.png)

A DSCR Loan is a type of mortgage loan designed for real estate investors where the underwriting is based primarily on the income-generating potential of the property rather than the borrower’s personal income. Essentially, these loans are a financing solution that offers more flexibility and easier qualification than constraining conventional options while still featuring competitive rates and terms that are much closer to conventional counterparts than the “last-resort” options from loan sharks or “hard money” lenders. Designed with “common-sense,” DSCR Loans offer investors a much-needed middle option, with reasonable documentation requirements, low enough rates and long enough terms to make deals work. DSCR Loans are a “goldilocks” loan type that have the perfect mix of qualification ease and attractive terms. They are accessible to most real estate investors and aspiring investors. Thanks to the existence of DSCR loans, successfully financing rental properties is no longer restricted to those with high enough personal incomes and tolerance for mountains of documentation paperwork, or people desperate enough to pay predatory rates and sky-high fees of hard money.

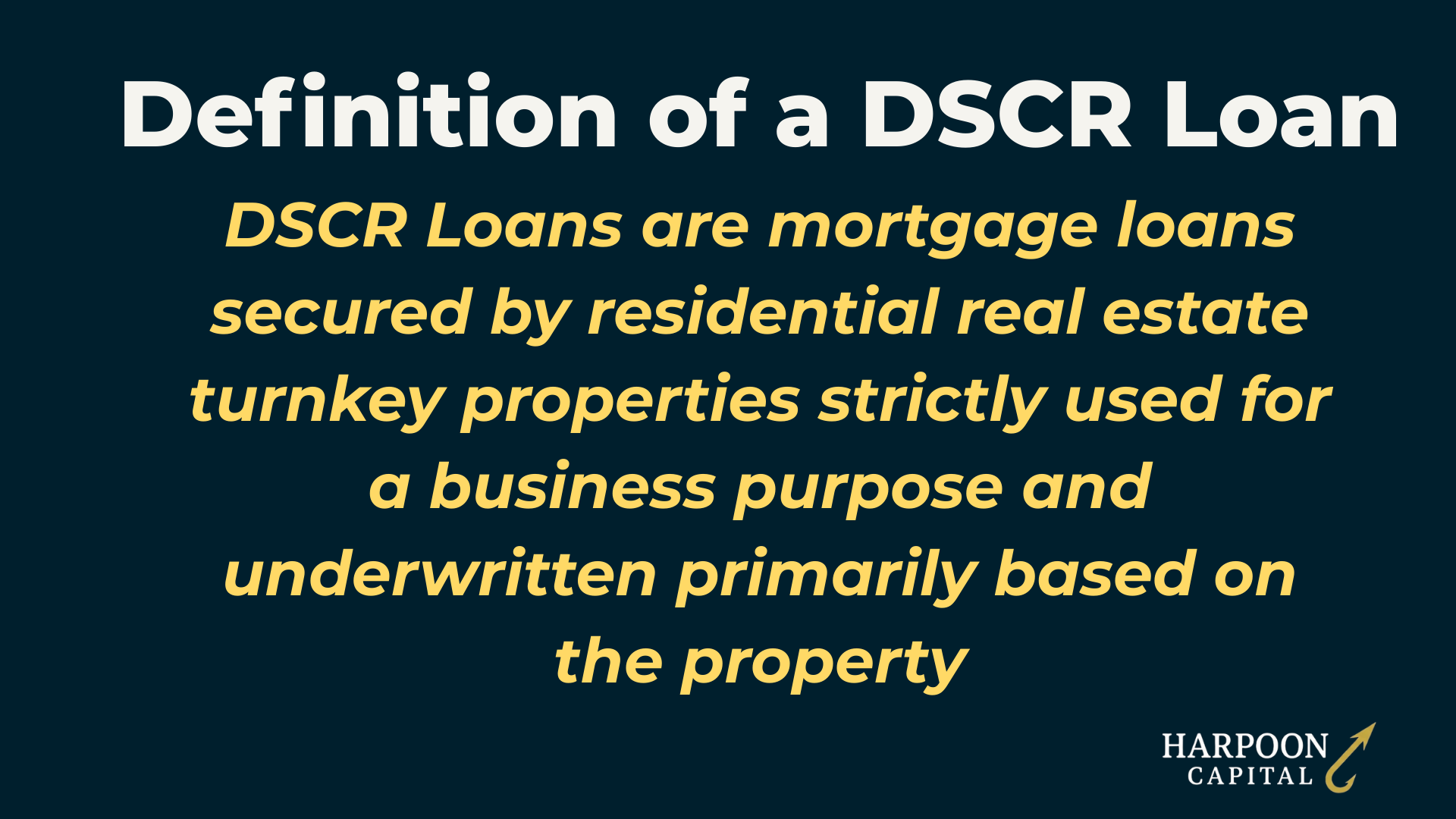

A DSCR Loan is defined as:

