.png)

Liquid Assets documentation serves two functions for DSCR Loans. First, it serves to confirm the borrower has funds for cash to close, such as enough money for down payments for acquisitions and any needed cash to “bring to the table” on rate-term refinances where new loan proceeds don’t fully cover payoffs, escrows and closing costs (i.e. “cash-in refinances”). Second, it confirms liquid asset “reserves” to show that the borrower has a “cushion” of funds to personally cover the debt payments in months where the property doesn’t generate enough cash flow to cover the PITIA payment for whatever reason, whether due to unexpected vacancies, seasonal variation in short stays or even if the loan is underwritten with a sub-1.00x DSCR ratio in the first place.

The amount of these liquid asset “reserves” will vary from lender to lender, but are typically calculated in “months of PITIA” for the DSCR Loan itself and range from two months of PITIA payments to up to nine or even twelve months in certain high-risk situations. An example of this would be if the DSCR Lender requires “3 Months of PITIA” of liquid assets reserves and the monthly PITIA payment is $2,500, then the required liquid asset reserves would be $7,500 ($2,500 x 3 = $7,500).

Additionally, DSCR Lenders include sourcing of funds review for this documentation set and must ensure that money came from an allowable source and not from ineligible channels such as undisclosed loans, unverified cash or prohibited third parties. This is a requirement to do due diligence in preventing DSCR Loans being used for money laundering or other illicit activities.

