.png)

Because your DSCR Lender is likely a national rep and won’t be at closing, and that DSCR Loans don’t fall under the myriad of regulations and disclosure rules that accompany consumer or conventional loans, it’s extremely important as a best-prepared borrower to have a solid understanding of the documents you may be required to sign before sitting down at closing with everything on the line.

To assist, here’s a comprehensive list of the kinds of documents you may see and sign at closing, especially if your DSCR Lender does not use a holistic loan agreement. In those cases, many provisions are broken out into individual documents, so the final loan package can be 80–100+ pages with a long checklist of separate forms. All the documents required to be signed by the borrower(s) or borrower(s)’s authorized signatories are typically called the Loan Closing Package. Each of these plays a specific role in the transaction.

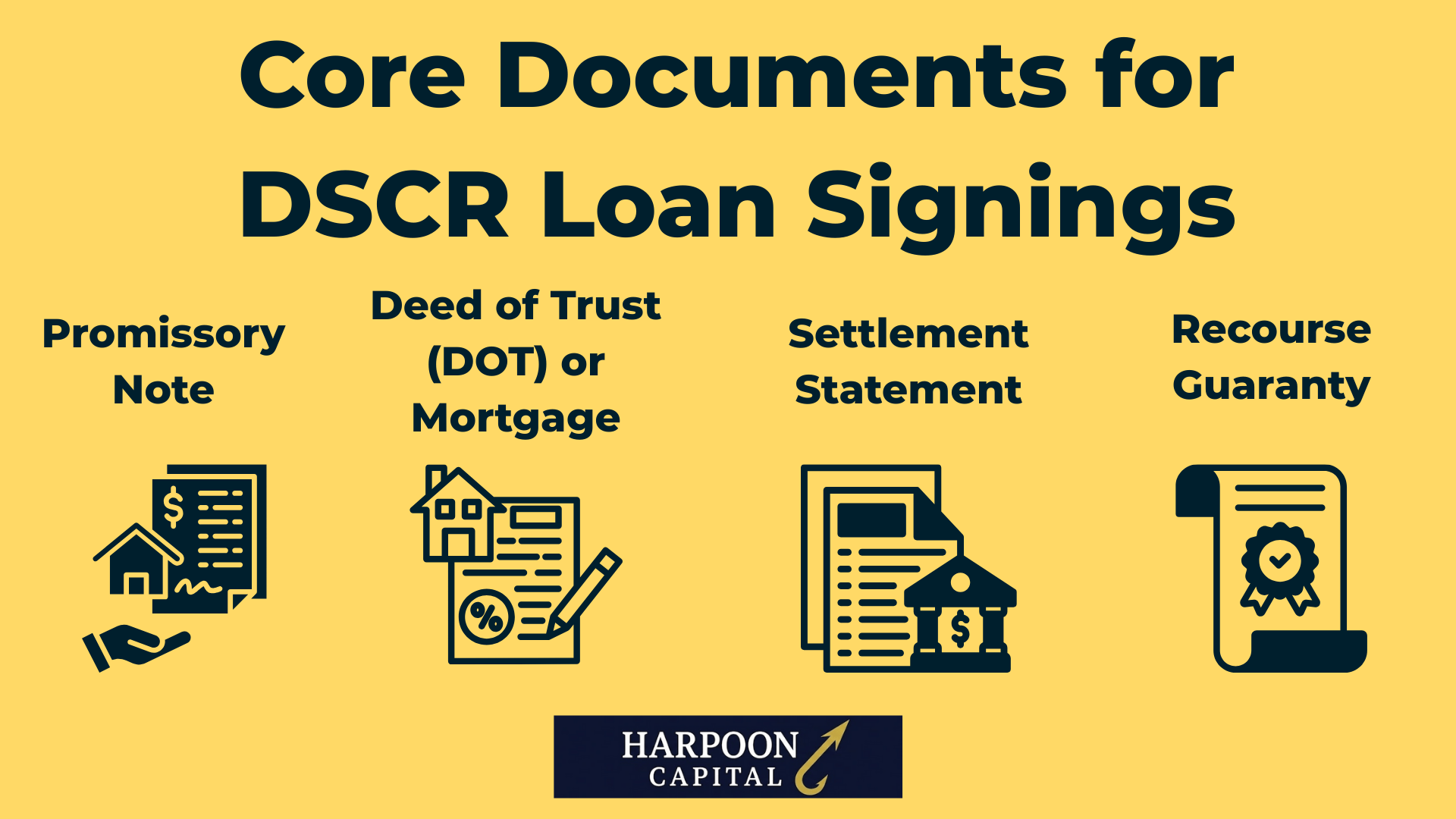

These are the primary, non-optional loan documents that form the legal backbone of your DSCR Loan closing documents. Together, they establish the repayment obligation, secure the lender’s interest in the property, and document the agreed-upon financial terms of the transaction. Every borrower, whether closing in person, remotely, or through an attorney, will sign some version of these, though specific formats and naming conventions can vary by lender and state. The “core documents” typically include the promissory note, the security instrument (either a Deed of Trust or Mortgage), a settlement statement and typically a personal guaranty document (although this is only needed when the borrower on the DSCR Loan is an entity).

