.png)

Despite the allure of conventional loan options for short term rentals, the benefits, from lower down payment limits and lower rates and fees are mostly a mirage, as the numerous hurdles, drawbacks and downsides as compared to DSCR Loans emerge when digging in a little deeper. DSCR Loans, when adding on significant prepayment penalties (usually not an issue with STR investors looking to build portfolios who are not too concerned with selling anytime soon), the rates and fees for DSCR Loans can even be equivalent or even lower than their subsidized conventional brethren. It’s no wonder then why so many real estate investors focused on the short-term rental strategy utilize DSCR Loans as the financing method of choice.

However, when it comes to DSCR lenders for STR Loans; all are not equal. While the rough groupings of 1) Anti-STR 2) Moderately STR-Friendly and 3) STR-Friendly still generally hold in 2025, the industry and individual lender guidelines and policies continue to evolve and change all the time, so the well-informed STR investor and DSCR Loan should be prepared to evaluate DSCR Lenders for short term rentals by clarifying and confirming the key policies and methods where they may differ.

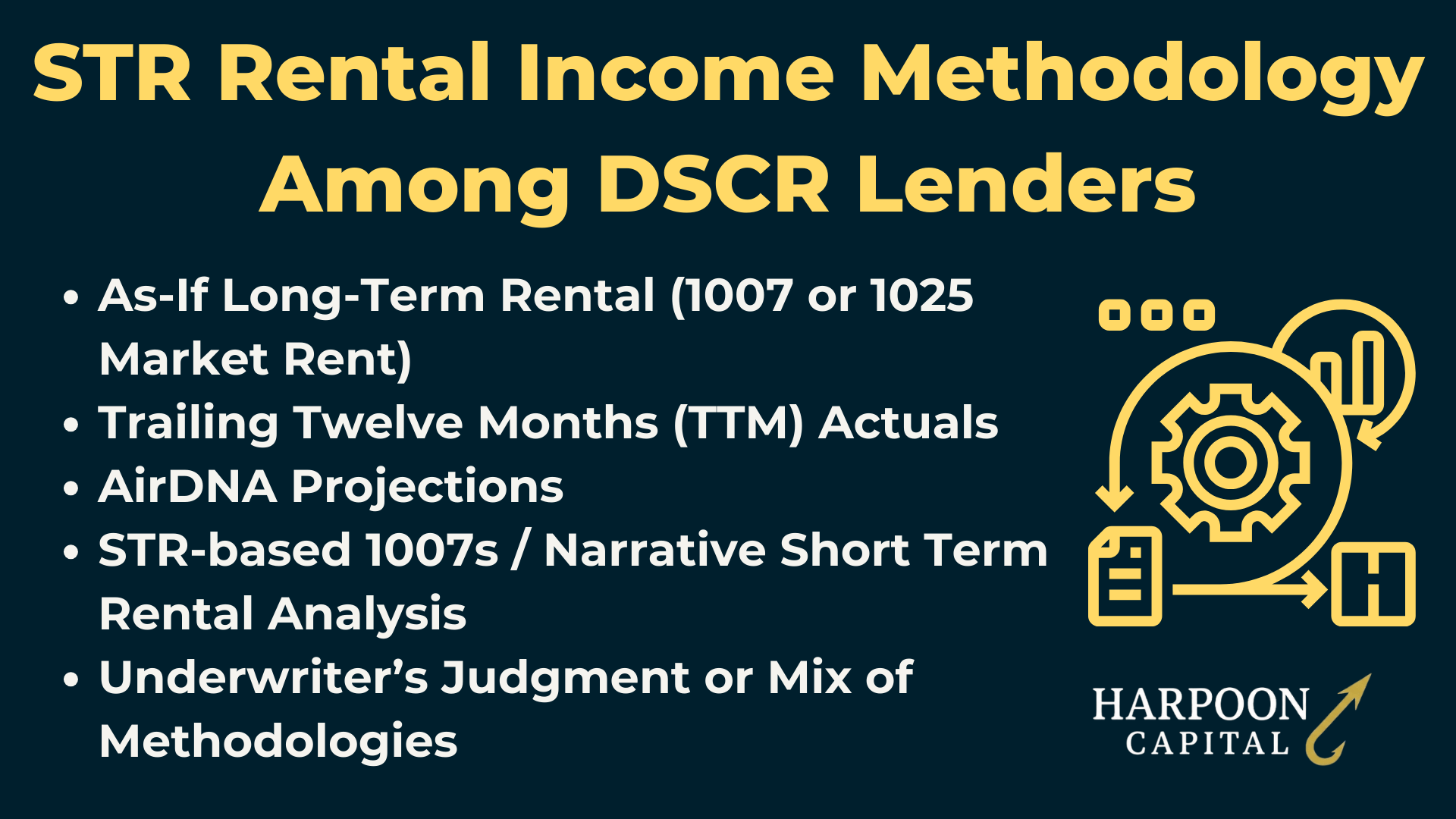

The single most important (and diversified) aspect of STR lending among DSCR Lenders is how they come up with the revenue number for qualification (i.e. the numerator used in the all-important DSCR ratio). It can often mean the difference between the DSCR Loan itself qualifying or not, and the particular method or methods used by different DSCR Lenders can vary significantly.

There are multiple methods for qualifying rental income common among DSCR Lenders, here are the possible STR rental qualification methods utilized for DSCR Loans:

Almost every single DSCR Lender will allow qualification for a short term rental based on the equivalent market rent for long-term rentals (found on the 1007 or 1025 addendum to the independent appraisal report). This is the most conservative methodology (LTR market rents tend to be much lower than potential STR income) and is allowed by all but the most steadfast anti-STR DSCR Lenders.

The only hiccup or potential issue you might encounter with this rental income methodology is on a refinance transaction, as most DSCR Lenders add a couple of verification measures to ensure occupancy fraud isn’t occurring (i.e. using “it’s an STR” as an excuse for an unleased refinance transaction where the borrower was fraudulently actually planning to occupy the property). But otherwise, an STR that still qualifies as an LTR will almost always be smooth sailing with any DSCR Lender.

