.png)

Most DSCR Loan borrowers close loans in the name of an LLC or other entity for liability protection and tax strategy. While that’s standard practice, it also introduces a layer of scrutiny: DSCR Lenders require a complete and compliant set of entity documents to ensure the borrower has legal authority to own the property and enter into the loan.

Problems surface when the DSCR Lender’s legal team reviews the entity documents and finds gaps, inconsistencies or compliance issues. Sometimes these are small, like a missing resolution. Other times, they’re structural, such as an LLC not being properly registered in the state where the property is located. These issues often come up late in underwriting and can derail a DSCR Loan closing timeline if not addressed quickly.

Unfortunately, the reality is that the large majority of DSCR Loans today vest property title in an entity like an LLC or Trust, and a large majority of these entity borrowers have problems with their documentation packages requiring changes and updates. There are many minor nuances involved with borrowing through an LLC, and many DSCR Lenders take the time to have active, fully-licensed lawyers comb through the entity document packages to make sure that even small errors don’t exist, and if errors are found, they are fixed. These seemingly small issues can have outsized risks for the lender down the line, such as potentially voiding foreclosure rights or even the debt itself if for example the borrowing entity wasn’t actually allowed to take on debt (in some of these cases, if that can be proven in court, the lender faces the catastrophic situation of being “out” all of the money owed – or “not owed” if determined by the court!). While the following three examples are common and major issues that can pop up for DSCR Loans, entity documents issues are frequent and wide-ranging, so it definitely pays to pay attention in this area.