The Promissory Note is the primary repayment contract between the borrower and the DSCR Lender. It specifies the exact loan amount, interest rate, payment schedule, maturity date, and what constitutes a default. The promissory note, or sometimes just referred to as “the Note” is enforceable on its own and typically contains all the major and relevant information needed.

The “Deed of Trust” or “Mortgage” is a document that secures the DSCR Lender’s interest in the property, i.e. the “security instrument,” allowing them to foreclose if the borrower defaults. It typically includes borrower covenants like paying taxes on time, keeping insurance in force, maintaining the property and allowing lender inspections if needed. The specific name of this document, i.e. “Deed of Trust,” sometimes abbreviated to “DOT,” or “Mortgage” varies and depends on the state the property is in and the differences, while minor, are typically based on the court involvement in cases of foreclosure, with “Deed of Trust” in most non-judicial states and “Mortgage” in judicial foreclosure states.

Q: What’s a Deed of Trust for a DSCR Loan?

A: A Deed of Trust is the legal document that secures a DSCR Loan against your property, giving the lender the right to foreclose if you default. Used instead of a mortgage in certain states, it involves a third-party trustee who can handle a faster, non-judicial foreclosure process if needed.

For DSCR Loans, the “security instrument” signed will be either a Deed of Trust or a Mortgage, depending on state law. Both create a lien on the property and give the lender the right to foreclose if you default. The main difference is in the foreclosure process: a Deed of Trust generally allows for faster, non-judicial foreclosure through a trustee, while a Mortgage usually requires judicial foreclosure through the courts. A Deed of Trust is a security instrument involving three parties, borrower, lender and trustee, that allows the trustee to sell the property without court action if the borrower defaults. Whereas a mortgage is a security instrument involving two parties, borrower and lender, that requires a court process to foreclose if the borrower defaults. The chart below shows which states use deeds of trust, which states use mortgages and which states allow both.

For DSCR Loan borrowers, the type of instrument is determined solely by the property’s location, you cannot choose. However, the day-to-day loan obligations are the same either way; the main practical difference is how quickly and through what process a DSCR Lender could foreclose if you fail to make payments.

The Settlement Statement, or “closing statement” is the master accounting document showing the full breakdown of loan proceeds, closing costs, credits, escrow deposits, and either the exact “cash to close” you must wire in (for purchases/cash-in refis) or “cash to borrower” you’ll receive (for cash-out refis). It is generally considered part of the loan package and must be signed by the borrower or their representatives. It can also serve as a key document confirming the loan has closed and funded.

Another “core document” for DSCR Loans is the personal guaranty if the borrower is an entity (like an LLC). In these cases, DSCR Lenders will require personal guarantees from each principal owner, typically anyone holding 25% or more of the ownership interest of the borrowing entity. A guaranty makes that person or persons personally liable for repayment if the entity defaults and the amount owed is not collected through foreclosure. The guaranty is typically referred to as full recourse and not limited to so-called “bad-boy” carveouts (triggered by fraud, misrepresentation, or other specified violations) common in CRE or business lending. For DSCR Loans where the borrowers are individuals taking title in their own names, separate guaranty documents are generally not needed because the individuals themselves are already directly obligated under the note.

Q: Do all DSCR Loans require signing a personal guaranty?

A: Generally, yes, all DSCR Loans must be “full recourse,” meaning an individual or multiple individuals must sign personal guarantees for the loan. While many DSCR Loans are vested in entities like LLCs, ironically, the only DSCR Loans that do not require individuals to sign personal guarantees are loans made to individuals as borrowers (i.e. not through an entity), because the promissory note itself implies and serves as a personal guaranty, making an extra guaranty document duplicative.

These documents confirm factual statements about the borrower, the property and the nature of the transaction. They are legally binding attestations and become part of the loan record. While some DSCR Lenders will utilize a more comprehensive “loan agreement” that covers many of these items within one document, as is common with larger commercial real estate loans, many DSCR Lenders will not have a standalone “loan agreement.” Instead, these DSCR Lenders will utilize a series of these individual “affidavits,” which are sworn written statements that serve as a formal and legally binding declaration from the borrower as well as riders that are added on to the promissory note, and cover specific loan situations. While having one large “loan agreement” is standard in commercial real estate financing, this sort of loan package with individual declarations and riders is much more common among residential real estate lenders, including those producing consumer owner-occupant and DTI-based loans.

