.png)

The biggest difference between traditional DSCR Loans and Multifamily DSCR Loans is simple: unit count. Traditional DSCR financing stops at one to four units, while Multifamily DSCR Loans extend to properties with five or more units, usually capped at eight, nine, or ten depending on the lender.

Beyond unit count, there are both similarities and differences worth understanding. In many ways, Multifamily DSCR Loans work just like their 1–4 unit DSCR Loan counterparts; they are still primarily based on the property’s cash flow, they follow the same streamlined, no-income verification and no-tax returns qualification structure, and they carry over familiar loan structures, such as the 30-year fixed rate term and similar prepayment penalty options.

But there are also distinct differences: lenders tend to require higher credit scores, lower maximum LTVs, and more prior experience when stepping into the 5–10 unit space. We will break down a comparison of “what’s the same” and “what’s different” when it comes to Multifamily DSCR Loans versus what real estate investors may be used to with standard DSCR Loans for 1-4 unit residential properties.

Additionally, while many small multifamily properties (in the 5-10 unit range) are too small to be eligible for traditional commercial or multifamily lenders, many real estate investors may have multiple options when financing a small multifamily, including both Multifamily DSCR Loans and loans from commercial lenders or banks. For example, a six-unit property worth seven figures will likely be eligible for both Multifamily DSCR Loans and some bank or conventional multifamily loan programs. We’ll break down how Multifamily DSCR Loans compare to other typical multifamily Loan options and when it might make sense (or not make sense) to utilize DSCR Loans for these investments.

Multifamily DSCR Loans are DSCR Loans at the end of the day, overwhelmingly more similar to the traditional DSCR Loans securing 1-4 unit properties than anything else, including conventional loans, non-QM DTI-based loans, bank or credit union financings and loans offered by CRE (commercial real estate) or larger Multifamily lenders. That being said, they are still only offered by a minority of DSCR Lenders as of 2025 and often have their own set of both rate sheets and guideline “matrices” that separate qualification, program limits and pricing (interest rates and fees) from a lenders’ standard DSCR Loan program.

Q: Can I use a DSCR Loan for multifamily properties with 5+ units?

A: Yes. Some DSCR Lenders now offer Multifamily DSCR Loans for 5–10 unit properties. However, these loans are only offered by a portion of DSCR Lenders and typically require higher minimum credit scores, lower maximum LTVs, and more experience among other things compared to 1–4 unit DSCR loans, but are typically easier to qualify for than traditional commercial multifamily financing.

Multifamily DSCR Loans are generally considered higher risk for lenders than standard 1–4 unit DSCR Loans, and the reasons are straightforward. First, market liquidity: the resale market for single-family homes is far larger than for duplexes, triplexes, or fourplexes, which is why lenders give SFRs the most favorable terms. If a loan defaults, foreclosure and resale are the lender’s primary backstop, and the deeper the buyer pool, the easier it is to recover value quickly. Beyond four units, the buyer pool shrinks further, making values more volatile and potentially needed recoveries through foreclosure less certain.

Second, operational complexity: managing cash flow across five to ten units is far more demanding than keeping one unit rented. Larger properties require more skill to maintain occupancy, handle repairs, and keep income consistent. As such, required experience levels and cash flow (i.e. minimum DSCR ratios) are higher.

How does this generally look in practice? A DSCR lender that has both a standard DSCR Loan Program and a Multifamily DSCR Loan program may have:

While these limits on key metrics stand in stark contrast, there are plenty of similarities and overlaps here too, particularly on how these metrics are calculated. While the maximums (LTV) and minimums (DSCR, FICO) might be more conservative for Multifamily DSCR Loans, the way they are determined are still extremely borrower-friendly and in line with standard DSCR Loans.

