.png)

Figuring out where DSCR lending companies fit into the DSCR Loan ecosystem is challenging in and of itself; a messy spectrum between brokers on one side and insurance companies with massive portfolios on the other, with many different lending entities involved in some form or fashion with finding borrowers, qualifying, underwriting, pricing and closing the loans; and servicing, securitizing and eventually, holding and collecting the payments.

However, there is another confusing area where DSCR companies or lenders fit: that’s within the mortgage lending ecosystem itself. This is because while there are certainly “pure-play” DSCR Lenders or brokers; i.e. originators that offer DSCR Loans and DSCR Loans only, many mortgage lenders have DSCR Loans as a loan program among multiple offerings; which can include all sorts of different types of loans, including conventional loans, other non-QM loans and hard money loans. In addition, some DSCR Lenders may even mix structure and programs as well; for example, acting as a fully in-control direct lender for DSCR Loans while acting as a mortgage broker for hard money loan applications that come their way. The following will attempt to break down where DSCR originators may fit within the wider world of mortgage lending in the US.

The most common type of mortgage loans most people will encounter are conventional loan providers where “conventional” means that the loans will be sold to a Loan Buyer that is a government sponsored entity or “GSE,” typically Fannie Mae for residential loans. Instead of multiple loan buyers doing different securitizations with differing guideline sets like you will see in the “Non-QM” world, for conventional loans there is essentially one Loan Buyer and one set of guidelines: all conventional loans end up in what are referred to as Agency MBS or mortgage backed securities (via securitization) of loans originated with the same qualifications and underwriting.

As with DSCR lending, there are both mortgage brokers and direct lenders that offer conventional loans, with the biggest difference that the loan buyer and securitizer is the same: Fannie Mae. With relatively high capital requirements to sell directly to Fannie Mae, there may be additional aggregators involved, but they still aggregate to the same end buyer and securitizer, unlike the more diversified post-aggregation sources for DSCR Loans and Non-QM Loans. Bottom line, everything is more universal and tightly regulated, and all the providers of conventional loans, whether conventional broker or lender, will offer the same application forms, same loan options and same essential pricing, i.e. rates and fees.

By shopping around just a little bit, a real estate investor getting a conventional loan will likely be able to get the best rates and terms available – conventional loans are as close to the economic concept of “perfect competition” around – same thing offered everywhere, so rates and terms don’t really differ depending on the source.

Mortgage Lenders that offer conventional loans will also frequently offer other government-sponsored loan types such as FHA Loans which are backed by the Federal Housing Administration and VA Loans which offer subsidized terms for military veterans. Some mortgage lenders will offer these alongside standard conventional loan programs or choose to focus on these as specific niches. While these options provide significant benefits in terms of lower down payments and lower rates, they are not intended for “pure” rental properties, but are a popular option for investors utilizing the “house hacking” strategy (buying a 2-4 unit property, living in one unit while renting out the other(s)). A large mortgage lender like Rocket Mortgage will generally offer all the conventional loan options as well as these FHA and VA options for eligible borrowers. Veterans United Home Loans is an example of a niche mortgage lender focusing only on one government-subsidized loan type: VA Loans.

The other biggest type of mortgage lender is non-QM Lenders, which offer mortgage loans that are “non-qualifying” which in this context, means non-qualifying for conventional loans under Fannie Mae rules and guidelines. DSCR Loans are one of several Non-QM Loan Types so while a DSCR-only lender may technically be a “non-QM lender,” for practical purposes, non-QM Lenders generally refer to mortgage lenders that offer the “full suite” of Non-QM Loan options, not just DSCR Loans. To further muddy the mortgage waters, some non-QM lenders will have non-QM options along with conventional loan or government-subsidized loan options (i.e. FHA or VA), so they will be both! This is in line with the mortgage market theme, lenders fit in different spots on the spectrum and can overlap or be niche, and not so easy to put each mortgage lender you come across in a clean and neat box.