The original qualification methodology that sparked DSCR Loans as the top option for short term rentals is still around and a common option for lenders. However, it’s important to note that this is typically only allowed for refinances and not acquisitions, since what’s important is that it’s the borrower’s history rather than the property’s history. Since the lender wants the comfort of the operator’s ability to recreate the past years’ performance, using the seller’s past performance is generally not allowed. There are maybe a small handful of DSCR Lenders that may offer TTM Actuals qualification for buyers (acquisition loans), they are few and far between in 2025, and would likely need very strong extenuating circumstances (such as a highly experienced borrower, the borrower keeping management company, cases where the buyer was previously managing the property or doing “Airbnb arbitrage” et cetera). Note that this is yet another example of how DSCR Loans are really about far more than just the “property” and not just another form of “asset-based” lending – borrower, and borrower experience matters in all sorts of places!

It’s also important to note that this measurement is for gross income only, and typically does not include deductions for operating expenses, even management fees that can be quite substantial. While this may appear to be a little reckless and liberal on the part of lenders – that’s a valid point. However, this is another example of the borrower-friendly aspects of DSCR Loans for STR investors and a stark contrast to conventional lenders that rely on tax returns that can sometimes be extremely unforgiving towards “real” STR income, or what is put on tax returns intended to take advantage of any and all allowable deductions, saving STR investors valuable money, but underselling performance on paper – and in conventional lenders’ underwriting files!

As of 2026, a DSCR Lender’s policies and usage of AirDNA projections for qualification and underwriting STR Loans is the key question to confirm when evaluating “STR-friendliness.” Over years of data now, the projections created via AirDNA have proven to be if not perfect; accurate, reliable and conservative. While as short a time ago as 2022 only a small portion of DSCR Lenders were ahead of the curve qualifying STR Loans with AirDNA projections, by 2026 it’s more like a majority. However, key distinctions remain and are important, particularly on haircut policies for AirDNA Projections (i.e. what percentage of the AirDNA projections “count” towards qualification) and the projections policies by loan purpose (i.e. if AirDNA can be utilized for refinances).

Generally, most DSCR Lenders that utilize AirDNA projections will now use a blanket 80% of the projected rental income – or a 20% “haircut” – which in practice means taking the Rentalizer number and reducing it by 20% (or multiplying it by 0.8). Some lenders will adjust haircuts by experience level, for example giving the full 100% of AirDNA projections if they qualify as a “professional STR investor” defined as owning a STR with 12-month history in the same market or three or more STRs with history nationwide, and without this “professional STR” qualification, use the standard or even more aggressive (i.e. 75% of projections) haircut.

