.png)

.png)

When a DSCR Loan is made to an entity rather than an individual, the lender must verify the entity’s existence, legal standing, and authority to borrow. This applies whether the entity is simple, such as a single-member LLC where one person owns 100%, or more complex with multiple owners, each with varying levels of involvement in the loan.

Even in the simplest scenario, all verification checks are still necessary to ensure the entity is properly formed, in good standing, and able to encumber the property. The importance of these checks increases significantly when multiple owners are involved. For example, in cases when not all owners may be guarantors, the lender needs to clearly identify which members are personally guaranteeing the loan. Additionally, signing authority must be documented, i.e. the lender must know exactly who is legally authorized to sign on behalf of the entity. Finally, decision-making rules in governing documents must be verified, for example, some operating agreements require unanimous consent for major transactions like borrowing, while others allow a single manager to make those decisions.

If the DSCR Lender misses something here, the consequences can be serious, such as the mortgage or deed of trust could be deemed invalid, the DSCR Loan could become non-enforceable against the property and in case of foreclosure, the lender could lose priority or fail to collect entirely. Because of these risks, DSCR Lenders require precise, verifiable entity documentation before closing. The requirements vary by entity type, and each key document serves a specific purpose.

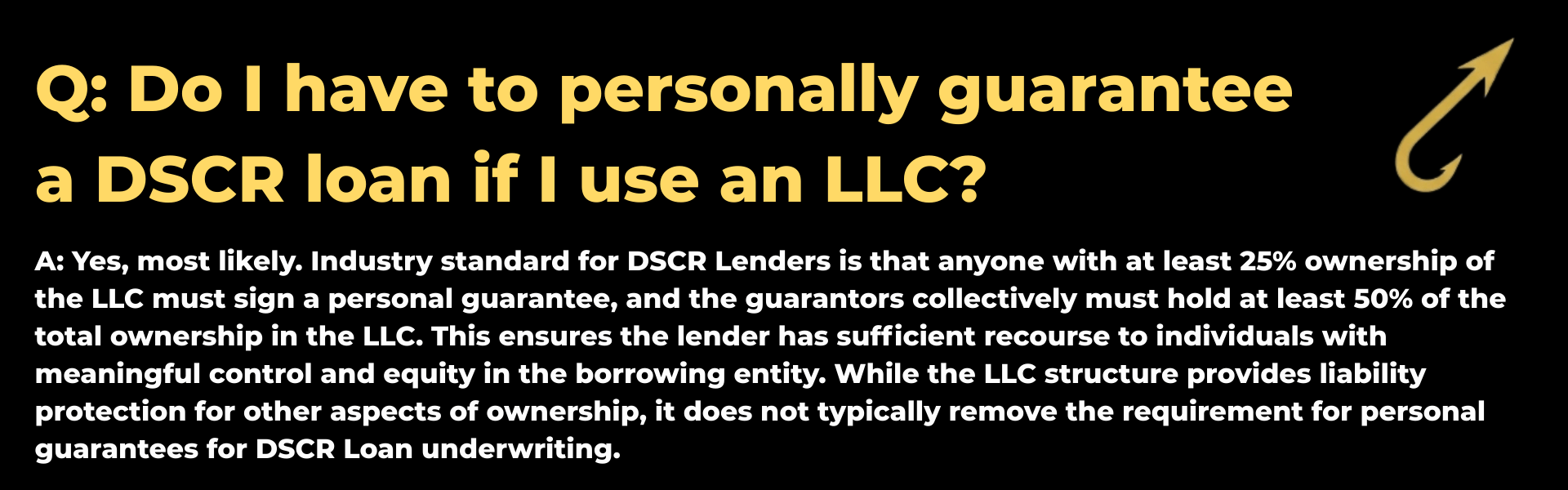

Q: Do I have to personally guarantee a DSCR loan if I use an LLC?

A: Yes, most likely. Industry standard for DSCR Lenders is that anyone with at least 25% ownership of the LLC must sign a personal guarantee, and the guarantors collectively must hold at least 50% of the total ownership in the LLC. This ensures the lender has sufficient recourse to individuals with meaningful control and equity in the borrowing entity. While the LLC structure provides liability protection for other aspects of ownership, it does not typically remove the requirement for personal guarantees for DSCR Loan underwriting.

DSCR Loans can be made to a variety of business entities which generally are reviewed and documented similarly. Limited Liability Companies (or “LLCs”) are the most common business structure, but some investors prefer corporate or partnership structures for the borrowing entities for their properties. While the exact governance structure differs between LLCs, corporations, and partnerships, lenders approach them with the same core goals.

When a DSCR Loan is made to an entity instead of an individual, the lender must confirm two critical things, 1) that the entity exists, is active, and is in good standing in the relevant state(s) and 2) the person(s) signing the loan documents has the legal authority to bind the entity to the loan, as in multi-owner entities, not all owners may be guarantors, and most importantly, signing authority might be limited to certain members or require unanimous consent.

