.png)

.png)

In addition to experience, citizenship/immigration status and background checks, financial factors principally around net worth and liquidity also play a role in qualifying for a DSCR Loan.

DSCR Lenders require borrowers (guarantors) to demonstrate a cushion of liquid assets after closing. These post-close reserves are typically expressed as a number of months of PITIA (Principal, Interest, Taxes, Insurance, and HOA if applicable) for the subject property. The standard liquid asset reserve requirement for DSCR loans is usually 6 months of PITIA payments, though some lenders increase this to 9 or even 12 months for large loan amounts (e.g., $1.5 million+), lower DSCR ratios or more complex property types. Additionally, some lenders will have lower reserve requirements, such as only 3 months of PITIA, typically for lower risk deals for strong borrowers.

The reason for these liquid asset requirements is to lower the risk of default. While most DSCR Loans are underwritten with DSCR ratios over 1.00x, indicating that the property itself should provide enough cash flow to cover the PITIA payments each month, the real world isn’t so neat and simple. For example, many DSCR Loans are for acquisitions of vacant properties where the DSCR ratio is based on market rent – but it will often take a bit of time for the new owner (borrower) to rent out the property and start collecting rent. Additionally, DSCR ratios don’t take into account any vacancies (typical over the life of the loan due to tenant turnover and maintenance) or seasonality (for example, a vacation rental that has slow “offseason” months and other months where the majority of revenue is obtained).

In addition, the unfortunate reality that most real estate investors know is that tenants don’t always pay rent in full and on time, but in these cases, the debt services payments are still due – and the borrower still needs to come up with the payment while they work to re-tenant the property or collect rents due. As such, these liquid asset requirements ensure a cushion where the lender has increased comfort that the sponsor can cover PITIA payments in case the property is not providing cash flow to cover the monthly payments for whatever reason, whether from vacancy, seasonality, tenant non-payment, or even as expected for a sub-1.00x DSCR loan).

While these requirements are called “reserves” in the industry, this term can be confusing because required escrows (such as the requirement to pay the taxes and insurance to a servicer-held escrow account as part of PITIA payments) are also frequently called “reserves” as well. As such, to avoid confusing this concept with the escrows requirement, it is generally better to refer to these “reserves” as “liquid asset requirements,” both for precision and to limit confusion among investors.

.png)

Liquid assets used for reserves can include:

Cash in checking or savings accounts (owned or fully controlled by guarantor)

Brokerage Accounts containing stocks and bonds

Retirement Accounts such as 401(k)s or IRAs

Life Insurance accounts (cash value)

Crypto (some lenders are starting to accept Bitcoin or even other crypto currencies like Ethereum)

Cash-Out Proceeds from Cash-Out Refinances

It is important to note that for some of the acceptable forms of liquid asset reserves, DSCR lenders apply what is often called a “haircut” to the value of the liquid assets for the purposes of counting it towards the qualifying requirement (e.g. 6 months of PITIA). The “haircut” refers to the percentage which is counted towards the requirement (or more accurately, what is not counted). Essentially, liquid assets that are not quite as liquid or as stable in value as true cash are not counted at 100% of their value (as of the date of the documentation). Since the purpose of this requirement is for a cushion to cover months where cash flow won’t cover PITIA payments, actual cash in a checking account or savings account is ideal, since it is both extremely liquid (it can be used to make a PITIA payment immediately through a click of a button) and stable in value (since held literally as cash, the “cash value” will not change like a stock share which fluctuates in value daily).

While cash liquid assets are typically counted with no discounting or “haircut”, DSCR Lenders will typically reduce “what is counted” for other forms of liquid assets that are less liquid and stable in value. For example, if a DSCR Loan borrower needs to cover a PITIA payment with funds that are being used in a stock brokerage account, he or she must sell the stocks and then transfer the proceeds to a bank account, a process which is less liquid because it would likely take a few business days to be able to complete the process from liquidation of stocks to making the payment. Additionally, the value of these stocks is less stable because the values of stocks can go up or down daily so there is always the risk that the value of stocks decrease in the time between when the borrower applied for the loan and when he or she needs to sell to cover a PITIA payment. As such, DSCR Lenders will typically apply a 10% discount to liquid assets that are stocks or bonds held in brokerage accounts to account for the lower liquidity and value stability versus cash. This means, for example, that if the sponsor provides a brokerage account statement with stocks and bonds worth $100,000 during the qualification process, the lender will count only $90,000 (or a discount – “haircut” - of 10%) towards the liquid assets reserve requirement.