Valuation of the subject property (for calculating LTV) is typically done with the same methodology (independent third party appraisal, lower of appraised value and purchase price for acquisitions) and can typically be the reports produced under FHLMC 71A & FHLMC 71B (Freddie Mac) or the “Small Residential Income Property Appraisal Report - FNMA 1050 (Fannie Mae) standards – which are much shorter and cheaper (for borrowers) than standard multifamily appraisals that typically run $3,000 or more and take longer to produce (“narrative” appraisal reports).

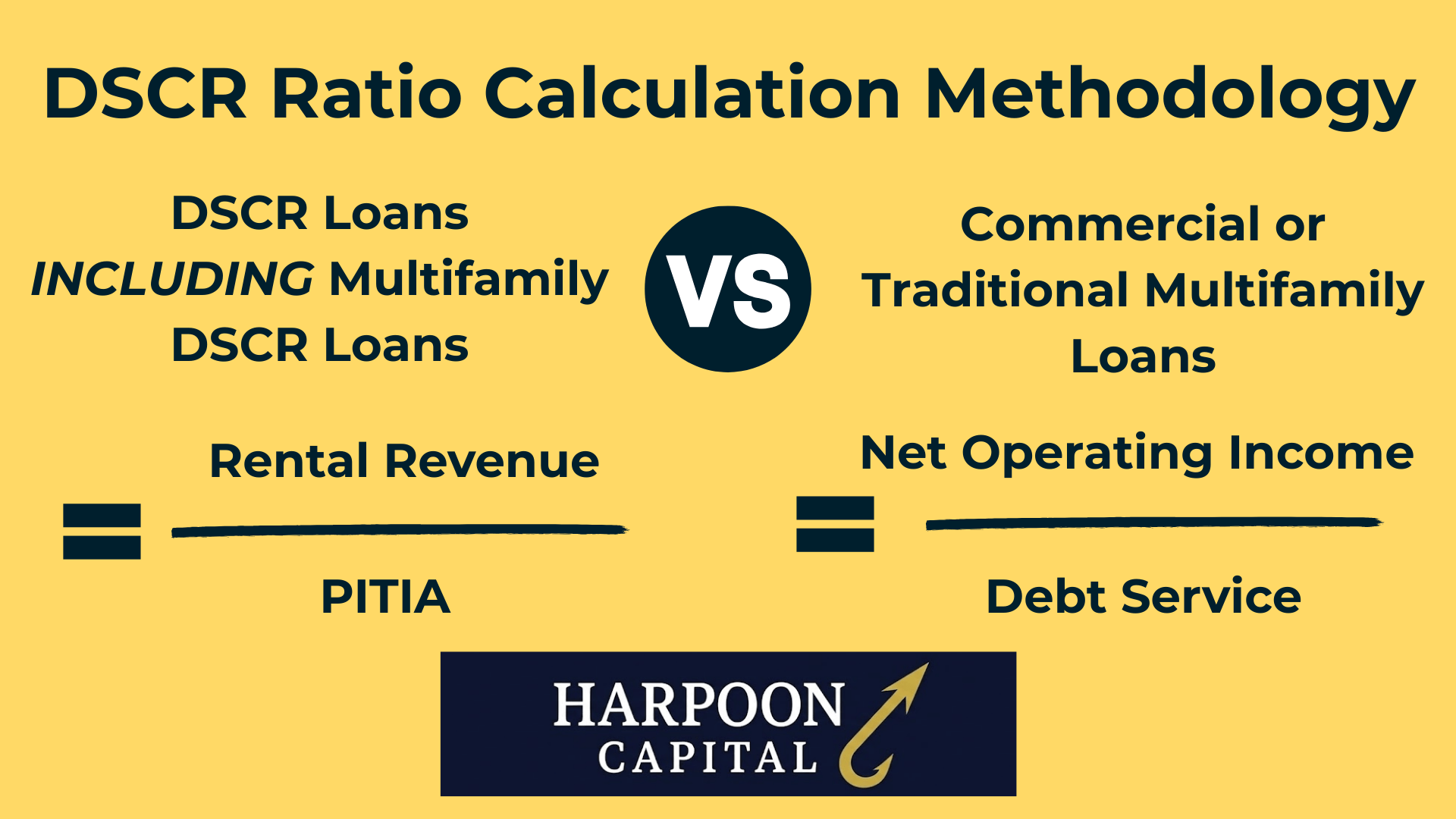

And one of the biggest benefits of Multifamily DSCR Loans is that the DSCR calculation is done in the traditional residential fashion (Rental Revenue divided by PITIA) instead of the way commercial or larger multifamily lenders typically compute it, which is NOI divided by debt service. This means that when qualifying a Multifamily DSCR Loan’s DSCR ratio, no expenses are considered besides property taxes and insurance, meaning the lender won’t typically “count” expenses such as utilities, management fees, repairs & maintenance, landscaping, capex and vacancy or credit loss, all of which are typically deducted from the NOI when traditional CRE lenders calculate DSCR, presenting significantly harder qualification hurdles. Further, the typical minimum DSCR ratio for multifamily loans from conventional (i.e. Freddie Mac) or CRE lenders (like banks or CMBS) is 1.25x, including all of the additional expenses, versus just 1.00x for Multifamily DSCR Loans, which is lower and only includes property taxes and insurance in the expense load!

This DSCR computation difference is the biggest benefit by far for Multifamily DSCR Loans, an incredibly easier qualification and borrower-friendly lower DSCR ratio hurdle than competing options.

To illustrate this stark difference (and how Multifamily DSCR Loans have such an advantage in this area), let’s look at an example small Multifamily property that has the following financials:

These numbers are just estimates and can vary widely by property, market and many other factors, however can definitely fit the typical profile of a small multifamily property between 5 and 10 units.