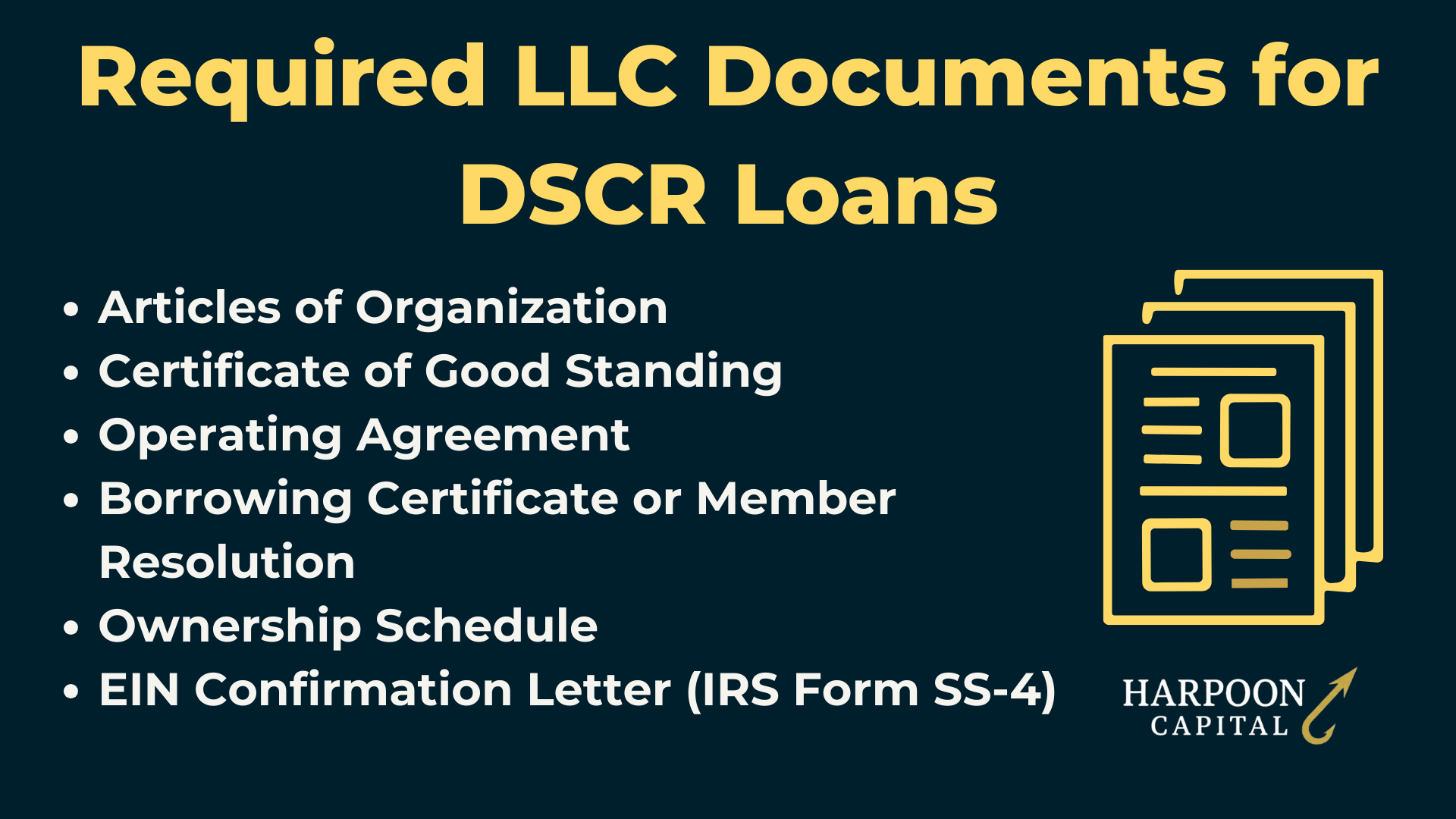

An LLC is a flexible business structure that is favored by many real estate investors because it provides its owners with liability protection and flexible features of management and taxation. Generally, it can be thought of as combining the best aspects of a corporation structure (liability and downside protection) and a partnership (no “double taxation” and less burdensome regulatory and filing requirements). The documentation burden is also relatively light, but similar to DSCR Loans themselves, is not “no doc,” but instead a meaningful and common-sense paperwork bundle of what is needed.

For borrowers on DSCR Loans utilizing an LLC, there is a typical set of “entity documents” required to provide. Typical required documents of LLCs include:

Q: How long is a Certificate of Good Standing valid for a DSCR Loan?

A: Most DSCR Lenders require a Certificate of Good Standing dated within the last 60 to 90 days at the time of closing. While the certificate can be requested at any time, it reflects only the entity’s status on the date it was issued, so a new one may be needed if the closing is delayed.

For investors utilizing an LLC as the borrower for a DSCR Loan, there are some key considerations to keep in mind to make sure the entity documentation requirements don’t cause delays or issues. First is to make sure that all documents clearly show state stamps or filing confirmations as unsigned drafts are not acceptable for DSCR Lender loan files. Additionally, most DSCR Lenders will require a Certificate of Good Standing if the entity is in existence more than 90 days prior to the expected closing date, even if no taxes have been filed yet. If the entity has been formed less than 90 days before closing, most DSCR Lenders won’t require a Certificate of Good Standing, but it makes sense to double check this since lender policies can vary. And finally, if the LLC is foreign-registered in the property’s state, the DSCR Lender will likely require a valid foreign registration certificate, which could take a couple weeks to receive after request.

