.png)

The market side of the DSCR Loan rate equation (as opposed to the loan-specific adjustments discussed in Section 22: LLPAs & Overlays) is hard to predict and generally outside the control of real estate investors, but making financial moves at the right times and right market conditions is a huge key to success in long-term real estate investing. The biggest driver by far of rates is what’s based on the greater market as even the best qualified DSCR Loans, with low LTVs, sparkling credit scores and unblemished history, robust DSCR ratios, are going to have an interest rate somewhere above the market Treasury yields and fed funds rate. But every percentage point – even basis point! – can matter, and understanding when to put on the brakes and when to put pedal to the metal in real estate investing can make or break a portfolio.

Historically, when DSCR Loans really entered the scene in 2018 and 2019 – interest rates were generally in the 5-6% range, and real estate values, while rising throughout the 2010s, hadn’t begun to really skyrocket like in the 2020-2021 period. Cash flow on traditional long-term leases on single family rentals was still solidly available at these rate levels. 2020 was a rollercoaster year for many, many reasons, DSCR Loans included; with the market for DSCR Loans completely freezing (meaning DSCR Loans weren’t available at any rate) for a few months at the beginning of the COVID panic in the spring, however, soon after the Federal Reserve cut rates to zero and launched massive quantitative easing program in March 2020, not only did the market re-open for DSCR Loans, but towards the latter half of 2020, the real estate market took off.

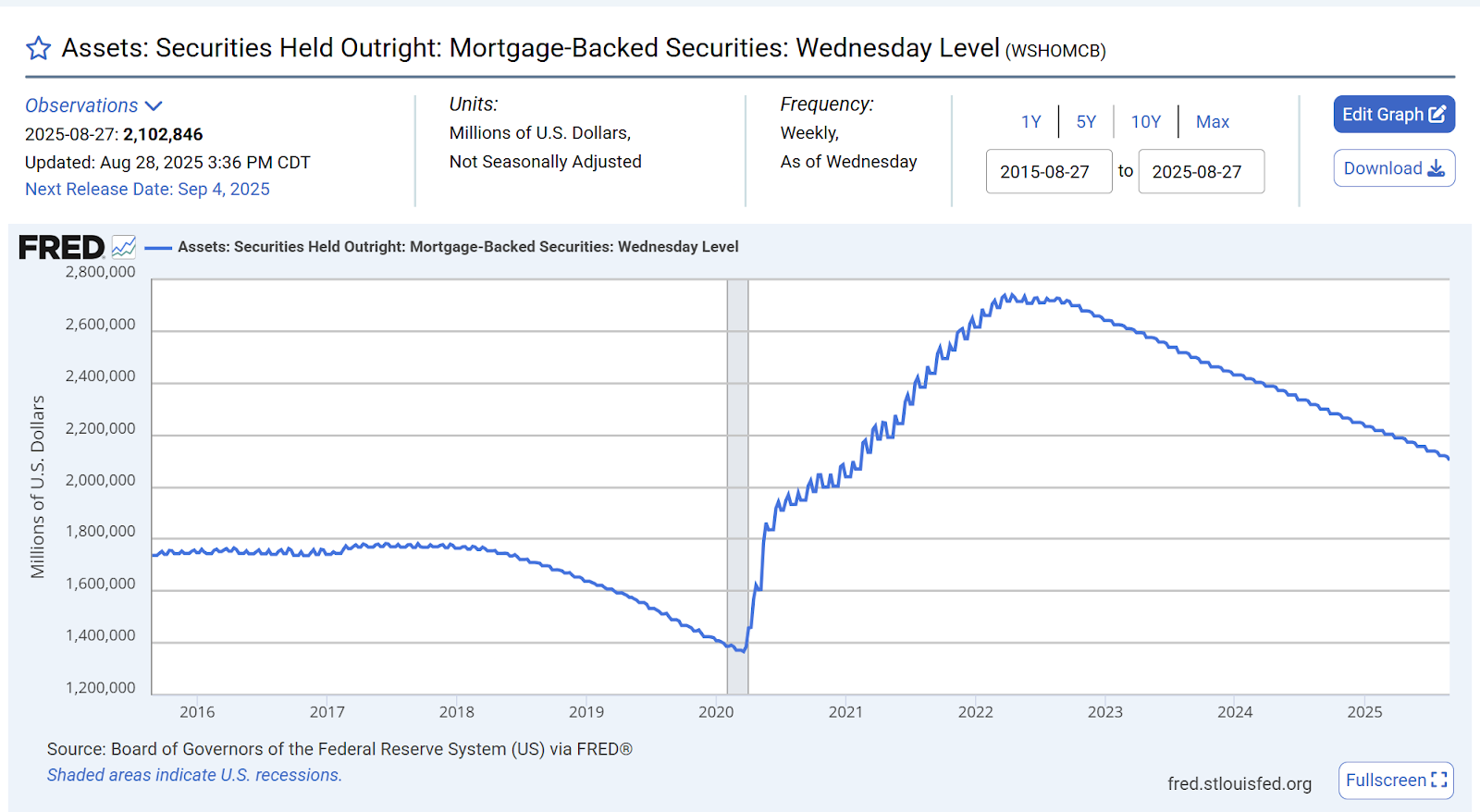

With the low rates and rocket fueled real estate values creating a frothy market into 2021, DSCR Loan rates dropped into the 4-6% range and even touched “three handles” – or rates under 4%. DSCR Loan rates were also so low at this time because the Federal Reserve had not only cut rates to zero in 2020 and bought US Treasury Bonds through quantitative easing throughout the first year of COVID, they continued to keep rates at the zero bound, continued to purchase Treasuries and bought significant amounts of MBS (conventional), which further pressured yields down to zero and mortgage rates at historic lows. Even when the market surged in 2021, creating a frenzied real estate market with surging prices and activity, the Federal Reserve dismissed inflation concerns as “transitory” and continued supporting the Treasury and MBS market through open market operations through the year.