Let’s look now at how lenders would calculate the DSCR ratio for qualification and pricing purposes, which will be very different depending on if it’s a Multifamily DSCR Loan or a traditional multifamily loan from a commercial lender. With the familiar formula of Rental Revenue ÷ PITIA for DSCR Loans, and the more stringent NOI ÷ Debt Service (PI) for the traditional multifamily lender.

The DSCR Lender would calculate DSCR Ratio for this multifamily property with the standard Rental Revenue ÷ PITIA:

The DSCR Ratio for a Multifamily DSCR Loan would be calculated as 1.48x, well above the likely program minimum (of 1.00x or sometimes 1.15x) and also likely in the “top bucket” for best pricing (i.e. lowest rate).

Now let’s look at how a traditional multifamily lender would calculate the DSCR ratio for this same exact property:

Note just how much harsher the calculation is by the commercial lender, this same property gets a much lower 1.15x DSCR ratio under the CRE or traditional methodology, versus 1.48x using the DSCR loan residential methodology. Further, this loan would not likely even qualify for a traditional multifamily loan since the CRE lender minimum DSCR ratio is almost always 1.25x! Thus, the investor, if needing to qualify with the traditional commercial lender for this property, would likely have to reduce the loan amount significantly (and thus invest way more capital, further crimping returns) to obtain traditional multifamily financing.

While qualifying credit scores minimums are generally higher for Multifamily DSCR Loans than for standard programs, it is generally around only 700, still covering around 60% of the population at large, not typically a significant hurdle for serious real estate investors shopping in the multifamily space. Additionally, DSCR Lenders will typically still have the same benefits for vesting approaches for Multifamily DSCR Loans as they have for traditional 1-4 unit DSCR Loans, such as offering investors the ability to borrow through an entity and structure among multiple guarantors to maximize qualifying score (i.e. utilizing the higher of two median scores for partnerships).

Beyond the “big three” factors of LTV, DSCR and FICO that play the largest role in DSCR Loan qualification and pricing, there are also some notable similarities and differences between typical Multifamily DSCR Loans and traditional DSCR Loans.