DSCR Loans are mortgage loans secured by residential real estate turnkey properties strictly used for a business purpose and underwritten primarily based on the property

Each aspect of this DSCR Loan Definition is purposeful and important. Let’s address each piece and why it’s important for understanding DSCR Loans, the emerging leading loan option for rental property investing.

DSCR Loans are loans that are secured by real estate, that is, the real estate itself serves as collateral for the loan. This means that if a borrower defaults on the loan (doesn’t pay the required debt service payments), then the lender or owner of the loan can foreclose on the real estate property and take over ownership of the asset. Mortgage Loans are secured loans in which the collateral is real estate. Other examples of secured loans are Auto Loans (secured by a vehicle) or even loans secured by assets like Bitcoin (Bitcoin Secured Loans). Unsecured loans are loans in which if the borrower defaults, the lender can’t take ownership of any collateral asset. Examples of unsecured loans include debt such as student loans or credit cards. Since there is no collateral for the lender to take in case things go wrong, interest rates on unsecured loans tend to be higher than secured loans.

The collateral for DSCR Loans is a specific type of real estate, in this case, properties that are residential in nature (usage is for living) and not commercial (such as usages for business or commerce). Sometimes people get confused and think that commercial real estate lenders (i.e. lenders that lend on commercial real estate (“CRE”) like offices or industrial properties) offer DSCR Loans, but these loans are a different loan type with very differing qualification standards and attributes. Since CRE lenders often use the DSCR ratio for qualification and underwriting, this can be confusing for many when just learning about financing options. Luckily, the guide you are reading goes over everything you need to know about DSCR Loans and clears these confusions!

A final note: as is common across real estate, there are exceptions to nearly every rule and many terms that can be confusing, and this aspect of the DSCR Loan definition is a good example of these phenomena. When DSCR Loans are described as being for residential real estate, this typically means residential properties between one and four units, while anything with five or more is considered “multifamily” and is typically considered separate from both residential (1-4 units) and commercial (i.e. properties where people go to work). Additionally, in recent years, some DSCR lenders are now offering DSCR Loans for multifamily (generally 5-10 units) or even Mixed Use (mostly residential with some commercial space). DSCR Loans are also a top option for Short Term Rentals, where tenancy is better classified as “short stays” rather than full-time residential living as the use; however, these properties are typically financed by residential DSCR Lenders rather than commercial hotel lenders!

In real estate, the term “turnkey” refers to properties that don’t need any renovations or repairs in order for someone to move in. The idea is that all the work that’s needed is to “turn the key” in the front door and the tenant is good to go! A key aspect of DSCR Loans is that the properties must be turnkey with no major repairs needed (generally most DSCR Lenders will require the appraisal to show less than $2,000 of deferred maintenance, or only very minor repairs that wouldn’t preclude living). Sometimes investors who utilize real estate investing strategies such as fixing and flipping will finance these purchases. However, loans for these scenarios are referred to as “Hard Money Loans” and if the property needs any significant repairs, it won’t be eligible for a DSCR Loan. This can confuse some investors since there are many private lenders that offer both DSCR Loans and Hard Money Loans, so the key takeaway to remember is that for DSCR Loans, you need a turnkey property. If it needs work, you probably should investigate hard money loan options.

%20v3.png)

Q: How do DSCR Loans Compare to Hard Money Loans?

A: DSCR loans are designed for stable, income-producing rental properties. Hard money loans are short-term and typically used for distressed properties that need rehab, like fix-and-flips. Hard money loans also come with higher rates and interest-only payments, while DSCR loans offer longer terms and lower rates.

One of the most important aspects of DSCR Loans is that the loan must be used for a “business purpose.” In non-technical terms, this means that the property must strictly be used as an investment property, not occupied by the owner (or any close relatives). Lenders are very strict on this point and many steps are taken in the qualification and underwriting process to confirm it’s being used as an income-producing property as there are potentially very serious consequences for DSCR Loan occupancy fraud. The DSCR Loan “business purpose” rule even applies to cash-out refinances, where even cash-out proceeds must be used for a business purpose (i.e. buying more real estate or even funding unrelated businesses) and cannot be used for personal reasons (such as paying off personal income taxes or going on vacation).