This concept continues for retirement accounts such as IRAs and 401(k)s. Like stocks and brokerage accounts, these accounts are less liquid and provide greater risk of a value drop than cash or cash equivalent accounts. These retirement accounts typically have even less liquidity than standard brokerage accounts, as there can be vesting requirements and longer / more complicated processes for selling assets and moving them to a cash account that could be used to make a PITIA payment. Additionally, these accounts can often have rules and fees associated with liquidating or taking out to use early, that will reduce their value (i.e. if moving $100,000 from the account to cash incurred a 10% early liquidation fee). For these reasons, retirement accounts are even less liquid and have lower immediate cash values, so they are often subject to a larger haircut (typically 20% or 30%, so only 70% or 80% of their value at application would be counted towards the liquid asset reserves). Also note that in cases where a sponsor has a loan outstanding that is secured by a retirement account (such as a so-called “401(k) loan”), this amount would need to be deducted from the vested balance as well.

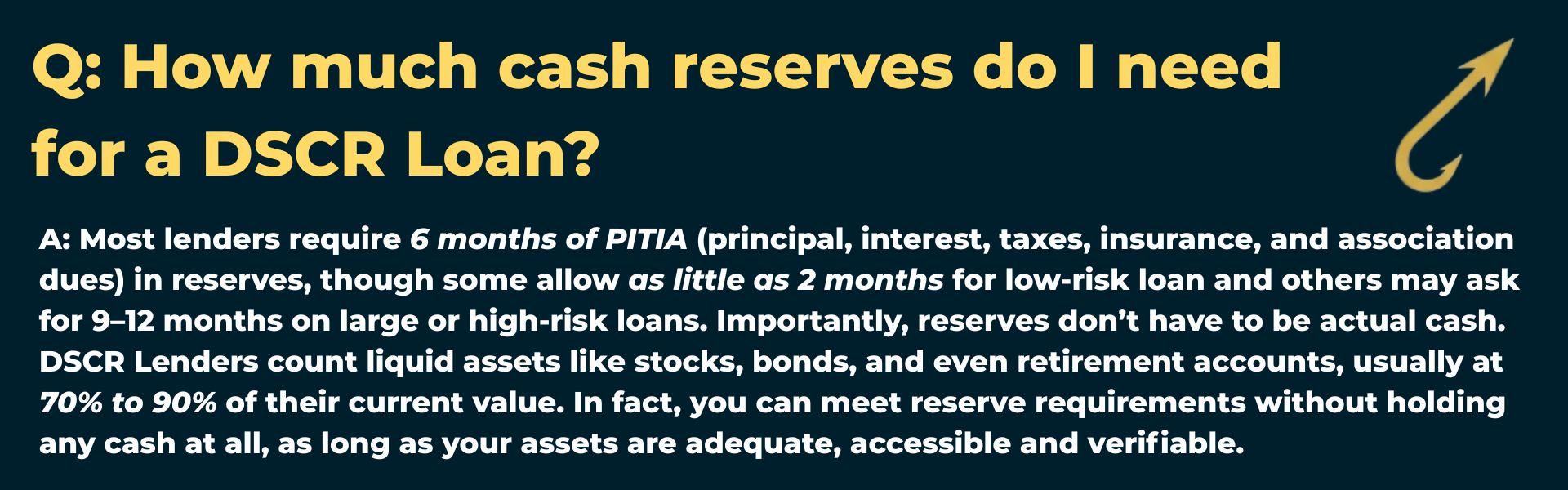

Q: How much cash reserves do I need for a DSCR loan?

A: Most lenders require 6 months of PITIA (principal, interest, taxes, insurance, and association dues) in reserves, though some allow as little as 2 months for low-risk loan and others may ask for 9–12 months on large or high-risk loans. Importantly, reserves don’t have to be actual cash. DSCR Lenders count liquid assets like stocks, bonds, and even retirement accounts, usually at 70% to 90% of their current value. In fact, you can meet reserve requirements without holding any cash at all, as long as your assets are adequate, accessible and verifiable.