For Loan Amounts and Property Values, Multifamily DSCR Loans will generally have a smaller loan amount window, both a higher loan amount minimum and lower loan amount maximum than traditional DSCR Loans. A typical loan minimum for a Multifamily DSCR Loan will be $250,000 to $400,000, and, when combined with 75.0% LTV limits, means minimum property values of around $333,333 to $533,333. A typical loan maximum for a Multifamily DSCR Loan is generally around $2,000,000, which is in line with typical traditional DSCR Loan maximums, although it’s not uncommon for some DSCR Lenders to expand up to $2.5 million or even higher ($3.5 million is generally the industry absolute max) for DSCR loans secured by single family rentals.

Loan Size minimum is usually the biggest hurdle for investors looking for Multifamily DSCR Loans as there are many 5-10 unit properties in the mid to low six figure value range where the loan amount is too small, rendering the deal ineligible. Confirming loan amount minimums for a Multifamily DSCR Lender immediately upfront and if any exceptions might be available is the smart move to avoid headaches and wasted time.

Regarding Loan Term, Loan Amortization Structure, Loan Rate Structure and Prepayment Penalty Provisions, Multifamily DSCR Loans are typically the same as traditional DSCR Loans. Loan structure options will typically be 30-year loan terms with the same amortization or interest-only options (i.e. can choose fully amortizing or a partial-IO structure for the first 10 years) and the same options for 30-year fixed rate or hybrid (fixed to ARM) as well. Further, Multifamily DSCR Loans will typically have the same prepayment penalty provision options and related pricing benefits but also generally have no prepayment restrictions as all of the laws and regulations restricting prepayment in certain states are generally not considered applicable for any properties with five or more units. Multifamily DSCR Loans provide not only all the great borrower-friendly loan structure options as traditional DSCR Loans - they actually provide additional options!

Loan Structure is another area where Multifamily DSCR Loans shine versus traditional CRE or Multifamily loans offered through banks or Freddie Mac Multifamily. The 30-year term is often beloved by borrowers who want to avoid the shorter loan terms typical of the traditional options, which tend to span only five, seven or ten years. These traditional multifamily loans also typically require a “balloon payment” meaning a very large payment at maturity, instead of the standard payment required at the end of thirty years for most DSCR Loans that is the same as all the other 359 monthly amounts. Balloon payments can cause significant stress and losses for borrowers, as a looming large payment can force a sale or an ill-timed refinance if conditions aren’t ideal when the maturity date hits.

Additionally, many CRE and traditional Multifamily lenders have much harsher prepayment penalty provisions, and can include concepts such as lockout periods, which means the borrower can’t prepay the loan no matter what for the first few years of the term, even with a fee. Traditional multifamily loans can also have prepayment penalty provisions such as defeasance or yield maintenance, meaning instead of being required to pay a lowish fee (no more than 5% of remaining balance), the borrower would owe an estimate of all the remaining interest due on the loan for the remainder of the term and these periods typically make up most of the loan term, instead of a max of just the first five years of a 30-year term typical for Multifamily DSCR Loans.

Since multifamily properties include a higher level of sophistication and management responsibilities, it’s no surprise that Multifamily DSCR Loans typically have a bit more stringent investor experience and mortgage and credit history requirements than traditional DSCR Loans. This makes sense, as many investors move to multifamily after starting out investing in single family rentals or basic house hacking (i.e. a duplex with one unit rented). While traditional (i.e. 1-4 unit properties) DSCR loans typically are okay for first time investors (with potentially only minor restrictions like slightly higher credit score minimums and maybe 5% lower LTV maximums than otherwise available), generally “first time investors” are not eligible for Multifamily DSCR Loans. It’s important to note that “first time investor” generally is defined by most DSCR Lenders as anyone that doesn’t have a full 12 months of rental property ownership in the preceding three years and not simply “first time ever” investing.

Additionally, a 30-day late payment on a mortgage loan in the last year or a single significant credit event (i.e. bankruptcy, foreclosure, short sale or deed-in-lieu) in recent 3-4 years are generally not dealbreakers for DSCR Loans on 1-4 unit properties (although typically come with additional restrictions and higher rates), they tend to be dealbreakers for Multifamily DSCR Loans, generally a borrower needs a fully clean recent history on real estate debt: no recent mortgage lates or credit events in the preceding handful of years.

