualify. Additionally, this methodology restrained refinances that were coming off renovations, or the “AirBnBRRRR strategy,” requiring a full 12 months of waiting for seasoning to accrue the operating history to qualify, a big obstacle for investors that added value to properties instead of pursuing turnkey units.

Starting around late 2020, AirDNA, a data company tracking real-time STR performance and providing property-level projections via its Rentalizer tool began to be adapted by some DSCR Lenders to determine rental revenue from short term rentals. AirDNA’s Rentalizer uses scraped Airbnb and Vrbo data to project a median annual gross revenue for a specific property. Many DSCR Lenders have begun to utilize AirDNA for the rental revenue number for short term rental properties, particularly for acquisitions and adaption of this tool continues to increase over time, from a small handful of “STR-friendly” DSCR Lenders in 2020 to a large portion of the industry in 2025.

Key for AirDNA qualification is the use of a “haircut” by many DSCR Lenders, meaning, instead of simply just utilizing the Rentalizer number to project revenue, they will use a certain percentage of the projected rents, or subtract a certain “haircut percentage.” For example, if a property was projected by AirDNA to generate $100,000 in STR income in a year, some lenders may apply a “10% haircut” which would mean utilizing $90,000 for rental revenue qualification, with some utilizing a “20% haircut” (i.e. $80,000) or “25% haircut” (i.e. $75,000). DSCR Lenders differ not just in their approaches in utilizing AirDNA projections or not, but also in terms of what percentage haircut is utilized, if at all. Further, some DSCR Lenders will utilize different “haircuts” based on investor experience (i.e. only utilizing a haircut if the investor doesn’t have a documented track record of STR success with other properties) or other similar methodologies.

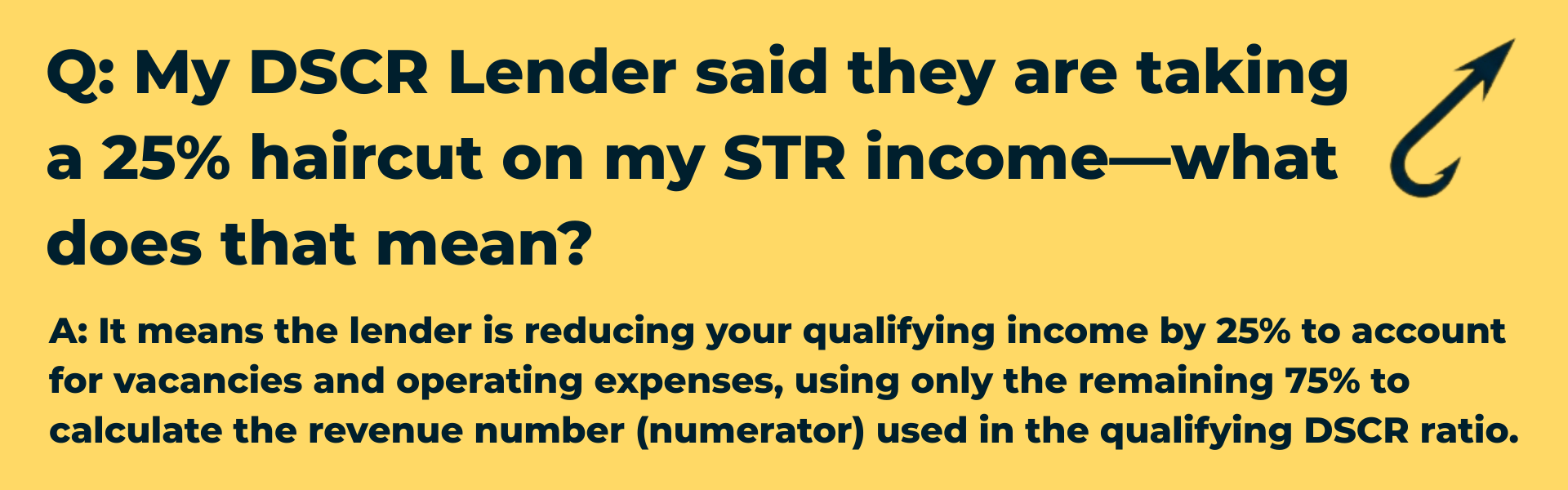

Q: My DSCR Lender said they are taking a 25% haircut on my STR income—what does that mean?

A: It means the lender is reducing your qualifying income by 25% to account for vacancies and operating expenses, using only the remaining 75% to calculate the revenue number (numerator) used in the qualifying DSCR ratio.

Additionally, while AirDNA projections are typically utilized for acquisitions of properties intended for STR usage, some DSCR Lenders will allow them to be utilized for refinances, including cash-out refinances, applying similar haircuts and potential experience requirements. This can include requirements such as a documented listing showing the property is up and running and fully renovated and furnished, as well as proof of a legitimately completed booking, mostly as a measure to avoid any potential occupancy fraud concerns. Additionally, for using AirDNA projections for either acquisitions or refinances, some DSCR Lenders have additional hurdles, such as requiring minimum AirDNA “market grades” or projected occupancies from the website.

Some DSCR Lenders have also experimented with so-called “STR-based 1007s” for the rental revenue qualification number, i.e. to specifically instruct the appraiser to determine their market rent estimate based on short term rental comps rather than the traditional long-term market rent comparables. However, this has started to fall out of fashion by 2026 for several reasons, including many appraisers not being qualified or comfortable with this process, specific guidance from Fannie Mae (who developed the 1007 form) that it was not intended to be utilized in this manner as well as the growing trust with alternatives like AirDNA.

Another recent alternative that has emerged in 2025, is what is called a “Narrative Short Term Rental Rent Analysis,” which essentially instructs the appraiser to conclude an STR market rent, but instead of using the 1007 form, utilizes a new template and methodology, more geared towards STRs. Some DSCR Lenders that are now embracing this new form and methodology will typically also apply a “haircut” and other restrictions, similar to their treatment of AirDNA.

Finally, there are some DSCR Lenders, particularly larger ones with long-standing track records of quality underwriting and risk management, that use a “holistic approach” to determining a rental revenue number for STRs, having their in-house experts and underwriters utilize multiple sources and judgments to determine the rental revenue numerator in the DSCR.

Q: Do properties need to be rented or have a lease to qualify for a DSCR Loan?

A: No, properties do not have to be currently rented or have a signed lease to qualify for a DSCR Loan. For acquisitions, vacant properties are almost always acceptable, and most DSCR Lenders will qualify short-term rental (STR) properties without requiring a traditional long-term lease. However, for refinances, a property that is neither leased nor operating as an STR will typically not be eligible.

Up Next: PITIA Determination for the DSCR Ratio in Final Underwriting for DSCR Loans

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.