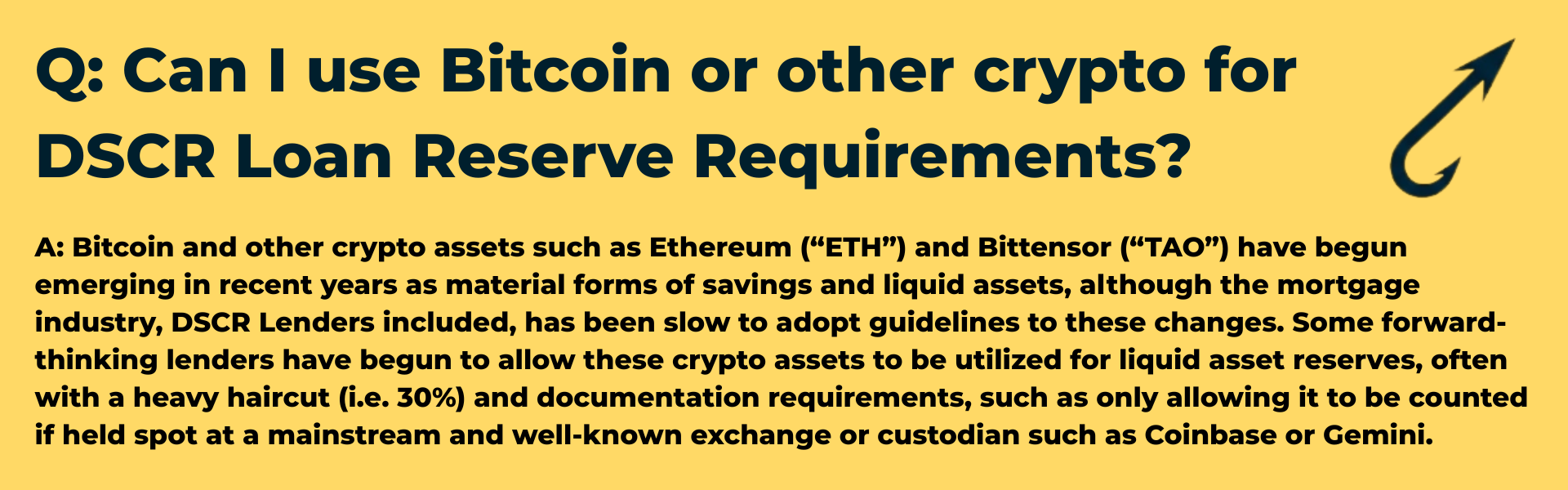

Q: Can I use Bitcoin or other crypto for DSCR Loan Reserve Requirements?

A: Bitcoin and other crypto assets such as Ethereum (“ETH”) and Bittensor (“TAO”) have begun emerging in recent years as material forms of savings and liquid assets, although the mortgage industry, DSCR Lenders included, has been slow to adopt guidelines to these changes. Some forward-thinking lenders have begun to allow these crypto assets to be utilized for liquid asset reserves, often with a heavy haircut (i.e. 30%) and documentation requirements, such as only allowing it to be counted if held spot at a mainstream and well-known exchange or custodian such as Coinbase or Gemini.

