.png)

Many investors come to DSCR loans expecting a light-touch underwriting process, no tax returns, no W-2s, no DTI calculations. However, some borrowers are surprised to discover that DSCR Lenders still have strict rules around sourcing large deposits. Even though your personal income isn’t under review, your financials around down payment and liquid assets are.

The logic is simple: lenders need to know the money funding the loan is yours, legitimate, and not secretly borrowed. They also have to comply with federal anti-money laundering (AML) regulations, even as private lenders under the conventional, government-subsidized system. For real estate investors, many of whom have irregular project-based income, shifting business cash flows or frequent transfers between accounts, this can create unexpected friction.

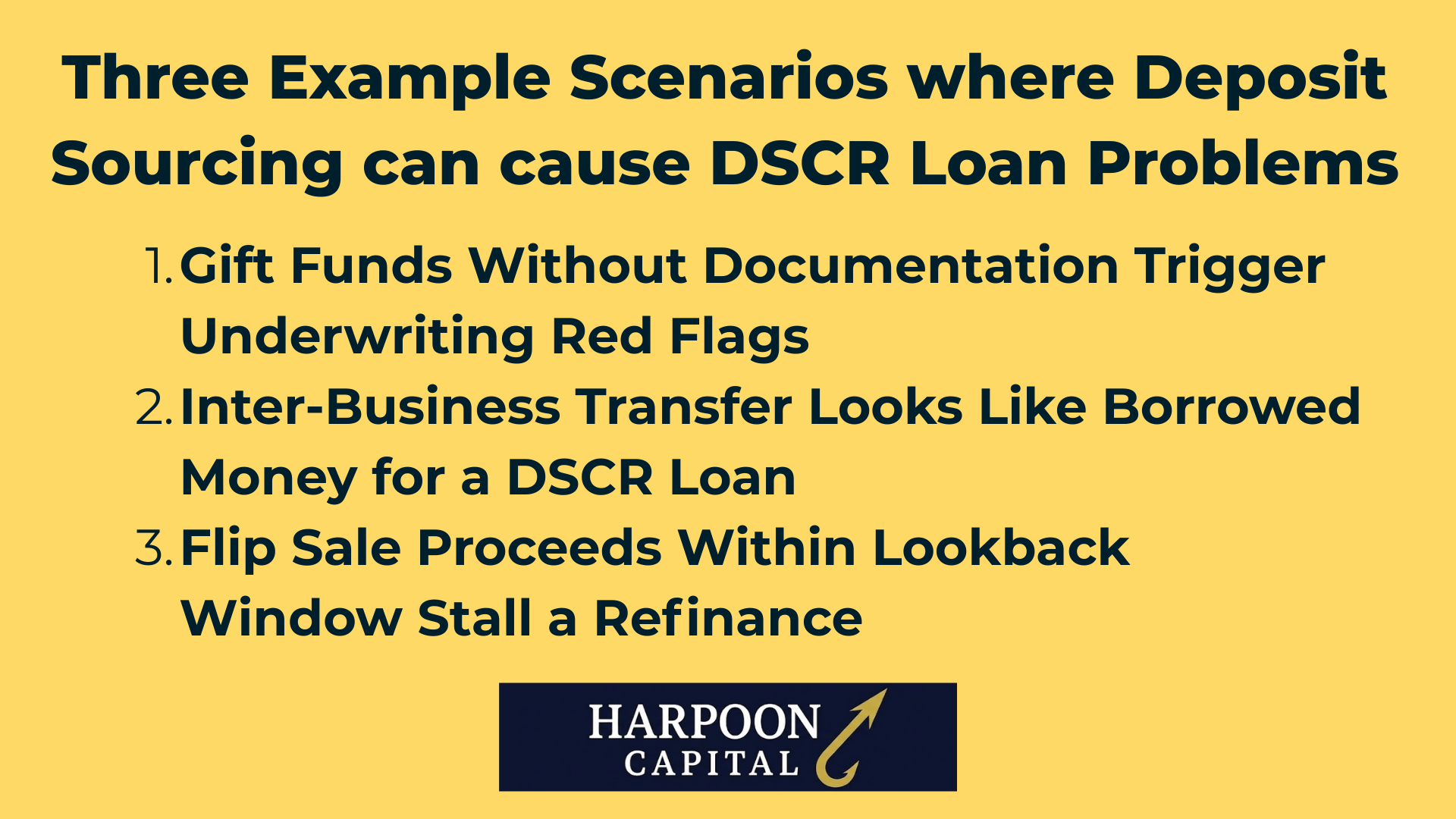

An investor’s parents wire $50,000 to help with the down payment on a DSCR purchase. The borrower assumes that because DSCR Loans don’t verify personal income, the DSCR Lender won’t care where the funds came from. During underwriting, however, the lender flags the transfer as an unexplained large deposit within the 60-day bank statement review window. Even though gift funds are allowed as long as the amount doesn’t make up over 90% of the down payment, the DSCR Lender requires a formal gift letter, a copy of the sender’s bank statement showing the withdrawal and evidence the gift is not a loan that must be repaid. The borrower’s parents are traveling abroad and slow to provide documentation, delaying final approval by nearly two weeks. The deal still closes, but the seller demands a per-diem extension fee, adding $1,200 in unexpected costs simply because the “family gift” wasn’t disclosed and sourced upfront.