AirDNA projections have typically been used to qualify acquisitions, however the question becomes a little trickier when it comes to using projections to qualify STR income on refinances. Typically, this will come up for borrowers looking to refinance a STR that was recently renovated and now is fully fixed and up and running ready to be a fully operational Airbnb. Many investors that use this strategy, the so-called “AirBnBRRRR” or “brrrSTR” method; will use high-rate hard money to finance the purchase and renovations, and are loathe to wait a full 12 months saddled with high-rate interest and extension costs building up a TTM Actuals history to refinance. And the LTR-based 1007 market rent doesn’t work to qualify the loan, so qualifying with AirDNA projections becomes the only feasible option.

For these “AirBnBRRRR” investors, being able to use AirDNA projections on refinances has been a godsend; as it allows these deals to not only pencil; but to provide some of the highest returns in real estate investing by combining the two lucrative strategies of STRs and BRRRRs with a tailor-made financing solution. Note that the DSCR Lenders that allow AirDNA projections to be used on these refinances (a smaller subset of the STR-friendly DSCR Lenders that use AirDNA in general, i.e. for acquisitions) typically will have some mild additional safeguards in place to protect against mortgage fraud or refinances before the property is truly ready, often requiring a proof of listing documentation and at least one completed or in-progress booking to close.

STR-based 1007s, or when the lender instructs the appraiser to determine a market rent based on short term rental usage instead of traditional long-term rental rates, continue to go out of favor among DSCR Lenders in 2025 and are essentially obsolete in 2026. This is primarily related to many DSCR Lenders finally coming to embrace AirDNA, as the main reason to gather STR-based 1007 reports – if boxed into only utilizing an appraisal for projecting STR income - fades away. However, some DSCR Lenders are still utilizing 1007 appraisal market rents based on short-term rents to underwrite and qualify STR rental income.

The use-case and reasoning for this methodology makes sense in certain cases, particularly long-time vacation rental markets like Ocean City, Maryland and Block Island, Rhode Island, where properties have long been utilized as short-stay or weekly/monthly vacation rentals, but the market is still dominated by independent booking sites and management companies rather than listings on Airbnb. In these cases, these local comps, especially if the norm in the area is week-long or month-long stays, can be stronger than the AirDNA projections which are still primarily driven by Airbnb listings and newer hosts.

Additionally, some properties, especially large luxury properties in smaller markets where most comparables are significantly smaller in size (for example an eight-bedroom mansion in a ski town generally filled with two-bedroom condos or small houses) or in cases where true guest count potential doesn’t match up with “legal bedroom definitions” in the jurisdiction, individual judgment from a local appraiser can be superior. But as DSCR Lenders become more and more comfortable with AirDNA, and the vacation rental industry continues to consolidate and modernize (with more online and algorithmically optimized booking systems), it’s likely STR 1007s continue to decline in relevance and usage for DSCR STR Loans, essentially being replaced with the new Narrative Short Term Rental Analysis.

Finally, some of the most established, long-time STR-Friendly DSCR Lenders have progressed towards using a more “holistic” underwriting approach to determining underwritten STR rental income, meaning a more professionalized judgment and analysis of multiple sources, such as using AirDNA, the borrower’s portfolio and experience and downside-case long-term market rents to come up with judgment-based numbers. This is more akin to traditional, larger-scale commercial real estate lending such as for large office buildings or apartments with many floors and tenants, where coming up with projected rents and incomes isn’t so simple as looking at a unit or two. As the STR industry matures, it’s likely that this more sophisticated, high level approach will become more common.

Q: How do DSCR Lenders decide what income to use for an Airbnb or STR property?

A: It depends on the lender. Some use conservative “as-if long-term” rent comps, while others accept trailing 12-month booking history, STR-specific appraisals, or even AirDNA projections. The method matters, it can mean the difference between qualification or a dead deal, and can play a large role in interest rate, leverage and points and fees as well.

Different DSCR Lenders may also have additional or layered experience requirements for STR Loan qualification. Beyond the fairly standard “first-time investor” and “first-time homebuyer” restrictions and requirements, direct short term rental experience or simply a higher level of overall real estate investing experience may play a role in qualification, underwriting methodology and eligibility for STRs for some DSCR Lenders.

The primary way that DSCR Lenders will utilize STR-specific experience, however, is related to whether qualification through AirDNA projections is allowed (typically the most-sought after rent qualification among investors since it will qualify the loan with the highest potential revenue). Some pioneering lenders in the space used the “STR professional” qualification which targeted top-tier STR owner operators to lend to – such as qualifying with 100% of AirDNA projections with the following experience requirement:

Other ways DSCR Lenders may use experience requirements for STRs may be to restrict “first-time investors” to long-term rentals only, or provide additional LTV restrictions (on top of rental revenue restrictions) for borrowers without STR experience (i.e. 5 or 10% LTV overlays, or cuts to what would otherwise be the maximum leverage offered).