This varying treatment and document set, similar to Deed of Trust vs. Mortgage, doesn’t really matter from the borrower perspective, as the documents essentially do the same thing, regardless of if there is one large “loan agreement” or a big set of individual attestations, affidavits, riders and declarations. This is another illustration of how DSCR Loans uniquely sit between residential real estate and commercial real estate financing, as these differing loan documentation methodologies, one common in residential, one common in commercial, can both show up for DSCR Loans, which mix a lot of the two worlds.

A full loan agreement document is applicable only if a particular DSCR Lender uses one, as many do not. When present, this document consolidates the core terms and covenants of the loan into a single contract, often supplementing the Note and Deed of Trust/Mortgage. If not used by a DSCR Lender, there will likely be a series of affidavits, disclosures and riders related to individual important items, each signed and presented individually.

Q: My DSCR Loan didn’t include a “Loan Agreement,” is that normal?

A: Yes. Not all DSCR Lenders use a standalone Loan Agreement. Some combine all key terms into that single document, while others use separate affidavits, riders, and disclosures to cover the same ground. Both approaches are standard and carry the same legal effect.

A Business Purpose Affidavit is a signed statement confirming the property and, if applicable, any cash-out proceeds are intended strictly for investment/business purposes and not for personal, family, or household use. This protects the DSCR Lender’s status under business-purpose lending rules and limits applicability of certain consumer protection laws.

When it comes to DSCR Loans, the primary focus of this affidavit and the wording of “business purpose” is for occupancy, meaning that the property must not be used for the owners or their family members to live in. Indeed, this provision of DSCR Loans is so important, there may be an additional affidavit document, typically called an “Occupancy Affidavit” or “Non-Owner Occupancy Affidavit" that simply reaffirms this declaration. While it is essentially saying the same thing as the business-purpose affidavit (although not covering the also-important requirement for cash-out proceeds to be utilized for business purposes in loans for that purpose), it further underscores the borrower going on legal record that the property is intended for investment use only.

Note that for both documents, minor exceptions, like staying at a short-term rental for less than two weeks per year are generally okay under these rules, but not likely to be spelled out as such in this document. Also note that in cases where there is a full loan agreement document, the business-purpose and/or occupancy attestation will be included as a section, and a separate affidavit document won’t be needed or present.

Q: What is a Business-Purpose Affidavit in a DSCR Loan?

A: A Business-Purpose Affidavit is a short, signed statement confirming that the property, and any cash-out proceeds, will be used strictly for investment or business purposes, not personal use. It helps the lender classify the loan as business-purpose and avoid consumer mortgage regulations, while still allowing future use changes if circumstances shift.

For entity borrowers (i.e. when title is vested in an entity like an LLC, corporation, partnership or trust), a separate Entity Certificate and Resolution document may be required as part of the loan package. This document certifies that the LLC, corporation, partnership or trust is validly formed, in good standing and authorized to borrow. It will also typically list the members/managers or officers and affirms who has signing authority for the loan.

Many DSCR Loan packages will also have a standalone Name Affidavit document required to be signed in the loan package. This document certifies your legal name and any variations (middle initials, prior names, alternate spellings) that may appear on public records or in the loan documents, ensuring clear identification and title continuity.

Riders are addendums to the core loan documents that modify or add terms specific to the property type, loan structure, or lender requirements. They are only included when applicable and typically if the DSCR Lender doesn’t use a loan agreement document or doesn’t include them directly in the note.

A Prepayment Penalty Rider is applicable only if your loan has a prepayment penalty and the terms are not already stated in the Note or a full loan agreement. This standalone addendum sets out the penalty details, including the percentage, step-down schedule (e.g., 5% in year one, 4% in year two), or flat rate, and clarifies what actions count as a “prepayment” (such as a sale, refinance, or partial payoff).

A Condominium (Condo) Rider is used when the property is a condominium unit. Modifies the mortgage or deed of trust to address condo association rules, assessments, insurance and maintenance responsibilities. It essentially is a legal document requiring that the borrower promises to not only make any and all needed HOA payments, but promises to follow all the rules under the condominium’s HOA.

A Planned Unit Development (PUD) Rider is typically used for properties in a PUD. This rider outlines obligations related to homeowner association dues, common area maintenance and compliance with community rules. It’s essentially the same thing as a condo rider, but for properties that are in an HOA for a planned unit development rather than a condo project.

An Assignment of Rents Rider is a legal document that grants the DSCR Lender the right to collect rental income directly from tenants if you default. Because in many states the foreclosure process can sometimes be long and arduous, this provides additional protection to the lender to collect some of what is owed if the property is still occupied and leased to rent-paying tenants during a default.

Q: What is a DSCR Loan Condominium Rider?

