.png)

The settlement statement, whether labeled an ALTA Settlement Statement, HUD-1, or simply “Closing Statement,” is the master accounting sheet for your DSCR Loan closing. In DSCR lending, the lender and title/escrow company work together to make sure it is “balanced,” meaning every dollar in and every dollar out is accounted for and matches exactly.

A balanced statement will include the following major sections, each of which you should review line by line and should be received for review at least a couple of days before closing.

This section shows the loan amount from your new DSCR Loan. This is the starting point for calculating how the funds flow. Note that sometimes in real estate lending, particular financing for larger commercial or multifamily properties, there can be concepts called “holdbacks,” where a portion of the loan is “held back” by the lender to be doled out specifically for a certain use, such as a planned renovation or to pay leasing costs to fill the property. However, there are no lender holdbacks for DSCR Loans, and this section should simply show the full loan amount (matching what’s on the loan documents).

The next section will show any existing mortgages or liens, i.e. the payoff amounts to any current lenders or lienholders. These should match the payoff letters ordered by title/escrow. This section can also include any other property debts such as outstanding HELOC balances, judgment liens, tax liens or mechanics’ liens that must be paid off in conjunction with the new DSCR Loan.

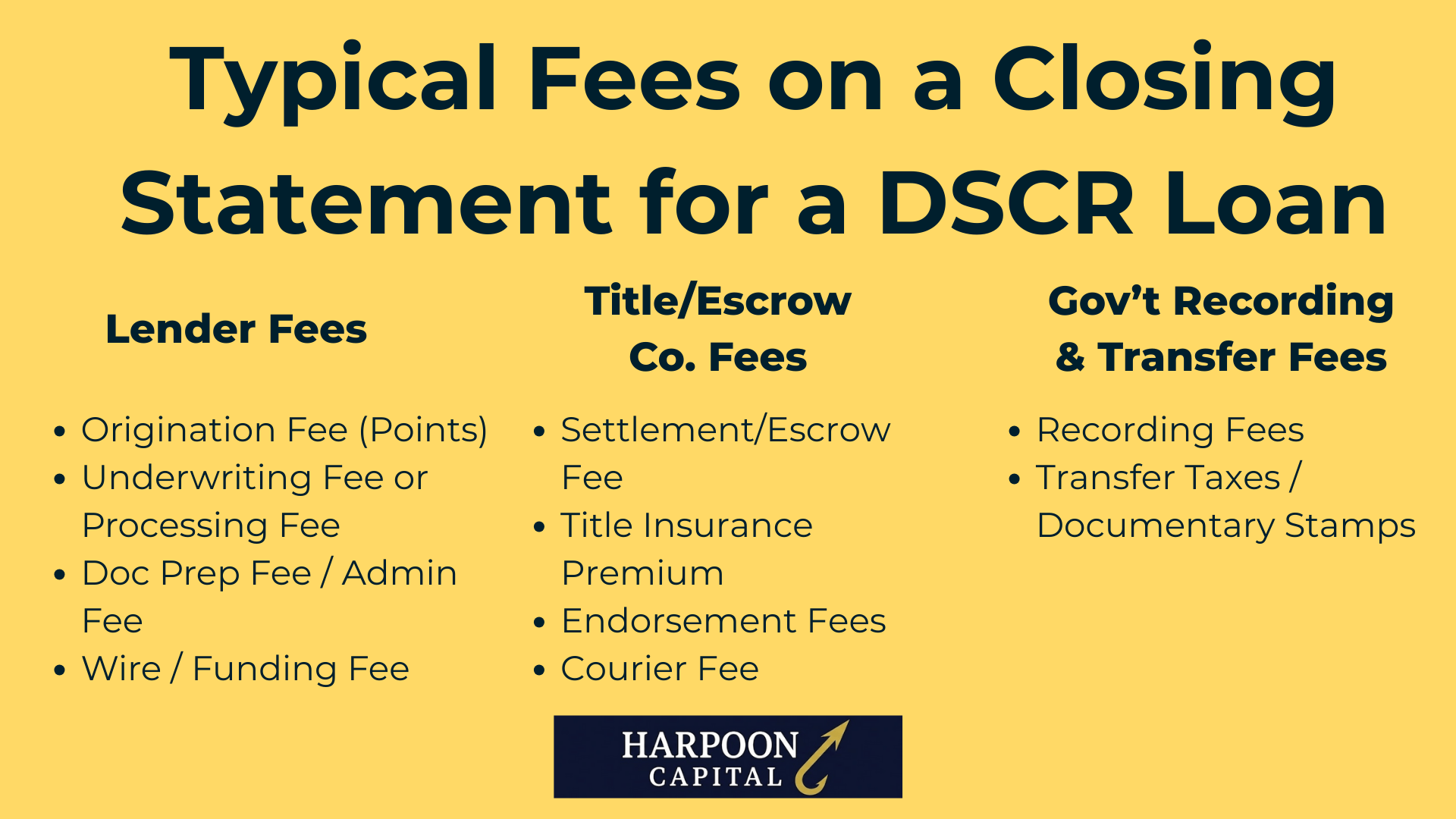

This section covers fees due at closing and generally is split into three parts:

These include any fees charged by the DSCR Lender or mortgage broker for originating and processing the loan. Some lender fees that may commonly be seen on a settlement statement for a DSCR Loan include:

These fees are to the title company for handling the settlement, ensuring clear title, and issuing title insurance. These vary by state, county and loan size.

These are fees paid to county or local governments for recording the new lien and in some areas for transferring property ownership.

If your DSCR Lender requires escrows for property taxes and insurance (common but not a universal requirement), initial escrow deposits for property taxes and property insurance will show up in this section.

Credits are amounts applied against total costs at closing, reducing the cash needed to bring to the table on acquisitions or rate-term refinances. On your settlement statement, they’re shown as positive amounts, typically offsetting the fees found in section three.

Prepaid interest, also called “stub interest,” covers the daily interest that accrues from your closing date through the end of that month. It ensures that the first regular payment covers a full month’s interest, not a partial month. For example, consider a DSCR Loan closes on June 10 with an interest rate of 7.500% and a loan balance of $500,000. The daily interest is about $102.74 ($500,000 × 0.075 ÷ 365). If there are 21 days left in June, the prepaid interest is $2,157.54 ($102.74 × 21), paid at closing. The first full payment will then be due August 1, covering all of July’s interest (and any principal if amortizing).

This is the bottom-line figure that tells you exactly what is either owed at closing (if you’re bringing money in, for acquisitions and certain rate-term refinances) or the cash received at closing, for cash-out refinances and other rate-term refinances. This “bottom-line” number is essentially a long arithmetic problem flowing from the top section.

For acquisitions, it essentially starts with the purchase price, subtracts the new loan amount and any credits and adds all the associated fees, escrows and prepaid interest to find the total cash number needed to “wire in” to complete the purchase. For refinances, it is a similar math problem, but starts with the new loan amount and subtracts any and all payoffs (including a current mortgage loan), as well as fees, escrows and prepaid interest, and then adds back any credits to determine how much money is released in proceeds. If this number is negative, it is a rate-term refinance (sometimes nicknamed “cash-in” refinance), where to secure the new DSCR Loan, additional funds must be wired in to cover the shortfall.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.