When an LLC, corporation, or partnership is formed in one state but owns property or conducts business in another, that “other” state considers the entity a foreign entity. To legally operate there, including holding title to real estate, the entity must apply for and obtain foreign qualification from that state’s Secretary of State.

The resulting Foreign Registration Certificate (sometimes called a “Certificate of Authority”) is proof that the entity is authorized to do business in that state. DSCR Lenders will often require this because if the property’s state requires foreign registration and the borrower entity doesn’t have it, the DSCR Lender’s mortgage could be challenged (i.e. foreclosure rights) or even invalidated in that state. Some states have carve-outs for this (e.g., passive ownership exceptions), but many DSCR Lenders require foreign registration anyway to avoid legal ambiguity.

While getting a foreign registration certificate is a fairly easy and straightforward process, the processing time for a foreign registration certificate can be a significant deal hurdle for borrowers unaware it is needed. Processing time can vary by state; it can range from same-day online approval to 2–3 weeks if mailed or if the state has backlog. Rush service may be available for a fee in some states but it’s best practice for borrowers utilizing LLCs and investing nationally to confirm these requirements and order early in the process if it’s necessary, to avoid costly delays or headaches.

Q: What is a foreign registration certificate for an LLC in a DSCR Loan?

A: It’s proof that an LLC formed in one state is legally authorized to own property and conduct business in another state. If your DSCR loan is for a property in a state different from where your LLC was formed, many DSCR Lenders will require this certificate from the property’s state before closing.

Q: Do I need a Certificate of Good Standing from more than one state for a DSCR Loan?

A: Yes, if your entity was formed in a different state than where the property is located, most DSCR Lenders require a Certificate of Good Standing from both the formation state and the property’s state (via foreign registration) to confirm the entity is active and authorized in each jurisdiction.

Q: How long does it take to get a foreign registration certificate?

A: In some states it’s available the same day through an online application, while others can take 2–3 weeks. Because DSCR Lenders won’t close without it, borrowers should start the application as soon as they go under contract or begin the refinance process if using an LLC in a different state from the property.

A Series LLC is a specialized form of limited liability company that allows for the creation of multiple, separate “series” or “cells” under one master LLC. Each series can hold its own assets, incur its own liabilities, and have its own members and managers, essentially functioning like an independent LLC, while remaining under the umbrella of the master LLC. Investors will typically use Series LLCs for liability segregation as the debts and liabilities of one series are intended not to affect the assets of another series, administrative efficiency, since one master LLC filing (and often one annual report) covers all series, ongoing costs and paperwork can be significantly reduced.

Series LLCs are also often used by investors planning to invest heavily in a singular state, as only a limited number of states allow the structure and typically properties with their own series cell must all be in the same state as the master LLC. Series LLCs originated in Delaware but are now recognized in multiple states, including Texas, Tennessee, Illinois, Nevada, Oklahoma, Utah, Iowa, Arkansas and Montana.

Many DSCR Lenders can be wary of Series LLCs because the structure is still relatively new and there is limited case law on how courts will treat them in creditor disputes. While some DSCR Lenders will only lend to the master LLC and require the property title to be held directly in the master LLC, others will lend to the series holding the property, but will require full master LLC documentation plus the series’ formation and governance documents. In addition, when DSCR Lenders accept Series LLC borrowers, it could require a formal “exception,” adding to the deal uncertainty and timeline and may come with additional costs as many lenders utilize third-party legal firms (outside attorneys) to review entity documents, and the review of these extra documentation needs will typically be passed on to the borrower.