A: A DSCR loan Condominium Rider is added when the property is a condo unit. By signing it, you agree to follow all the condo association’s rules, pay any required fees or assessments, and keep the right insurance in place. It basically gives comfort to the lender that you are agreeing to meet all the obligations of the HOA and not jeopardize their collateral.

These are DSCR Loan documents that ensure the loan complies with state laws and provide the lender with authority to make administrative corrections if needed. State-Specific Notices and Disclosures are required forms depending on the property’s location. These can include attorney closing acknowledgments (GA, SC, NC), Texas “No Oral Agreements” notices, property condition affidavits, or local tax and settlement certifications. There will also be what’s typically called an “Error & Omissions Agreement” in a DSCR Loan package. This document authorizes the lender or closing agent to correct clerical or administrative errors in your signed documents after closing, without requiring a full re-signing, as long as no material terms are changed.

Q: What’s an Error & Omissions Agreement for a mortgage loan?

A: An Error & Omissions Agreement (also called a Compliance Agreement) is a document you sign at closing that lets the lender or title company correct minor clerical mistakes in your mortgage paperwork after closing. It can’t change the loan’s core terms; it can only fix small issues like typos, missing dates, or incomplete signatures.

These are DSCR Loan documents that relate to protecting the property securing the loan and ensuring that taxes, insurance and other obligations are paid on time.

The Initial Escrow Account Disclosure appears only if the DSCR Lender is requiring an escrow account for taxes and/or insurance and chooses to utilize it, as it is a TRID requirement for consumer mortgage loans, but not legally required to be used by DSCR Lenders. This disclosure shows the starting balance collected at closing, the monthly escrow portion included in the PITIA Payment and the anticipated disbursement dates. Note that this disclosure should make clear that the initial monthly escrow amounts are based on an estimate of what will need to be paid and are subject to change over the life of the loan term. Since property tax costs and property tax rates typically move up over time, but not at a standardized 100% predictable rate, the monthly escrows are not specified in any loan documents as an exact number for the life of the loan (like monthly debt service typically is on fully amortizing loans), and this disclosure importantly spells out the variability and likely increased change in these amounts that borrowers should expect.

An Insurance Authorization & Requirements Form confirms hazard insurance coverage is in place, identifies your carrier and policy limits and authorizes the DSCR Lender (eventual servicer via eventual note holder) to verify coverage or obtain updates as needed. This essentially means that the servicer will and is authorized to handle needed renewals and updates in property insurance over the life of the loan. If the DSCR Lender is utilizing a loan agreement document, this information might be in that document, and not exist as a standalone. There may also be a Replacement Cost Endorsement or Waiver required by some DSCR Lenders to ensure your hazard policy includes replacement cost coverage. If waived, the waiver form confirms the DSCR Lender’s acceptance of the coverage exception.

For DSCR Loans, there will also typically be Flood Certification & Flood Insurance documentation provided if the property is located in a FEMA-designated flood zone (and not included in an overall loan agreement document). For properties in these zones and requiring flood insurance, this document verifies compliance with flood insurance requirements and identifies the policy in force.

These are DSCR Loan documents that finalize the payoff of any existing obligations, set up your payment method and ensure the DSCR Loan can be properly serviced after closing.

A DSCR Loan First Payment Letter states the date and amount of your first payment, along with a breakdown of principal (if applicable), interest and escrows (if applicable). It should also note the payment address or online payment portal instructions. There will also usually be a Servicing Disclosure or Notice of Transfer which informs you whether the originating DSCR Lender will retain servicing of your loan or transfer it to another servicer after closing. An IRS Form W-9 may also be included among these documents. The W-9 form provides your taxpayer identification number (SSN or EIN) to the lender and servicer for reporting purposes, such as issuing IRS Form 1098 for interest paid. Note that all three of these documents are optional for DSCR Lenders and may or may not be included.

While this document and provision is commonly optional for many DSCR Lenders, many DSCR Loan document packages will include an ACH / Automatic Payment Authorization form. This document allows the DSCR Lender or servicer to draw your monthly payment automatically from a designated bank account. This includes both authorization and includes the exact bank account information for the lender and servicer to pull the monthly payments.

For refinance transactions, a Payoff Authorization document may be in the loan package which authorizes the title company to pay off your existing mortgage(s) and any other debts that appear in the payoff section of your settlement statement.

Q: What’s an ACH form for a DSCR Loan?

A: An ACH (Automated Clearing House) or Automatic Payment Authorization form allows your lender or loan servicer to automatically pull your DSCR loan payments each month from a specific bank account you designate and is a document signed at closing as part of the closing package. The form includes both your authorization and your exact account details, which means accuracy is critical, even a small typo or unclear handwriting can cause failed payment attempts, creating headaches, potential late fees, and in extreme cases, a default if the first payment isn’t processed correctly.

RELATED: Community Property State Signature & Consent Requirements in DSCR Lending

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.