While these added restrictions make qualification a bit tougher for Multifamily DSCR Loans versus the traditional DSCR Loans, it makes sense for both borrower and lender: multifamily real estate investing works best after the investor has some experience and recent success under their belt; if investing in real estate for the first time or after running into significant recent credit issues; it likely makes a lot more sense to stick to simpler properties like single-family rentals or small multi-units like duplexes or triplexes before making the leap.

In the same vein, Multifamily DSCR Loans will typically have higher liquid asset reserve requirements versus the requirements for standard DSCR Loans from the same lender. While liquid asset requirements vary a lot from lender to lender, traditional DSCR loans will typically have 2-6 months PITIA liquid asset reserve requirements, while the range for Multifamily DSCR Loans is more likely to be in the 6–12-month PITIA range, it can also scale up to the higher end of the range with higher loan amounts.

While the aggressive borrower-friendly DSCR ratio underwriting is a hallmark of Multifamily DSCR Loans, there are some significant differences for DSCR Loans securing 5-10 unit properties when it comes to vacancy and property usage. Even though Multifamily DSCR Loans do not include any vacancy or credit loss deductions from gross rental income like traditional multifamily lenders, DSCR Lenders are not as amenable to vacant units when it comes to multifamily properties, even on acquisitions, where fully vacant properties are typically A-OK and underwritten at full market rent. Most Multifamily DSCR Lenders will allow a maximum of one or two vacant units on 5–10-unit properties and instead of counting 100% of market rent, typically will use a “haircut,” for example counting only 75% of any vacant units’ market rent.

This is in contrast to traditional DSCR loans where properties typically get credit for 100% of vacant unit market rent (at least for acquisitions). This makes sense, as keeping 100% of units occupied for 100% of the year when the property has five or more units and tenants to worry about is much less realistic, turnover and minor vacancies as leases expire and tenants move in and out is expected and normal in multifamily investing. Plus, these properties usually produce so much cash flow it doesn’t harm the DSCR ratio too much when applying a minor “haircut” to rental revenue to account for a vacant unit or two.

Additionally, even the most “STR-friendly” DSCR Lenders that also offer Multifamily DSCR Loans will typically not allow STR usage (let alone alternative rental qualification methods like AirDNA projections) for 5-10 unit properties. This is because these properties are considered too far into the hotel/motel “hospitality” side of the classification ledger, as compared to the “residential” asset class that DSCR Loans are intended for. Typically, usage, rent qualification and market rent projections for Multifamily DSCR Loans must always be based on traditional 12-month long-term leases.

Based on the above walkthrough, DSCR Loans for eligible multifamily properties (in the right unit range, i.e. around 5-10, and value range, i.e. $400,000 to $2,500,000) seem to be a no-brainer for investors. There’s a much easier qualification methodology when it comes to DSCR calculations and minimums, and investors get the coveted 30-year fixed rate structure to boot.

Well, unfortunately it’s not that simple. There are two big advantages that traditional CRE or Multifamily lenders have over Multifamily DSCR Loans: pricing and recourse. By pricing, it’s fairly accurate to say that the interest rate for a Multifamily DSCR Loan is likely going to be significantly higher than the alternative options such as through a bank, CRE lender (like a CMBS issuer) or Freddie Mac conventional multifamily. Multifamily DSCR Loans are also typically higher in rate than traditional DSCR Loans, sometimes significantly (such as 1 to 2 percent). The difference is the same or even starker for Multifamily DSCR Loans vs. traditional Multifamily Loans, with as much as a 2-3 percent difference not unheard of. For example, a Freddie Mac “conventional” Small-Balance Multifamily Loan might quote a rate at 6% when an equivalent Multifamily DSCR Loan on the same property would be 8%.