Here is a quick overview of the different types of “Non-QM” Mortgage Loans that are generally available (including for rental properties) in addition to DSCR Loans:

This is the closest thing to a “traditional” loan inside the non-QM world. A Full Doc Non-QM loan means the borrower provides the standard tax returns, W-2s, and pay stubs to verify income, just like a conventional mortgage. What are some reasons a borrower might be eligible for a “full doc” Non-QM Loan, but not an otherwise “full doc” conventional loan? Some examples would be borrowers with strong credit and compensating factors, but has a DTI slightly over 50%, making conventional loan qualification infeasible, or if someone recently switched from a W-2 role to a 1099 contractor role in the same line of work, but doesn’t have a full 24 months of self-employment required by conventional lenders. In these cases, the mortgage loan looks very similar to a conventional mortgage loan, but a non-QM lender can get exceptions or push past limits that are a hard “No” under Fannie Mae guides.

This is a common mortgage loan type for self-employed borrowers without a standard W2 income history as an employee. Instead of handing over tax returns (which often understate real income thanks to write-offs), the lender reviews 12 to 24 months of business or personal bank statements. They average out the deposits to calculate income. The catch? Lenders may apply an “expense factor” (say, assuming 40% of deposits went to business expenses), so the usable income might be less than the raw deposits. But for business owners and gig-economy borrowers, Bank Statement loans can unlock far higher qualifying income than their tax returns ever would show and allow borrowers to qualify for a mortgage loan without a steady “9 to 5.”.

This non-QM loan type functions similarly to Bank Statement Non-QM Loans and serves a similar borrower profile (self-employed individuals or business owners). Instead of submitting a mountain of statements, the borrower provides a year-to-date Profit & Loss statement prepared by a CPA or tax professional. The lender relies on the P&L as a snapshot of business income. The upside: much simpler documentation. The downside: lenders want to trust that CPA-prepared statement, so this option usually works best for borrowers with an established business and strong credit, and a knack for strong bookkeeping.

This one is for borrowers who might not show much income at all, but who have significant assets or savings. The lender essentially converts those assets into “deemed income” by applying a formula. For example, if the borrower has $1 million in liquid assets, the lender might divide by 120 months (10 years) and count $8,333 per month as qualifying income. This structure is particularly popular with retirees, people that recently “exited” or sold a business, high-net-worth individuals, or anyone living off investments rather than a paycheck.

This is a mortgage loan type for independent contractors and gig-economy workers who get paid on a 1099 instead of a W-2. Rather than reviewing full tax returns, lenders base income calculations on the past one or two years of 1099 forms. For rideshare drivers, consultants, freelancers, and other contract workers, this can be much cleaner and often shows higher usable income than what gets reported after deductions on a tax return.

Here, the lender verifies income directly with the employer through a Written Verification of Employment (WVOE) form, rather than combing through pay stubs and tax returns. This can speed up the process and is useful for employees whose income may fluctuate or who don’t want to track down endless paperwork. WVOE isn’t accepted everywhere, but where it is, it’s a streamlined solution.

Generally non-QM Loans can be used for both owner-occupied properties and rental properties. DSCR Loans are the unique non-QM option that is strictly for rental properties only. While some of the non-QM non-DSCR options can offer better rates and terms than DSCR Loans for financing rental properties, generally the difference isn’t much and the additional qualifying hoops to go through make it so typically if a borrower is financing an investment property with a non-QM Loan, it will likely be a DSCR Loan (with rare instances of the full-doc near-conventional non-QM options that have significantly better rates).

Many DSCR Loans that are securitized end up in Non-QM Securitizations, where DSCR Loans are mixed in with these other non-QM loan types, although there are DSCR-Only Securitizations that continue to make up a bigger portion of the secondary market. Since DSCR Loans generally don’t have too much in common with their other non-QM brothers and sisters, it’s likely that the securitization market for DSCR Loans continues to separate from the rest of non-QM and trend towards more DSCR-only securitizations in the secondary markets.