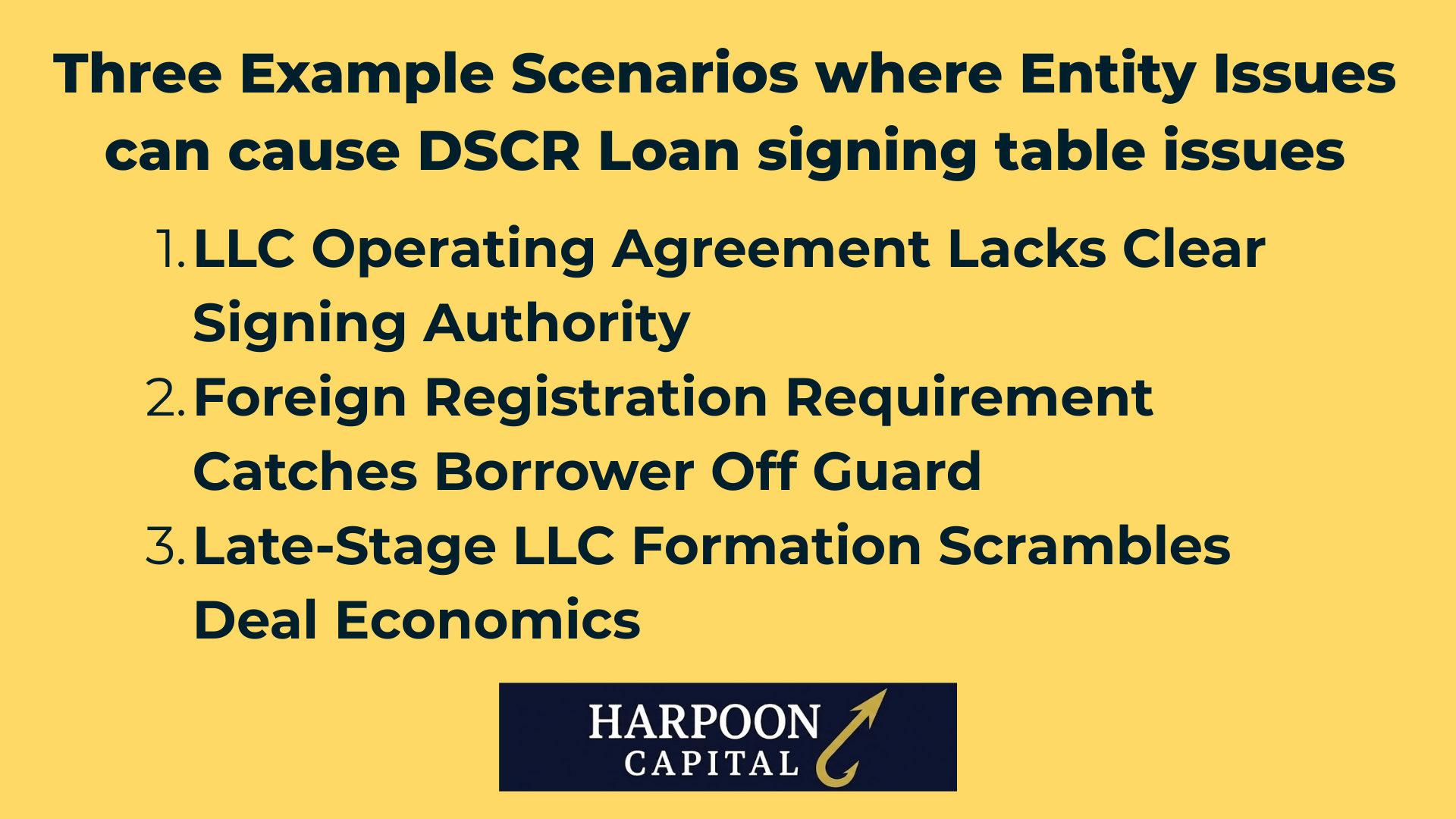

An investor formed an LLC years ago to hold multiple rental properties but never updates the operating agreement to spell out who can sign for mortgage loans or encumber property. When applying for a DSCR Loan cash-out refinance, the DSCR Lender requests evidence that the signer, one of three members, has the authority to bind the company. The title company reviews the operating agreement and finds it silent on borrowing powers or management authority. As a result, underwriting halts until a formal amendment or corporate resolution is executed and signed by all members. One partner is out of state and difficult to reach, forcing a two-week delay while notarized signatures are collected and filed. What should have been a straightforward closing turns into an administrative scramble simply because the original LLC documents weren’t drafted with financing in mind.

A common structure for real estate investors is to form an LLC in a business-friendly state such as Delaware, Wyoming or Nevada while buying property elsewhere. An investor does just that; her LLC is registered in Delaware, but the property securing her DSCR Loan is in Florida. During underwriting, the DSCR Lender’s legal review flags that the LLC hasn’t been registered as a foreign entity in Florida, meaning it technically isn’t authorized to conduct business or hold title in that state. To move forward, the investor must file for a Certificate of Authority with the Florida Secretary of State, pay the filing fee and designate a local registered agent. While not complex, the process takes about ten business days and can’t be skipped. The delay pushes closing into the next rate-lock period, increasing costs and adding frustration over an easily preventable oversight.

An investor is purchasing a single-family rental in Illinois under his personal name, planning to use a DSCR Loan with a five-year prepayment penalty structure that offers the best rate. Midway through underwriting, the DSCR Lender informs him that they only allow prepayment penalties for DSCR Loans made to entities in Illinois, not to individuals. If he closes in his personal name, the loan will have to be priced with a much higher interest rate, wiping out the deal’s projected cash flow. With just days before closing, the investor scrambles to create an LLC, obtain an EIN, draft an operating agreement, and coordinate a title update so the entity can take title instead. The rushed process adds filing fees, legal costs and nearly two weeks of delay. While the loan eventually closes, the stress and expense could have been avoided if entity structuring had been addressed before the application stage.

While entity documentation issues are widespread, the good news is that they are relatively easy to avoid with preparation, and typically fairly fixable and not “deal-killers,” more like “delay-delayers.” Even a delayed deal can cause significant time and money, and sometimes, especially on tight purchase timelines in sellers’ markets, can actually cause a DSCR Loan to completely fall apart. As such, it’s smart to prepare well and know all the rules and potential issues ahead of time to avoid any potential trouble.

When it comes to borrowing through entities, cutting corners early almost always costs more later. Many investors rush to create their LLCs online or through budget filing services, only to find out during underwriting that their operating agreement doesn’t authorize anyone to borrow money, encumber property or sign loan documents. At that point, they’re forced to hire an attorney anyway, only now it’s under time pressure, with closing dates looming.

It’s worth spending a few hundred dollars more upfront to have an experienced real estate attorney or a company that specializes in DSCR Loan ready LLCs draft your documents correctly the first time. A properly written operating agreement should clearly define management authority, outline who can bind the entity in loan transactions and be consistent with how the LLC is registered with the state. Getting this foundation right not only prevents future delays but also provides long-term legal protection for your investments.

Even the best-formed LLCs can trigger problems if they’re not properly maintained. Lenders routinely verify an entity’s Certificate of Good Standing during underwriting to confirm it’s active and compliant with all state filing requirements. Forgetting to file an annual report, missing a renewal deadline or failing to pay a small state fee can cause your entity to show as “inactive” or “delinquent,” instantly halting the loan process. The same goes for foreign registration, one of the most common, and preventable, DSCR Loan issues. If your LLC was formed in one state but owns property in another, you’ll almost always need to register as a foreign entity in the property’s state before you can close. The fix is simple but not instant, it can take a week or two for processing, which can easily blow a rate lock or purchase timeline. Setting calendar reminders for annual filings, renewals, and state registration deadlines keeps your entity “funding-ready” year-round.

Not all entities are treated equally when it comes to DSCR Loans and vesting simplicity. Trusts, Series LLCs and structures more complex than a standard LLC often have unique signing rules and documentation requirements that can trip up even experienced investors. Some DSCR Lenders allow these structures only under specific conditions, such as requiring all trustees or series managers to sign or mandating separate EINs and operating agreements for each cell in a Series LLC. Others don’t permit them at all. If you’re borrowing through a trust, confirm early how your DSCR Lender defines signing authority: do they require both the trustee and the grantor to sign, or just the trustee? If you’re using a Series LLC, clarify whether the lender will need documentation for both the master entity and the individual series cell. Sorting this out during application instead of at closing gives you time to prepare the correct resolutions, EINs, and document sets, avoiding last-minute chaos. The key is to treat entity clarity as part of loan prep, not loan cleanup, because once a deal is deep in underwriting, every missing document becomes a clock ticking against your closing date.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.