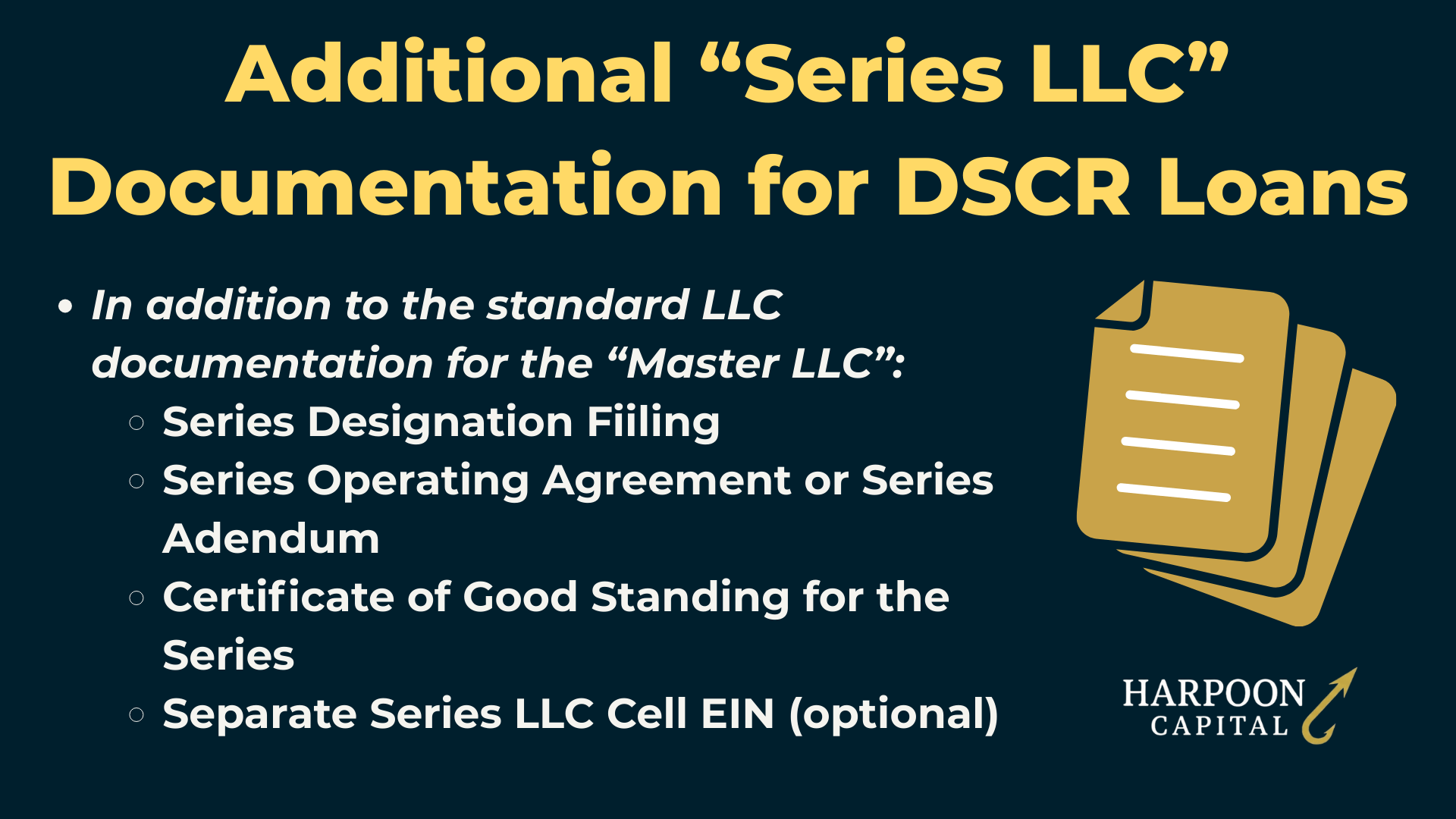

There will also typically be some additional documentation required for a DSCR Loan to a Series LLC. This will typically involve providing the normal LLC documentation package for the “master LLC,” which will include the master LLC articles of organization, operating agreement and certificate of good standing. In addition to the “master LLC” documents, “series-level” documents will be typically required, including the “Series Designation Filing” a document filed with the Secretary of State (note however that not all states require public filing of series), a Series Operating Agreement or Series Addendum, showing the members, managers, and borrowing authority specific to the series and a Certificate of Good Standing for the Series, required in states where each series is separately registered and must maintain its own standing. In addition, some DSCR Lenders will be okay with just an EIN confirmation letter and Tax ID number for the master LLC only, however some will require a separate Series LLC Cell EIN confirmation letter as well.

If using a Series LLC for a DSCR Loan, it’s a borrower best practice to check early whether the specific DSCR Lender accepts Series LLCs or if this structure requires an exception. Additionally, the specific series-level LLC entity documents may differ from lender to lender so it’s crucial to get a specific checklist of required documents in that area as well.

A corporation is a separate legal entity owned by shareholders and governed by a board of directors. Day-to-day operations are handled by officers (e.g., CEO, CFO), and corporate governance is dictated by bylaws. While most real estate investors who utilize DSCR Loans will typically use an LLC as the entity type for the borrower, using a corporation as the borrowing entity on a DSCR Loan does occur sometimes and is generally always allowed by DSCR Lenders.

The entity documentation package for corporation borrowers on DSCR Loans will look similar to LLCs and typically require Articles of Incorporation, filed with the state to legally create the corporation and that lists the corporate name, incorporation date, and state. Instead of an Operating Agreement typically found in LLC or partnership document sets, corporations will typically have “Bylaws” which serve as the internal rules governing corporate operations, including officer roles and borrowing authority and require a specific “Corporate Resolution,” which is a board-approved resolution authorizing the loan and identifying the authorized signer(s). Like LLCs, corporations will typically need a “Certificate of Good Standing,” a state-issued confirmation that the corporation is active and compliant which, similar to the “foreign entity registration certificate” for LLCs, may be required from multiple states if incorporated in one and owning property in another. Corporation borrowers will also generally need an EIN Confirmation Letter including an IRS-issued letter verifying the corporation’s Employer Identification Number. And finally, some DSCR Lenders’ entity document checklists for corporations will include Franchise Tax Status / Payment Evidence, which is proof that state franchise taxes are paid and current, required in some jurisdictions to maintain good standing. Most DSCR Lenders will require a list of current shareholders in order to determine guarantor status for the loan if not included in the bylaws.