While offering the full non-QM suite of options versus only offering DSCR Loans seems like an appetizing opportunity, offering any sort of mortgage loan for owner-occupied real estate, even if not conventional, comes with an overwhelming amount of licensing requirements and regulations. Primarily due to the significant role that the mortgage lending industry contributed to the 2008 financial crisis, any company extending loans to owner-occupants, or “consumers,” is required to follow strict rules on disclosures, marketing and referral programs and loan officer (employee) compensation.

As such, a different class of lender, with many names but now primarily referred to as “private lenders” comes into play; defined here as mortgage lenders for residential real estate that stick to lending business-purpose or non-owner occupied properties only. As such, these private lenders actively make the tradeoff of not accessing the gigantic mortgage loan market of mortgage loans for consumers (borrowers who intend to occupy all or part of the property) for enjoying instead far enhanced freedom and flexibility in offerings and operations, with a vastly lesser licensing, regulatory and statutory burden of the much less regulated business-purpose only mortgage market.

Private Lenders, or mortgage lenders providing financing for residential investment properties only, include a good portion of DSCR Lenders. There are also some mortgage brokers that focus solely on business-purpose loans as well, as licensing requirements for even brokering or referring consumer mortgage loans can be strict as well. While there are a portion of “pure play” DSCR private lenders, or private lenders who solely offer one type of loan: DSCR Loans, there are many private lenders that will offer additional business-purpose loan types as well.