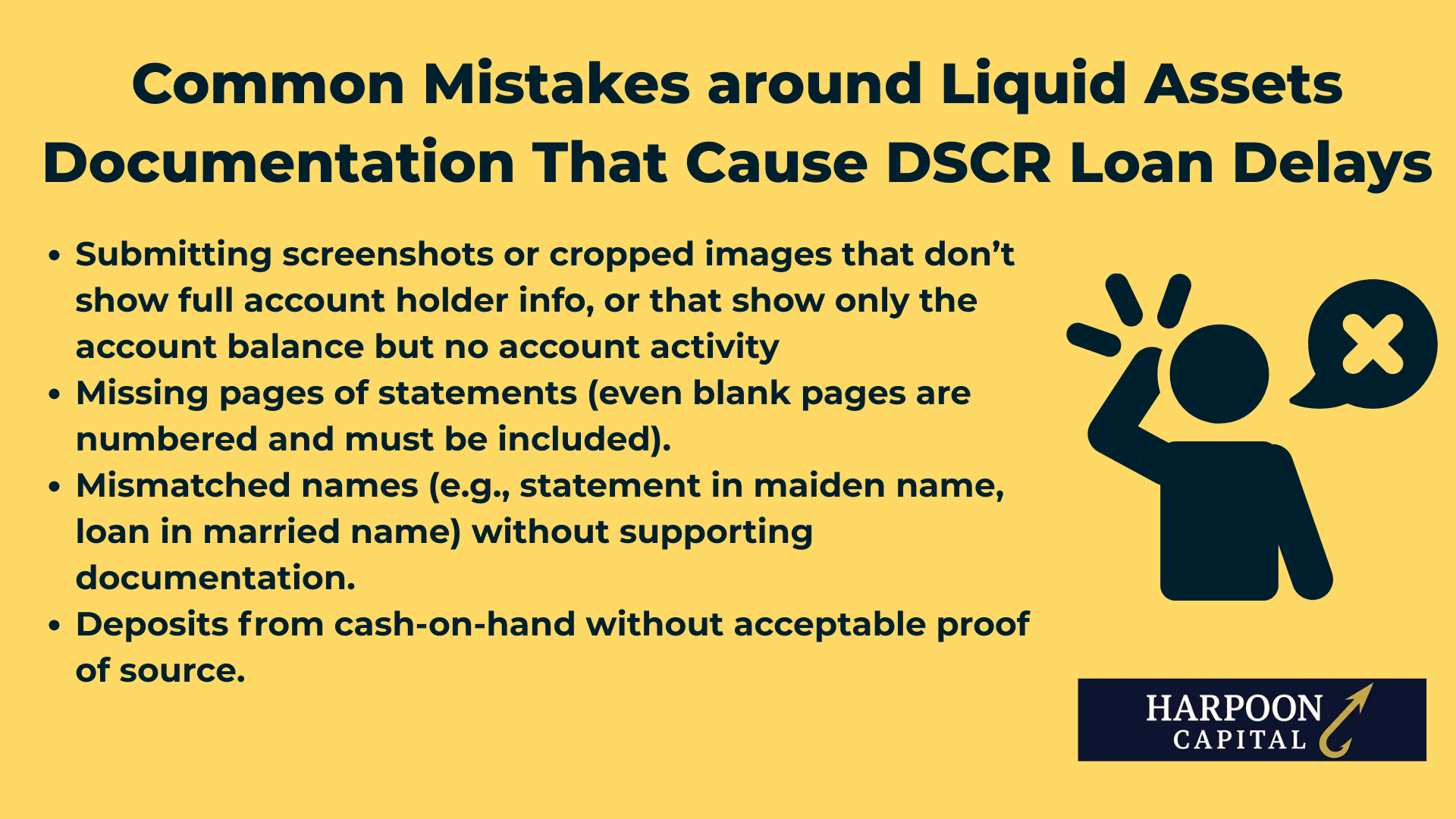

When your DSCR Lender asks for “bank statements” or “account statements,” they mean full, official statements showing all required details, not screenshots or partial exports. In most cases, documents must be full account statements for the previous two months prior to the month in which the loan closes. Typically, since most accounts issue monthly or 30-day statements, borrowers must provide two statements (two monthly statements) for each account utilized. Note that a common occurrence for DSCR Loans is the closing date “pushing” into a new month (i.e. the planned closing date moves from one month to the next one) and in these cases, will typically require providing new and updated monthly statements.

Accepted formats for DSCR Loan liquid assets documentation include Official PDF statements issued by your bank, brokerage, or custodian. Online downloads from the institution’s secure portal are also typically acceptable, but usually must show the account holder name(s), institution name, full account number (or at least the last four digits), statement period and all transactions. Quarterly statements (covering 90 days’ worth of activity) are acceptable for accounts that only issue quarterly reports (e.g., certain retirement or brokerage accounts), but must be the most recent available.

Every account statement submitted for liquid assets documentation for a DSCR Loan should show:

The good news for borrowers is that “liquid assets” encompass far more than just cash held in simple bank checking or savings accounts. There are many types of financial accounts that can be used for liquid asset reserves documentation for DSCR Loans. However, there are some nuances to the specific documentation requirements needed depending on the specific type of account used for liquid assets documentation. Bank Accounts (Checking/Savings/Money Market) simply require the two most recent consecutive months of statements. All pages must be included, even if some are blank or contain only disclosures. Brokerage Accounts (Stocks, Bonds, Mutual Funds) require the two most recent monthly or most recent quarterly statement, if applicable. Certificates of Deposit (CDs) must typically show maturity date and balance; early withdrawal penalties may be considered in reserve calculations. Life Insurance Policies can be used as well, but the value utilized for reserves is limited to the terms of surrender from the issuing institution.

If utilizing Retirement Accounts (401(k), IRA, 403(b), etc.), the most recent statement (if quarterly) or statements (if monthly) showing vested balance is required. Typically, a “haircut” is applied to account for penalties and taxes, so documentation around the vesting/penalty specifics on these accounts should always be provided. Note that if a loan secured by the assets in these accounts is outstanding, the amount owed on the loan is subtracted from the current vested balance for the DSCR Lender’s calculation. While it’s still relatively rare, some DSCR Lenders will allow Cryptocurrency Holdings for liquid asset reserves documentation, but likely will be required to be held at a major exchange like Coinbase or Gemini (and not a personal wallet). The crypto exchange statements must show ownership, coin type, and value in USD at statement date. Note that haircuts can be substantial if a DSCR Lender allows these for liquid assets, and would typically only be permitted for major currencies like Bitcoin, Ethereum and Bittensor.

Business Accounts for entities that are different than the borrowing entity are typically only allowed if the individual guarantor owns 100% of the business or has written authorization from all owners. A CPA or account signatory letter may be required confirming that withdrawal will not negatively impact operations and there might be an additional set of attorney entity documents review (including costs) of the business’s entity documents (i.e. Operating Agreement, etc.) by the DSCR Lender to confirm ability to use and access these funds. If Trust Accounts are utilized, a statement plus trust agreement or trustee letter confirming borrower’s access to funds and ability to use them for the transaction will likely be required.

DSCR Loan underwriters will generally flag any large or unusual deposit in statements used for liquid assets documentation. While definitions vary, any deposit that’s $10,000 or more, a significant percentage of your balance or that seems out of pattern will trigger a sourcing requirement. For these large deposits, you may be asked to provide additional documentation such as a copy of the check, wire confirmation, or transfer statement, documentation of the original source (e.g., sale of property, investment liquidation, tax refund) and most likely a signed Letter of Explanation (LOE), explaining the context of the transaction(s). New accounts opened within 90 days of the loan application also require an explanation and sourcing for the initial balance. Unverified or ineligible funds will be excluded from the liquid assets reserves calculation.

Doctoring or providing falsified liquid asset reserves are two of the most common forms of mortgage fraud, especially in an era of technology or AI-powered editing tools that can fool even the most scrupulous underwriter. For these reasons, the documentation requirements and rules can be heaviest in this area, and cutting corners on full and complete requirements will often cause problems. Some examples of seemingly small liquid asset documentation issues that can lead to re-sending and deal delays include:

For investors aiming for the smoothest possible process, and especially for deals with a time crunch, it’s best practice to provide complete, clearly labeled PDF files in your initial submission. Name files with the property address, account type, and month/year (e.g., “123MainSt_Checking_Jun2025.pdf”). The clearer your documentation, the fewer back-and-forth requests you’ll face, and the faster underwriting can move your file forward.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.