%20for%20DSCR%20Loans.png)

A partnership is a business structure in which two or more people share ownership and management responsibilities. In a general partnership, all partners typically have equal authority and liability; in a limited partnership, there are general partners (managers) and limited partners (investors without management control).

For borrowers on DSCR Loans utilizing a partnership structure for vested ownership (i.e. the “borrower” on the loan), the typical entity documents required include:

A trust is a legal arrangement in which one party (the trustee) holds and manages property for the benefit of another (the beneficiary), as set out by the person who created the trust (the settlor, also called the grantor or trustor). The terms of the trust are established in a written trust agreement, which determines how the property is managed, who benefits from it and what powers the trustee has.

Trusts are commonly used for estate planning, asset protection, privacy, and in some cases tax efficiency. By holding property in a trust, an owner can simplify the transfer of assets to heirs, avoid probate, keep ownership details off public records, or protect assets from certain liabilities. For real estate investors, placing property in a trust can also help maintain continuity of ownership and management if the owner becomes incapacitated or passes away.

In general, most DSCR Lenders allow investors to utilize certain types of Trusts for vesting (i.e. act as borrower on the DSCR Loan) as long as a specific set of conditions exist for the trust structure. Typically, lenders need to verify that the trust is valid and enforceable under applicable state law and that the trust type is eligible (there are many types of trust structures, and generally only some can be borrowing entities on DSCR Loans). Additionally, DSCR Lenders confirm that the trustee(s) have clear, explicit legal authority to borrow money and encumber the property.

Q: Can you get a DSCR Loan if your property is in a trust?

A: Yes, depending on the specific type or structure of the trust. Many DSCR Lenders will allow loans to properties held in a trust if the trust is revocable, the settlor is also a primary beneficiary and trustee, and the trust agreement grants clear authority to borrow and encumber the property.

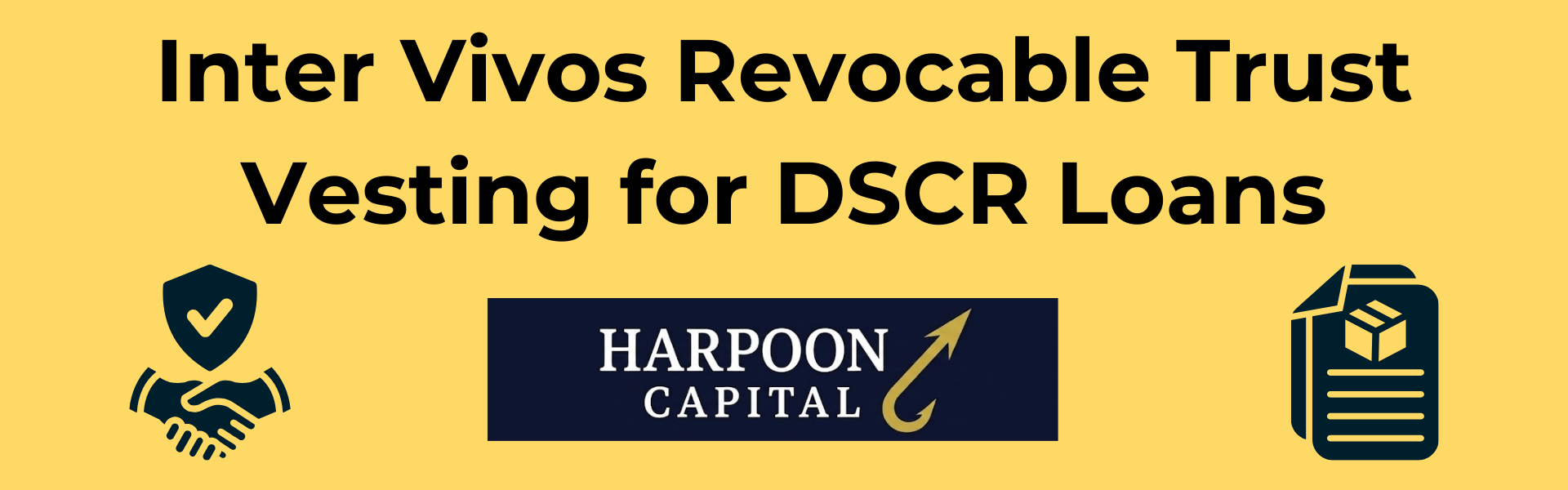

An “Inter Vivos Revocable Trust” is a trust created by the settlor during their lifetime (inter vivos means “between the living”) that can be altered, amended, or revoked at any time. The settlor retains full control of the trust assets and can make changes as needed. Investors generally create these types of trusts as an estate-planning tool, with several benefits related to transferring assets at death. This type of trust structure allows the assets, in this case real estate rental properties, to be handed down to heirs without involving courts, i.e. the “probate” process, which minimizes time and costs and maximizes privacy. The Inter Vivos Revocable Trust structure also has benefits in the case of continuity of asset management in case the settlor becomes incapacitated, as the trust documents can determine the process here without needing a court-appointed conservator or guardian.