In addition, many traditional Multifamily loans have guarantors that are non-recourse or sometimes called non-recourse with “bad boy” carveouts versus Multifamily DSCR Loans, which are still full recourse to the guarantors. What does this mean? The “recourse” provision governs liability to make the “lender whole” in case things go wrong, the loan is defaulted (not paid back) and after the foreclosure process (lender takes ownership of the secured collateral, in this case, the investment property), the lender sells the property and the amount received is less than the balance due (outstanding defaulted loan balance plus any accrued fees or interest). The “recourse” aspect of the loan governs if the lender has one final way to recoup the balance of what’s owed, through a “guaranty” from an individual or entity.

For DSCR Loans, including Multifamily DSCR Loans, there will always be a full recourse guaranty required by an individual (“warm body” in real estate lingo) that is on the hook in cases of a default, foreclosure and an amount still due. In contrast, “non-recourse” loans, typical for traditional CRE and larger multifamily, means that in this situation, the lender is typically out of luck and takes a loss on any amount still due after foreclosure proceeds. There are typically still guarantees as part of loan documents that are non-recourse, however, these just include what’s typically called “bad-boy carveouts” which essentially means that there is no recourse on the loan except for if the guarantor commits significant bad activity such as fraud, gross negligence or criminal acts. If this occurs, then the lender will be able to go after the guarantor as if there were full recourse. Typically, these Multifamily Loans from traditional CRE lenders will be “non-recourse” and sometimes even have the non-recourse guarantor an entity and not an independent “warm-body” person, although this would be more common at loan sizes well above what might have a DSCR Multifamily Loan alternative.

There are two significant advantages for traditional Multifamily Loans versus Multifamily DSCR Loans for situations where a real estate investor may have options for both. If lower interest rates and avoiding full recourse are top priorities, Multifamily DSCR Loans may not stack up well against the alternative. However, these differences, upon closer look, are not as material of an advantage in many cases as they may appear.

Let’s take a look at the math on an illustrative example:

A real estate investor is looking to purchase a 7-unit multifamily property for $1,333,333 purchase price and value, looking to put 25% down for a 75.0% LTV ratio and considering options as such for a $1,000,000 mortgage loan.

This investor gets three quotes:

Quote A) Traditional Multifamily CRE Lender, offers a 6% Interest Rate with a 10-Year Term and a 20-Year Amortization Schedule, with a Balloon Payment structure.

Quote B) Multifamily DSCR Lender, offers 8% Interest Rate with a 30-Year Term that is Fully Amortizing, with equal monthly payments due until and at the maturity date.

Quote C) Multifamily DSCR Lender, offers 8.5% Interest Rate with a 30-Year Term that has a Partial-IO structure, with interest-only payments due for the first 10 years of the term, then amortizing on a 20-year schedule for the final 20 years of the term.

Before crunching the numbers, it looks like Quote A – the traditional Multifamily Loan offer (likely from a bank or Freddie Mac Small-Balance Multifamily originator) appears to be the best – the rate is the lowest by far (200 basis points or 2% lower than the Multifamily DSCR Loan, and 250 basis points or 2.5% lower than the Multifamily DSCR Loan with an interest-only option).

But digging deeper, let’s take a look at what the monthly debt service payment is for each of these quotes. Often, this is what matters for many real estate investors as it is one of the main drivers of cash flow and the key investment return metrics investors look to for evaluating deals, such as return on equity and cash-on-cash returns. The actual dollars and cents that are coming in and going out every month are typically more important than whatever numbers go into the formulas behind the scenes: show me the money is what typically matters most for investors! After all, financial freedom isn’t about the interest rate written in your filed away loan docs, it’s about the money in the bank.

So what’s the monthly payment for these three quotes? The results may surprise you:

Quote A: The monthly payment is $7,164.31 (based on 6% rate, 20-year amortization) and a balloon payment of $645,314.20 is due at maturity (in 10 years)

Quote B: The monthly payment is $7,337.65 (based on 8% rate, 30-year amortization) and there is no balloon payment (standard $7,337.65 payment is due at maturity in 30 years)

Quote C: The monthly payment approximately is $7,083.33 for the first 10 years (based on 8.5% rate, interest-only payment), with this jumping to $8,678.23 after 120 months, which would be the amount due at maturity, also in 30 years.