This ill-fated decision to artificially suppress mortgage rates and turbo-charge the real estate market in 2021 was great for investors that locked in rock-bottom rates for their portfolios in 2021 and for professionals in the mortgage and real estate industry, but reality would snap back hard in 2022.

As inflation started to rage in late 2021 and into 2022 – showing it wasn’t just “transitory” as Federal Reserve and Biden Administration officials had wishfully claimed during the prolonged government spending frenzy and loose monetary conditions (zero fed funds rate and quantitative easing), the Federal Reserve started raising rates three years after the fateful March of 2020 – raising rates in March 2022 for the first increase since 2018. While DSCR Loan rates had started to rise in anticipation, as inflation continued to rise and the Fed began to slowly unwind QE by running off their MBS holdings, 2022 saw a relentless rise in rates with DSCR Loan rates rising rapidly and violently, spiking to an average of less than 5% in the spring to above 6% in summer, then above 7% or even 8% by the fall of 2023.

Many DSCR Lenders that were not prepared for the rate rise reality lost millions and dramatically cut their workforces or even went out of business. While there wasn’t a huge rise in delinquencies (as the vast majority of the DSCR Loans originated in 2020 and 2021 were low-rate and fixed for 30 years, so people’s monthly payments didn’t move), there was a severe pullback in volume with refinancings falling off a cliff (outside the occasional BRRRR) and many investors holding off on expanding portfolios when faced with elevated rates crimping cash flow.

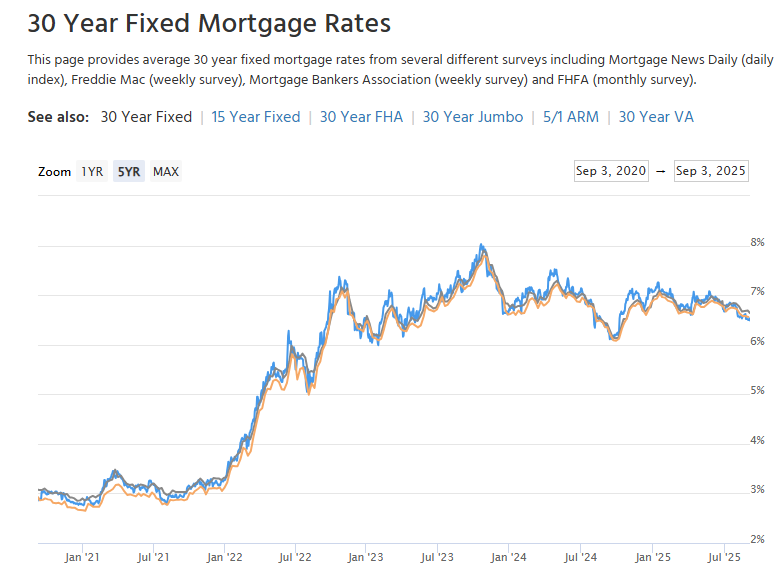

October 2023 saw the likely top of mortgage rates for a while (see below for the tracking from MortgageNewsDaily.com – which is for general conventional loan rates, but these move in similar manner to DSCR Loan Rates). Rates started to drift down through 2024 and 2025, but continued to chop up and down and stay in a fairly consistent range, generally in the 6-8% range for DSCR Loans in these years. While real estate values generally stayed stable or slowly increased on average, DSCR Loans continued to pick up volume and exceed the frozen landscape of 2022 and 2023, however getting deals to cash flow remained challenging, which helps explain the rise of strategies such as BRRRR, Short Term Rentals and multifamily investing as many long-term rental SFRs still struggle to cash flow at these rate levels.

What comes next for the end of 2025 and 2026 and beyond? It’s anyone’s guess but it certainly appears that rates are destined to continue to go down, and spark another surge in real estate investing activity and portfolio building. The math varies and the market is dependent on many factors however, once average DSCR Loan rates sink below 6% it’s likely a huge surge in activity will be unlocked, as deals begin to “pencil” again with traditional single family rentals, unlocking a market that’s been pretty unfeasible for years.

Additionally, there are more basic math and “charts” that make it very hard to believe that realistically, further rate cuts and money printing quantitative easing won’t resume as US Federal Government interest payments skyrocket with higher debt costs:

This chart shows that the US debt is rapidly becoming unsustainable, the interest payments are a function of debt and interest rate (the yields demanded at new Treasury auctions), and the easiest way to flatten the above curve is to lower borrowing costs through rate cuts. As we have illustrated, mortgage rates and DSCR Loan rates are sure to follow this inevitable rate cut band aid solution.

In addition, 2025 has seen a public feud between President Trump and the chair of the Federal Reserve, Jerome Powell, with the President understandably pushing for rate cuts and relief for the markets, particularly the real estate market and mortgage rates. While Powell has mostly resisted, his term is due to end in May 2026 and it is extremely likely that the replacement appointment (made by President Trump and confirmed through a GOP-controlled Senate) will be completely in line with rate cuts and lower mortgage rates.

All that being said, it’s tough to make predictions, especially about the future, as aptly explained by the great Yogi Berra. Anyone who can perfectly predict the path of bonds and interest rates would certainly not need to worry about DSCR Loans or real estate investing as they would be busy bathing in billions. But the case is clear: it is very likely that DSCR Loan rates are likely to fall in the near future, and when they do, opportunities for real estate investors will re-emerge after a long wait. The smart and savvy investor will be watching – and after reading this chapter – will be equipped to watch closely and strike when the iron is hot before the rest of the market wakes up.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.