Inter Vivos Revocable Trusts are generally acceptable to be used as a borrowing entity for DSCR Loans if the settlor is also the primary beneficiary and serves as a trustee and if the trust agreement explicitly grants the trustee the authority to borrow money, encumber the property and sign loan documents. If there are multiple trustees, then generally all trustees must sign at closing and title insurance must insure the trust without unacceptable exceptions.

Note that the Latin-flavored name is long and a mouthful and Inter Vivos Revocable Trusts can often be referred to with different labels, but they are functionally the same structure, and also generally eligible for DSCR Loans. These types of trusts can also be referred to as “Living Trusts,” “Family Trusts” or “Revocable Living Trusts” but are generally all just different monikers for Inter Vivos Revocable Trusts and have the same uses, documentation requirements and eligibility standards for DSCR Loans.

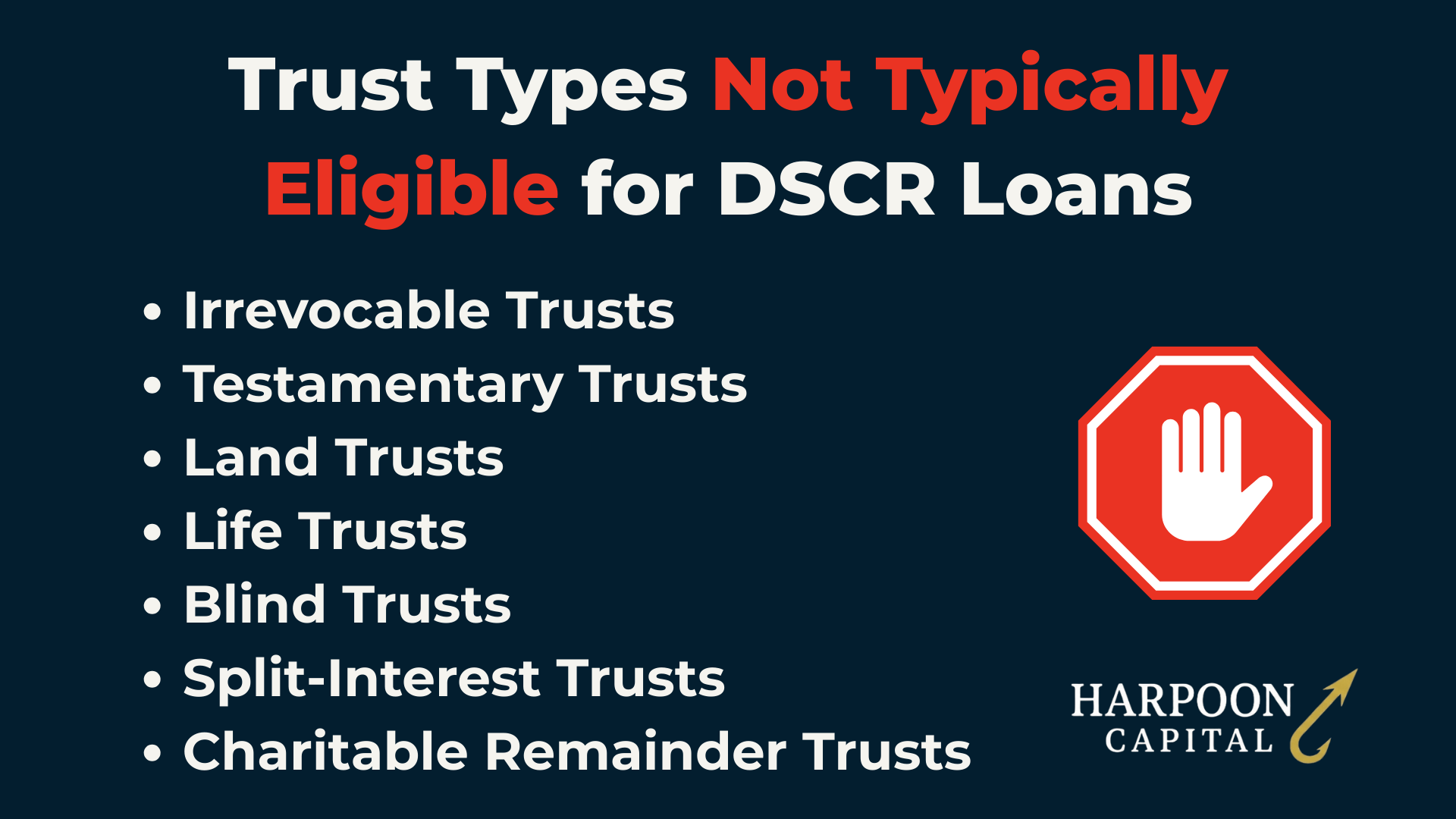

While the Inter Vivos Revocable Trust (regardless of the naming convention type) types listed earlier are typically eligible as DSCR Loan borrowing entities, many other trust structures are generally ineligible because they present enforcement, control or title issues for the DSCR Lender. These trust types, that are typically not allowed as borrowing entities (i.e. vesting) for DSCR Loans, include Irrevocable Trusts, Testamentary Trusts, Land Trusts, Life Estate Trusts or Blind Trusts. In addition, trusts that have “split interest” or “charitable-remainder” structures or situations where multiple trusts have split ownership of the subject property are ineligible to be used as borrowing entities for DSCR Loans as well.