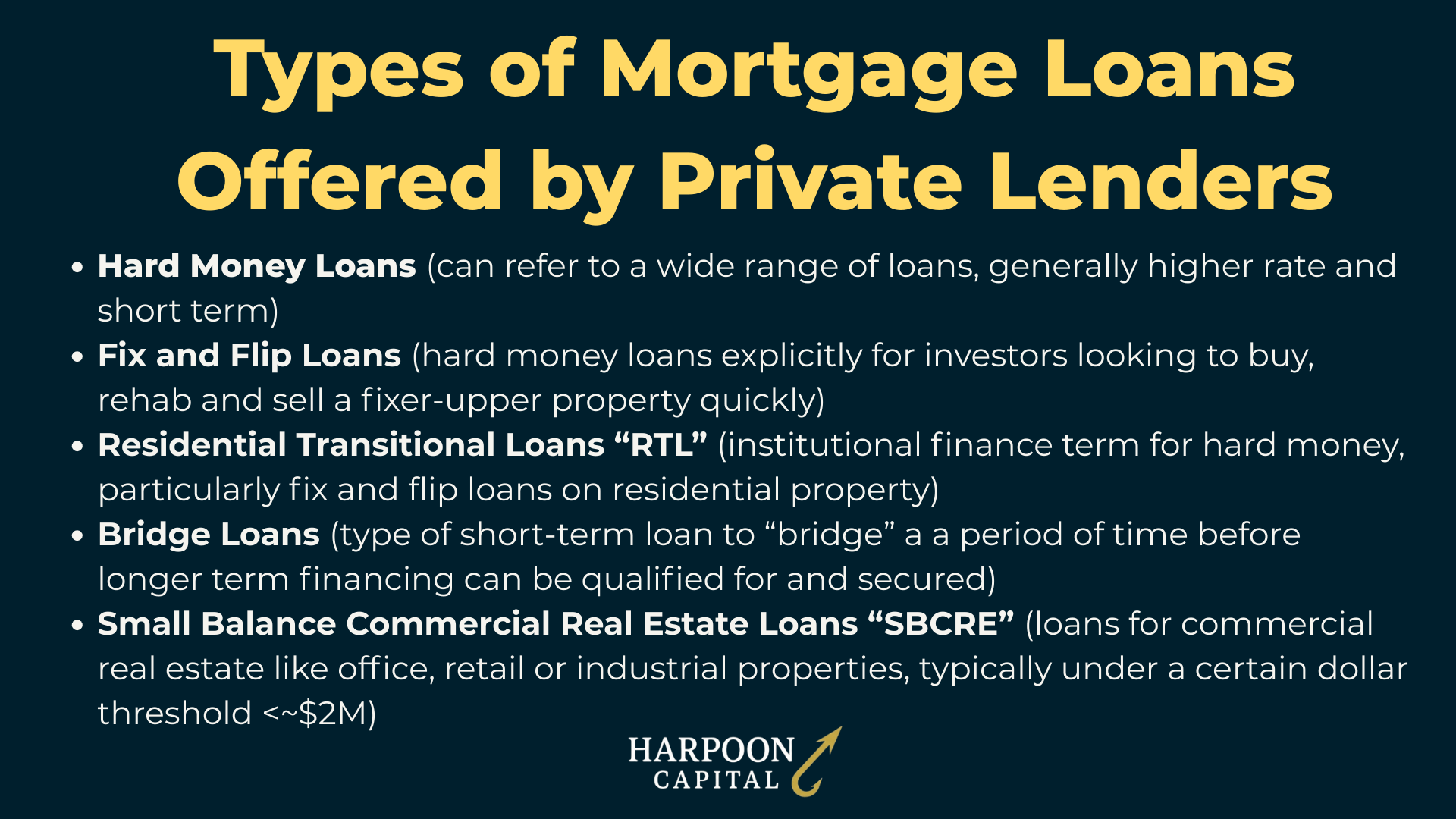

Hard Money Loans, which can refer to a wide range of loan offerings, most commonly describe short-term loans for the purpose of an investor doing a value-add renovation or rehabilitation of a residential property with the intent to pay off the debt quickly (less than one year). These are often also referred to as Fix and Flip Loans since the most common use case for these hard money loans are for the “fix and flip” real estate strategy of buying a property in need of rehab, doing a quick renovation and then quickly selling – or “flipping” it on the market. This strategy is quite common and well-known, as many TV shows and other media have glamorized the strategy to the masses. These types of loans can also be used for the BRRRR Strategy, or where the same investor at the same property can simply choose to refinance instead of flip once the renovations are complete. It’s a bit of a misnomer to call these loans “fix and flip loans” when the “exit strategy” could be flip or keep, but the loan looks the same and is for the same purpose: “buy and rehab.”

These loans, primarily in more finance-institutional and secondary market circles may be referred to as Residential Transition Loans or RTLs in institutional finance and secondary market circles, but these are the same loans, just with a fancier name. Because these loans are business-purpose (some conventional – i.e. Fannie Mae – renovation loans exist like the “Homestyle Loan,” but these are a very small portion of the market) and because with the rise of BRRRR in recent years the opportunity to do “two loans with one lender,” many private lenders will be structured to offer Hard Money Loans and DSCR Loans as their offerings.

Yet another name for this type of loan is Bridge Loan, which refers to a short-term “bridge” to finance the renovations or value add before the flip or refinance into long-term debt. Bridge Loans can also be a form of higher-rate short-term financing for properties not needing renovations, but rather just need a “bridge” in order to qualify for a DSCR Loan in the near-future, for example maybe if the borrower needs a mortgage late to roll off the credit report lookback period or needs an under-market lease to expire. This term is typically more used in commercial real estate investing, and most residential hard money loans are for true “value-adds” through renovation, but you may find these types of loans (and this name) in hard money loan program offerings as well.

These types of “bridge loans” will typically look very similar in form and substance to other hard money terms offered. Additionally, some of these lenders will also offer Ground-Up Construction Loans which look similar to hard money loans for residential flips – but provide financing for new build on a fresh land lot, instead of rehabbing a prior-existing property.