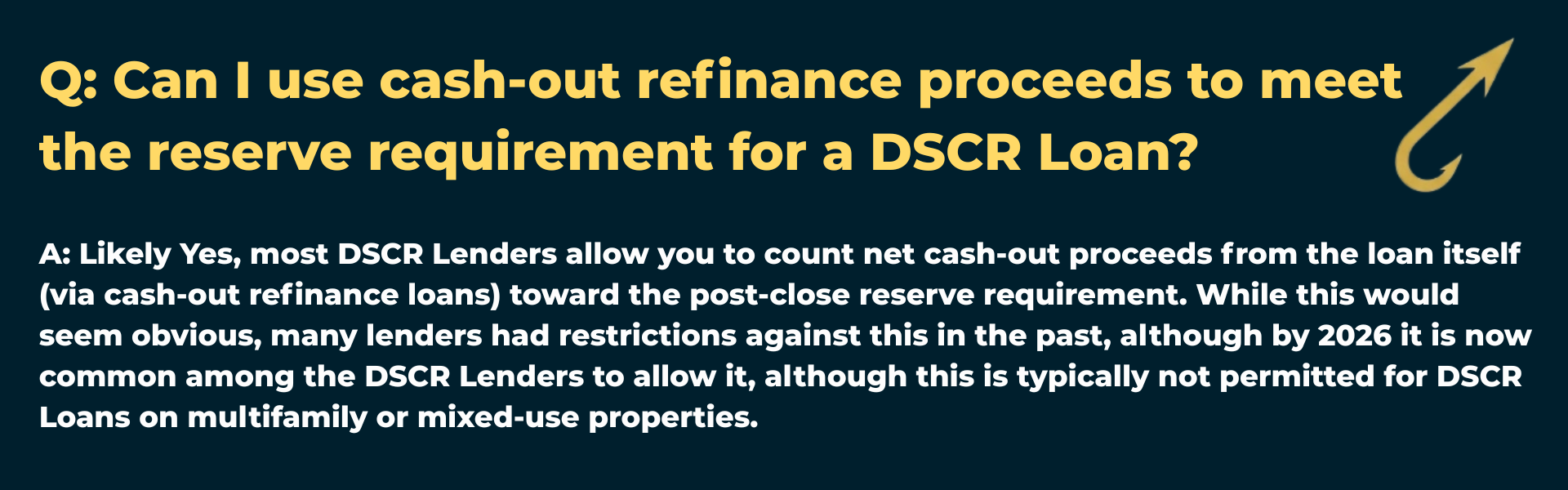

Q: Can I use cash-out refinance proceeds to meet the reserve requirement for a DSCR Loan?

A: Likely Yes, most DSCR Lenders allow you to count net cash-out proceeds from the loan itself (via cash-out refinance loans) toward the post-close reserve requirement. While this would seem obvious, many lenders had restrictions against this in the past, although by 2026 it is now common among the DSCR Lenders to allow it, although this is typically not permitted for DSCR Loans on multifamily or mixed-use properties.

Q: Can I use retirement or investment funds as reserves for a DSCR Loan?

A: Yes, most lenders allow stocks, bonds, brokerage accounts, and retirement funds to count toward reserve requirements. But because these assets are less liquid than cash, lenders apply a “haircut” to account for access delays, penalties, or volatility. For example, 401(k)s and IRAs are usually counted at 70–80% of their value, due to early withdrawal rules and liquidation fees.

While not the most common reserve issue, one topic that occasionally trips up DSCR borrowers is whether funds held in a business bank account can be used to meet post-close reserve requirements. Since many DSCR Loan borrowers are self-employed or business owners, and therefore less likely to pursue conventional financing, it’s not unusual for much of their liquidity to be tied up in operating accounts unrelated to their real estate ventures.

For example, a sponsor may own a restaurant or a landscaping company with one set of partners, and simultaneously be acquiring rental properties on their own or with a different set of investors. In these cases, DSCR Lenders will only count business account funds toward reserve requirements if the guarantor has 100% access and control over those funds. That typically means, the borrower (guarantor) must be the sole owner of the account or demonstrate unrestricted withdrawal access without requiring approval from other signers or business partners.

If access to those funds requires any third-party approval, they won’t be eligible as liquid asset reserves under DSCR Loan guidelines. While this issue doesn’t affect most deals, it can be a deal-killer in certain situations, particularly those with diversified portfolios and overlapping ownership structures. It’s important for investors potentially needing business funds to satisfy DSCR Loan liquid asset requirements to either maintain reserves in a personal account or be prepared to document full access to business-held assets.

.png)

While most DSCR Loans require these liquid asset reserves, there’s one key exception available to investors completing rate-and-term refinances. For some DSCR Lenders, liquid asset reserve requirements can be fully waived in certain low-risk non-cash-out refinance scenarios.

To qualify for a reserve waiver on a rate-term DSCR Loan refinance, the loan must meet three conditions: 1) The property must contain 1–4 units (i.e. not multifamily or mixed-use), 2) the new DSCR Loan must result in at least a 10% reduction in monthly principal and interest payment and 3) all guarantors’ mortgage (including both owner-occupied and investment properties) payment history must show no more than one 30-day late payment in the past 12 months.