So-called “condotels” are an emerging asset class that further blurs the line between hotels and short-term rentals. Condotels are a special form of condo in which a building is purposely-built to cater to investor-owned units and short-stays – it’s essentially a hotel in which the rooms are individually owned and operated by individual owners rather than one centralized hotel owner. The buildings typically have a front desk and other shared services amenities, with the infrastructure purposely designed to cater to short-stay guests (and the investors who own the units and serve them).

Traditionally, DSCR Lenders who offered STR Loans on condos had strict prohibitions on units in buildings like these – as any sign that a property was not truly residential (i.e. could be easily utilized as a residence for long-term tenancy, either tenant-occupied or owner-occupied) was off limits and too close to commercial. So, any STRs that had a whiff of a front desk, commercial booking system or a true “bed and breakfast” type arrangement were not allowed for DSCR financing. While that still holds true today for standalone properties – generally SFRs used as bed and breakfasts or small motel-like multi-unit properties are still fully ineligible – some DSCR Lenders have embraced financing these condotel units (used as short-term rentals) as a good fit.

For borrowers interested in investing in short term rentals within condotels, it’s important to dig in and understand the differing DSCR Lender treatments for condotel unit STRs. Generally, as of 2025, only a minority of DSCR Lenders will lend on condotel units, probably around 25-35% of lenders. Many lenders that have come to cautiously embrace STR Loans will still restrict their programs to short term rentals on traditional 1-4 unit properties and standard condo units (either warrantable or non-warrantable, but still in buildings that are designed for and primarily owner-occupied or long-term rental units). In addition, DSCR Loans for condotels (among the lenders that offer them) will typically have additional LTV restrictions (such as maximum LTVs of 65.0% or 70.0%) and somewhat higher pricing (interest rates and fees). This is to compensate for the elevated risks as these buildings are uniquely vulnerable to two enhanced risk areas: both condos and short-term rentals.

Another property type question that comes up mixed with short term rentals is potential eligibility for STR DSCR Loans for Multifamily (5-10 Unit) properties. Generally, the answer is that these are universally ineligible among DSCR Lenders. While it may seem silly that a four-unit short-term rental would be fully eligible while if it has five units it’s off limits, that’s the current (2025) reality for DSCR Lenders. More than four units generally seems too close to “motel” or “boutique hotel” territory than true residential and thus for now, DSCR Loans for short term rentals on five-plus unit properties are almost always ineligible. There may be DSCR Lenders that dip their toes into this area, but borrower-beware, if you see this advertised, it’s advisable to dig in very deeply with questions and confirmations on if this qualification is fully true and not a bait-and-switch scheme.

A growing niche in the STR space is the medium-term rental (MTR), furnished properties generally rented for one to three months, often to traveling nurses, consultants, or families in transition. These sit in a gray zone: not quite traditional year-long leases, but not nightly STRs either.

Generally, DSCR Lenders are amenable to offering DSCR Loans on MTRs, however the rent qualification for this strategy is still murky, as there doesn’t really exist an “AirDNA” equivalent for projecting rents for medium term stays. While the general rule of thumb is what you’d expect: MTRs generally earn an amount in the “middle” between what a property would earn as a long-term rental and short-term rental (i.e. 1.5 times as much as an LTR instead of twice as much for STRs), most lenders prefer not to qualify rents on thumb-based rules.

Most DSCR Lenders will be flexible on qualifying DSCR Loans for mid-term rentals using the 1007 market rent or AirDNA projections for acquisitions and the TTM Actuals of the MTR activity for refinances. Where it can get tricky is for refinances or situations where the property is currently under a medium-term lease (i.e. loan closing in the middle of a 90-day booking); in these cases, it’s both hard for the DSCR lender to extrapolate the 90-day rate for a full 12-months) but also difficult to use projections or STR market rents for a property that is in fact tenanted on longer-than-typical stays than normal STRs. In these cases, DSCR Lenders may have to default to conservative underwriting standards such as utilizing long-term market rents or the like. If investing in medium-term rentals and looking for DSCR financing (which is still likely the top loan option for MTRs), it’s best to discuss these details and finer points early on in the process to fully understand the particular lender’s methodology and treatment; as mid-term rental DSCR Loans are the likeliest to fall into the “case-by-case” or judgment-based underwriting and qualification among lenders.

Up Next: Common Nuances and Pitfalls in STR Lending

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.