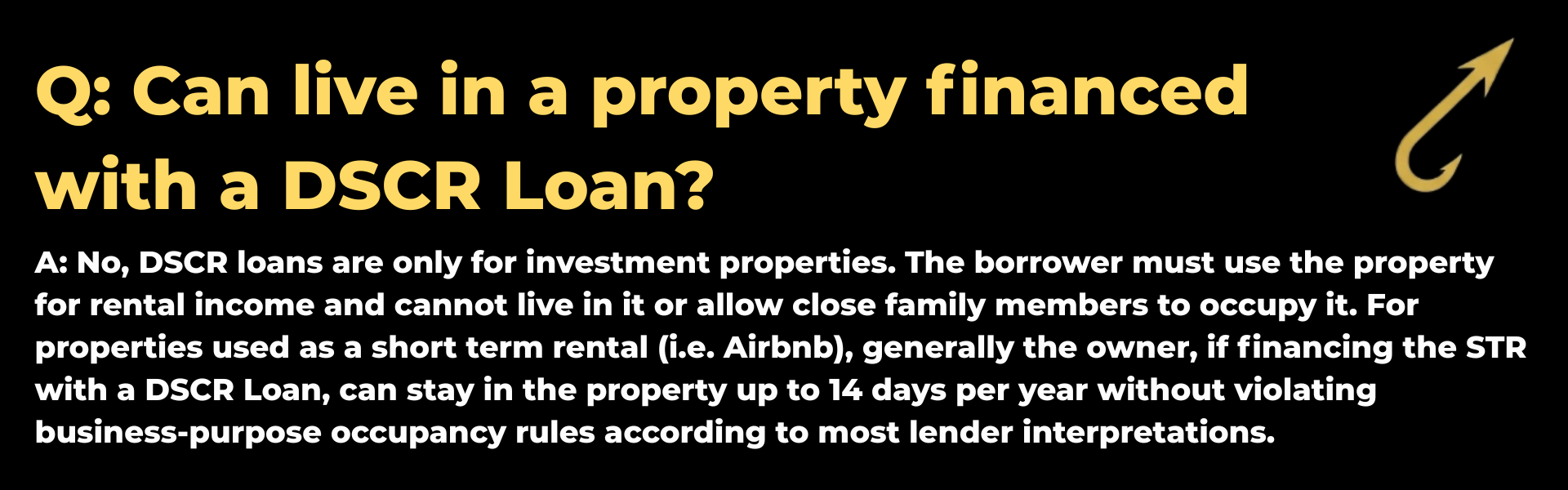

Q: Can I live in a property financed with a DSCR Loan?

A: No, DSCR loans are only for investment properties. The borrower must use the property for rental income and cannot live in it or allow close family members to occupy it. For properties used as a short term rental (i.e. Airbnb), generally the owner, if financing the STR with a DSCR Loan, can stay in the property up to 14 days per year without violating business-purpose occupancy rules according to most lender interpretations.

The last important (but very important) aspect of the definition of DSCR Loans is that the qualification is based primarily, but not only, on the property that secures the loan. This is the opposite of the qualification for most conventional or other non-QM loan options. Those are based mostly on the individual borrower and less on the property. A key differentiator of DSCR Loans is that DTI ratio (or a comparison of the borrower’s personal income and total living expenses) is not taken into account, which allows DSCR Lenders to qualify loans for income-producing properties that simply make sense as investments, even if the borrower doesn’t have a stable day job (typically requiring W2 employment for two years) or other issues with DTI.

However, it’s critical to note that DSCR Lenders do take some aspects of the individual borrower into account for qualification, including credit score and liquid asset reserves. These affect qualification too, with the key takeaway that DSCR Loan qualification is based primarily on the property (but not completely). One persistent myth that has confused investors is thinking that DSCR Loans are “asset-based” loans or similar to the notorious “NINJA” or “no doc” loans. However, these are misconceptions as qualification for a DSCR Loan does include some aspects related to the individual borrower (credit and liquid assets) and there is plenty of documentation. True “asset-based” loans that are completely based on the property are not DSCR Loans and also fall into the broad category of hard money.

.png)

Next Up, check out Part 2 of our Guide: DSCR Loans vs. Conventional Loans!

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.