Irrevocable Trusts are trusts that, once signed and funded, cannot be altered, amended, or revoked by the settlor without the unanimous written consent of all beneficiaries (and sometimes court approval). The settlor effectively surrenders ownership and control of the property. Because the settlor no longer controls the asset (real estate), the DSCR Lender cannot be certain the property can be sold or refinanced to repay the debt if needed. Any changes, such as granting a mortgage, could require consent from all beneficiaries, which may be impractical or impossible. While some lenders may consider on a case-by-case basis if all beneficiaries provide written consent and the trustee has explicit, unrestricted borrowing and encumbrance powers in the trust document, it is extremely rare for a DSCR Lender to allow any trust with an irrevocable trust as the borrowing entity.

A “Testamentary Trust” is a trust created through a will that does not come into existence until the settlor’s death. The terms are established in the will, and the trust is funded only after the estate’s probate process is complete. The trust technically doesn’t exist until probate is concluded, which can take months or years. Until then, ownership and control of the property are uncertain, making it impossible for a DSCR Lender to underwrite or secure the loan.

Land Trusts are trust arrangements, common in some states like Illinois, where the trustee holds legal title to the property, while the beneficiaries retain control over management, sale and rental decisions. These types of trusts are often used to keep ownership anonymous in public records. While land trusts can provide privacy, they often limit lender transparency. Beneficial owners may change without notice and the structure can make understanding who needs to (and can validly provide) recourse guarantees infeasible for the DSCR Lender (as well as complicate fraud avoidance and anti-money laundering efforts). For these reasons, Land Trusts are generally ineligible as vesting structures for DSCR Loans.

Life Estate Trusts are trust arrangements where one or more individuals (life tenants) have the right to use and occupy the property during their lifetime, after which ownership automatically transfers to a “remainderman” beneficiary. Similar to the same issues with Land Trusts, in which this structure and ownership transfer complicates the generally mandatory personal recourse guaranty requirements for DSCR Loans, these sorts of trusts are also typically ineligible to be borrowing entities on DSCR Loans.

A “Blind Trust” is a trust in which beneficiaries have no knowledge of the trust’s assets, and the trustee has full discretion over management and investment decisions without beneficiary input. These are often used for conflict-of-interest avoidance in political or corporate settings. While these sorts of trusts can be structured to invest in rental real estate as part of an investment strategy, the lack of beneficiary knowledge and transparency makes it difficult for the DSCR Lender to verify who controls the property and whether the trustee can borrow or encumber it in compliance with the trust’s terms and as such, Blind Trusts typically can’t be borrowing entities for DSCR Loans either.

A Split-Interest or Charitable Remainder Trust is a trust where the benefits of ownership are split between two or more parties, such as providing income to a non-charitable beneficiary for a set term, with the remainder going to a charity. These conflicting beneficiary rights create legal complexity and a DSCR Lender (or eventual note holder) may be unable to enforce a foreclosure or collect proceeds without impacting a charitable beneficiary’s rights, which can create reputational and compliance risks, generally not “worth it” to allow this type of trust. Additionally, cases of “multiple trust ownership,” or situations where title to the property is held jointly by two or more separate trusts, are not workable for DSCR Loan vesting. Each trust has its own settlor, beneficiaries, and trustee(s), and each must agree to any action affecting the property and this also adds multiple layers of authority, consent and title insurance complexity. Most DSCR Lenders would have to require every trust involved would have to satisfy the same eligibility and documentation requirements, creating too much legal risk and potential for delay, so most will not allow multiple trust vesting, although this type of situation may be allowed on a case-by-case basis.

Q: What type of trust is eligible for a DSCR Loan?

A: To be eligible for a DSCR Loan in which the borrowing entity and owner of the property is a Trust, generally the trust must have what is called a revocable structure, meaning the settlor (creator of the trust) retains full control of the property during their lifetime. These are typically called “Inter Vivos Revocable Trusts,” “Living (Family) Trusts” or Revocable Living Trusts. To qualify, the settlor is typically required to also be a primary beneficiary and a trustee, and the trust agreement must clearly grant the trustee authority to borrow money, sign loan documents, and encumber the property as security for the loan. Irrevocable Trusts, and most other types, are generally not eligible for DSCR Loans.