Small Balance Commercial Real Estate Loans, or “SBCRE Loans” are another offering from some private lenders in the residential space. While CRE lenders or lenders focused on commercial real estate loans for properties such as large multifamily, offices, industrial and retail properties typically fall into an entirely different industry and set of lenders than private lenders in the residential real estate lending space, there is some overlap in the area of small balance commercial which includes commercial real estate properties that are too small (i.e. low dollar value) for most commercial real estate lenders, but are also outside the wheelhouse of residential business-purpose real estate lenders, due to property type and even size. Small balance commercial real estate loans are generally in the loan amount range of $500,000 to $5,000,000 – and typically include properties such as small retail strip centers, single-tenant offices or tertiary industrial properties that are generally unloved by lenders and face financing needs.

Some enterprising companies attempt to serve this market in combination with a DSCR Loan program since there is some overlap in lending infrastructure (such as originations, underwriting and operations teams that can be cross-trained and utilized) and a similar lack of regulations and licensing requirements. It also serves a segment of the investor market that wants to “graduate” from residential real estate investing to commercial real estate investing by starting “small” and using a lender they know and trust (presumably the same lender they got DSCR Loans from for earlier residential investments).

Finally, there is a segment of the market typically referred to as Private Money (yes, very confusing with Private Lenders) where the key difference is that individuals invest in real estate through lending themselves, so at a high level, “private money” is getting real estate investment property loans from a person rather than a full-fledged company. Some investors have been attracted to going on the debt side of investing rather than owning and operating the properties themselves, typically after realizing that the workload and hassle of investing was not worth the extra reward, opting for the lower risk, lower work, lower reward aspects of lending. However, this option remains a tiny slice of the market at least for turnkey rentals – i.e. “private money” as an alternative to DSCR Loans, but can be a healthy alternative to hard money – since creative structures such as co-investing or quick financing arrangements are easier and more common in that space.

In summary, DSCR Lenders (and brokers) can take many forms and are not easy to place into specific and distinct boxes. Additionally, not all lenders are static in their offerings, some starting out with one certain loan type program and then expanding, or the reverse, cutting programs to focus in on key niches. However, at a high level, when working with a DSCR Loan provider, they will probably utilize one of the following structures:

Is one private lender structure better than the others for DSCR Loans? The answer to that is “it depends” with the answer having more to do with the particular lender rather than the lender’s structure. The answer can also depend on an investor’s particular long-term investment strategy or even where an investor is on in his or her timeline of portfolio building. If just starting out and considering “house hacking” or other non-100% rental properties, a full-suite non-QM lender might make sense. If it’s a heavy BRRRR method investor or someone that likes to mix flips with rentals, it likely makes sense to go with a lender that offers both DSCR and hard money. Flirting with expanding into commercial real estate to juice a portfolio? Well, you likely can finish this sentence yourself.

All that being said, “pure play” DSCR Lenders can be a great answer for many real estate investors, even if pursuing other strategies and financing types like RTL and commercial, as these lenders have total focus on DSCR Loans and are custom-built for the trickiest situations and newest needs (like first to adapt to tailoring guidelines around short term rentals or small multifamily). Additionally, a huge “behind the scenes” insight is that lenders will create and invest heavily in Loan Origination Systems (or “LOS”), operating structures and technology around their offerings. Lenders that have multiple loan type offerings (i.e. not just “pure play” DSCR Lenders) will often try to “jam” together the interfaces for DSCR Loans into the same systems as residential consumer loans, hard money loans and/or commercial loans, each of which have many aspects that are different and contradictory to a fully efficient and optimized DSCR Loan program.

When this happens, as any “tech integration” professional will tell you, there are tradeoffs and sacrifices, and the system optimizes for scalability and fitting all the different loan program square pegs into one round hole, usually producing sub-optimal results. For this reason, DSCR Lenders purely focused and built around DSCR Loans, a loan product that is both growing significantly and has unique structures, needs and tailoring, often have the best and smoothest DSCR Loan borrowing experience with the highest borrower satisfaction and certainty of close.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.