The immediate takeaway is that the quote with the highest interest rate has the lowest monthly payment! Despite the much higher rate, a Multifamily DSCR Loan with an interest-only provision can generate the most cash flow! Additionally, there is little difference in monthly payment between Quote A and Quote B, just $173.34 per month or a difference of just 2.4%! Despite a gigantic gulf in interest rate – 6% versus 8% - the actual monthly payments are minimal.

Finally, there is a looming balloon payment for the traditionally structured Multifamily Loan in Quote A - $645,314.20 due in 10 years – putting pressure on the investor to plan ahead to make this large payment due – while the Multifamily DSCR Loan options have lengthy 30-year terms with no such pressure valve.

It’s also important to note that the risks of full recourse versus non-recourse are typically overblown in the minds of real estate investors weighing the importance of the guaranty provision. Multifamily lenders, whether they are banks or traditional commercial multifamily lenders, conventional lenders or DSCR Lenders, rarely are actually required to use recourse to collect on defaulted loans. This only occurs in cases of serious fraud or criminality (for which the recourse vs. non-recourse distinction wouldn’t even matter – due to the “bad boy” carveouts) or in cases where the foreclosure proceeds fail to recoup what’s owed.

Since these loans will often have LTV ratios of 75.0% or less, there is always going to be a significant “cushion” between what the property is worth and what is owed, so in the vast majority of cases, even when fees and accruals pile up and some value degradation occurs, the proceeds from selling the foreclosed property will likely cover the gap. As such, the final “recourse” option for real estate investors is not likely to be a typical factor on these loans (regardless of the source, DSCR Lender or otherwise), and thus shouldn’t be weighted too heavily as a consideration for most investors, especially by investors that are responsible and strategic, with no intention or likelihood of defaulting on their loans.

Some other smaller nuances for Multifamily DSCR Loans that can come up in the lending process are related to the property’s market and the appraisal. These can be typical “snags” that can complicate DSCR deals for multifamily properties. A few additional things to be on the lookout for when considering a Multifamily DSCR Loan include the appraisal order, market classification rules and gift fund policy.

This is going to vary from lender to lender, but the appraisal for a Multifamily DSCR Loan will likely be either the expanded residential appraisal (such as the FNMA 1050) or a full commercial-style “narrative” appraisal. Regardless of the choice, there will likely be additional requirements for a multifamily appraisal versus one for a traditional 1-4 unit residential property, which can include things like:

Sometimes, especially for appraisers that are mostly used to residential properties and are picking up a rare multifamily bid, there could be missing items or overlooked requirements that delay deals and add costs. Thus, it’s smart for well-prepared borrowers to spend a little extra time making sure this is all done right the first time in order to maximize changes for a smooth and timely deal.

Multifamily properties (5-10 Units) secured by DSCR Loans might typically have different market rules, such as differing restrictions against being in a “Rural” market (as determined by appraisal or alternative measures such as a USDA map) and more stringent restrictions on acreage (like a 2-acre maximum versus higher limits like 10 acres for SFRs). In addition, some DSCR Lenders may have additional state or market restrictions or “overlays” that apply to multifamily properties but not for their traditional 1-4 unit programs.

Finally, gift funds are typically prohibited for down payments for Multifamily DSCR Loans, while lenders will typically allow them, subject to some limits, for traditional DSCR loan down payments.

Q: What is Debt Yield for a Mortgage Loan?

A: Debt Yield is a commercial lending metric calculated as Net Operating Income ÷ Loan Amount. It’s not typically used for DSCR Loans, but some lenders may apply a debt yield test, often around 9% minimum, on DSCR loans for multifamily or mixed-use properties.

Up Next: Guide To DSCR Loans for Mixed Use Properties

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.