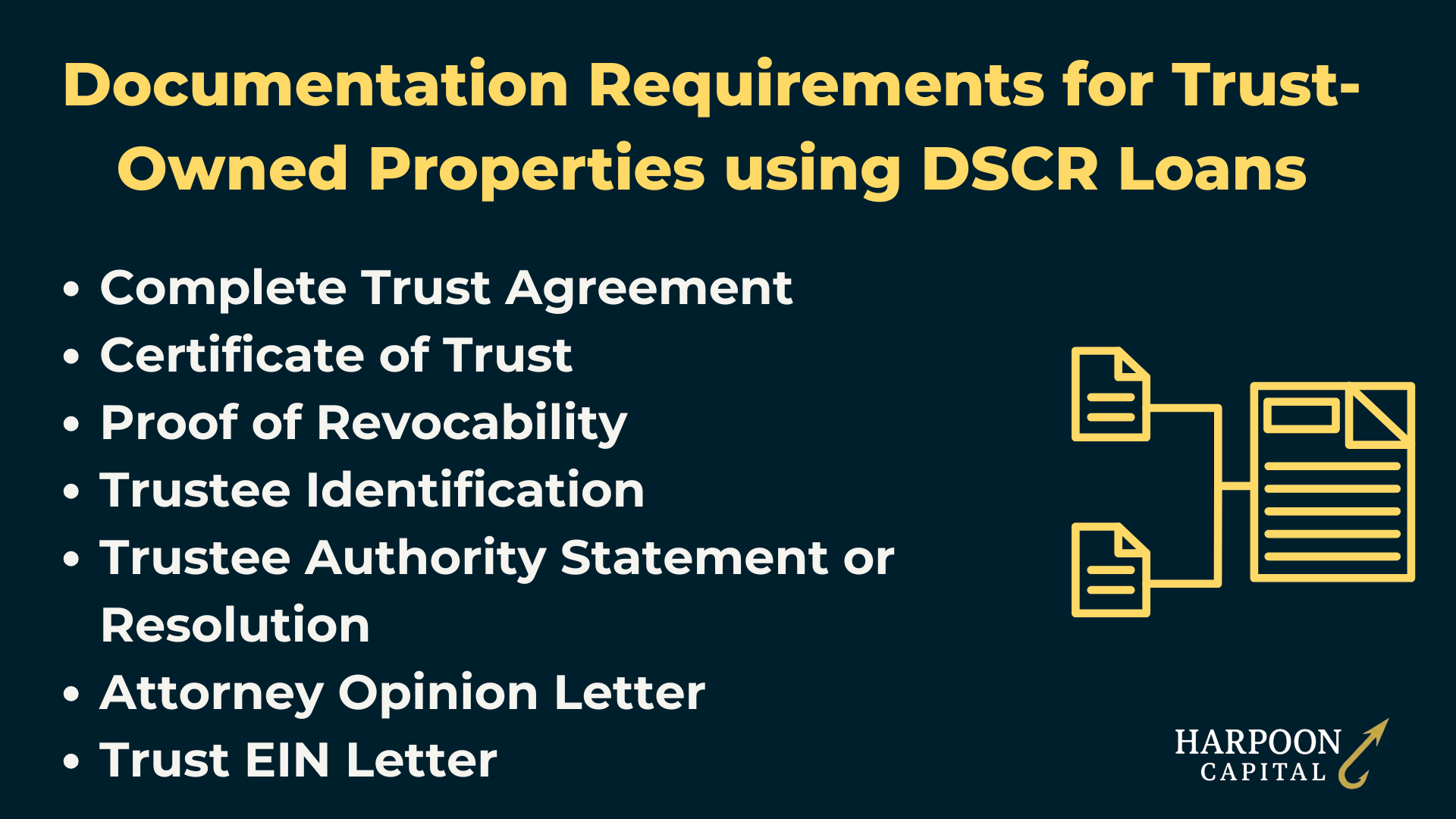

For eligible trusts serving as the borrowing entity, DSCR Lenders typically require these documents:

Q: Does the trustee have to sign the DSCR Loan documents if the borrower is a Trust?

A: Yes. All trustees listed in the trust agreement must sign the loan documents, both in their capacity as trustee and, if applicable, as an individual borrower or guarantor.

A syndication is a structure in which multiple unrelated investors pool funds to jointly purchase and own real estate, typically through an LLC, limited partnership, or similar entity. In a syndication, investors often contribute small ownership percentages and may have little to no direct role in the property’s day-to-day management.

While syndications are common in commercial real estate investing, DSCR Lenders vary in their approach and eligibility. Some will not finance properties held in a syndicated ownership structure at all, while others will allow it under strict conditions, typically requiring full joint and several personal guarantees from owners representing at least 50% or more of total ownership, complete documentation of ownership percentages, roles, and signatures for all guarantors (which can be very challenging with some syndications numbering near or above 100 investors) and clear borrowing authority in governing documents to ensure the entity can legally encumber the property.

These requirements can make many syndications ineligible, especially those with numerous passive investors who each hold small ownership stakes and are unwilling to personally guarantee the loan (potentially required in situations with significantly granular ownership that can’t hit the 50% aggregation mark without including small-portion investors). However, certain syndications with a smaller group of owners holding significant equity, and willing to provide full guarantees, may still qualify with some DSCR Lenders, especially in situations where the central owner-operators of the property own significant equity stakes (i.e. >25%).

Q: Do DSCR Lenders allow syndications?

A: Some do, but only under strict conditions, most commonly requiring full joint and several guarantees from owners holding at least 50% of the entity’s equity. This eliminates many passive-investor syndications but can work for smaller groups where major owners are willing to guarantee the loan.

Up Next: Check out this special section on Community Property State Signature & Consent Requirements in DSCR Lending, a tricky issue that can send deals sideways if not fully understood!

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.