This waiver follows the logic that if the borrower has successfully made payments on the current loan, and these payments are reduced with the new loan, they are a solid bet not to default and don’t need to prove a cushion. For these specific rate-term refinance DSCR Loan instances, the borrower can qualify for zero liquid assets reserves required at close.

This feature can be especially helpful for investors who are property-rich but cash-light, allowing them to optimize their loan without needing to park months of liquidity in a personal or business account just to satisfy this particular qualification requirement.

.png)

One final thing to remember about DSCR Loan liquid assets reserves requirements are for rate-term refinances where the borrower has to “bring money to the table” i.e. the new loan proceeds are less than the sum of the old loan payoff, closing costs and upfront escrows. These cases, also sometimes referred to as “cash-in refis,” will typically require the standard three to nine months of PITIA as liquid asset reserves. However, the borrower will have to provide documentation for these liquid assets in addition to the difference between the new loan and the payoffs. This is because the borrower cannot “get credit” for liquid assets for post-close reserves that will be used at closing. While this can seem obvious when broken down like this, sometimes borrowers can forget about this when planning for loans and might be left scrambling without being able to “double count” these assets for reserves and for the needed “cash brought to the table.”

For most DSCR Loan programs, the standard minimum down payment is 20%, meaning the maximum loan-to-value (LTV) is 80.0%. This is the common cap across nearly all lenders for acquisition DSCR Loans, regardless of property type, and reflects industry risk tolerance for business-purpose loans without income verification.

Some lenders do offer 85.0% LTV (15% down) options, but these are rare and come with tight restrictions, typically limited to long-term rental properties only, and requiring a minimum DSCR of 1.25x along with a very high credit score. These higher-leverage programs are also more likely to carry pricing add-ons, stricter reserve rules, or reduced flexibility on things like short-term rentals or mixed-use.

While 80.0% LTV is generally the ceiling for purchases, many investors still choose to put down 25% or more in order to secure better interest rates and loan terms. Lenders typically offer pricing incentives for lower LTV tiers (like 65.0% or 70.0%), especially when paired with strong credit and experience.

Most DSCR Lenders allow gift funds to be used toward the down payment or closing costs on 1–4 unit residential properties, but they come with restrictions, including typically requiring the investor to contribute at least 5 or 10% of the purchase price from their own funds and documenting gift funds with a formal gift letter and supporting transfer paperwork. Additionally, gift funds are generally not allowed for down payments for DSCR Loans secured by multifamily (5+ unit) or mixed-use properties. As a rule of thumb, DSCR loans still require borrowers (guarantors) to show personal financial capacity, and using gift funds doesn’t override the need for strong reserves or sponsor-level qualifications.

In DSCR loan underwriting, lenders require a minimum of 60 days’ worth of account statements (generally, Two Official Monthly Statements) for any liquid asset accounts being used to document liquid asset reserve requirements or down payment funds. The review is limited strictly to that two-month window, and activity prior to that period is generally not evaluated or requested.

Within this 60-day review period, any large incoming deposits, commonly defined as amounts of $10,000 or more, must be “sourced.” This means the borrower must provide documentation establishing the origin of the funds, along with a brief Letter of Explanation (LOE) if needed. The standard is not tied to income or debt ratio calculations, but rather to anti-money laundering (AML) compliance and risk mitigation protocols required across the mortgage industry.

Acceptable sources ordinarily include investment redemptions, business distributions, asset sales, or inter-account transfers, provided sufficient supporting documentation is included (e.g., closing statements, sale contracts, brokerage confirmations, or executed loan agreements). Funds that appear inconsistent with the borrower’s known financial profile—or lack sufficient paper trail—may be excluded from the reserves calculation or flagged for further review.

This sourcing requirement applies only to the accounts disclosed for liquidity verification. DSCR Lenders do not conduct full forensic reviews of unrelated accounts and will not request documentation beyond the 60-day scope unless there is a specific red flag. The objective is not to disqualify legitimate funds, but to ensure transparency and traceability in compliance with federal lending oversight and to avoid potential mortgage fraud.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.