A real estate investor who owns multiple businesses moves $120,000 from one company’s operating account into his personal checking to show sufficient liquidity for a DSCR Loan refinance on one of his rental properties. The funds are legitimate, his share of profits from a recent project, but the business has two other partners listed on the account. When underwriting reviews the statements, they flag the transfer as a potential loan or shared funds not solely controlled by the borrower. The DSCR Lender requires a Letter of Explanation (LOE) and documentation confirming that the transfer represents the borrower’s own earned proceeds and that no repayment is owed to the company or partners. Coordinating signatures and corporate records takes over a week, pushing the DSCR Loan past the original funding date and creating a short gap between payoff and new disbursement.

An investor who dabbles in different strategies such as flips and turnkey rentals, applies to refinance a rental property with a DSCR Loan expecting $60,000 in cash-out proceeds. Two weeks before submitting the DSCR loan application, he deposits $75,000 into his checking account from the sale of a recent fix-and-flip. Because the deposit falls inside the lender’s 60-day review period, underwriting requires full documentation: the prior property’s HUD-1 settlement statement, wire confirmation, and proof that no short-term loan or partner financing was involved. The title company from the flip has already archived its records, forcing the borrower to hunt down old documents and payoff wires. The back-and-forth adds three weeks to the process and pushes the lock extension cost to nearly $2,000, erasing most of the refinance’s rate savings. The funds were legitimate, but lacking quick access to clean documentation, common for frenzied flippers, turned a routine refinance into a timing and cost problem.

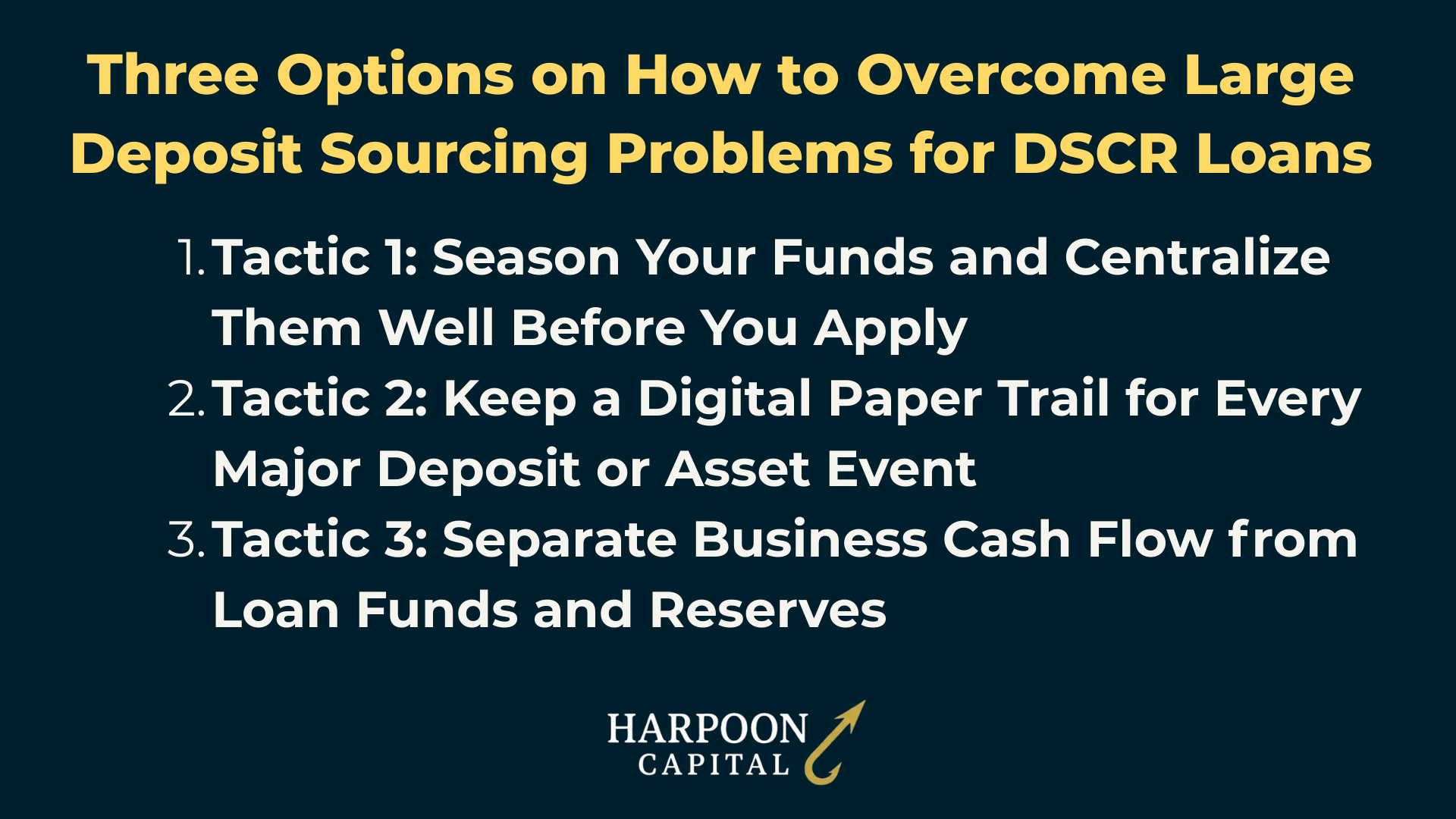

While these large deposit sourcing issues can cause serious problems for DSCR Loans, they are mostly preventable when understanding the DSCR Lender’s rules around “large deposits,” by budgeting enough time between bank statements and big deposits and by keeping clean and tidy records. A well-prepared borrower – both in terms of understanding exactly what will get flagged, and what won’t show up in due diligence, and staying tightly organized – will essentially guarantee this isn’t an obstacle worth worrying about.

The cleanest way to avoid sourcing headaches is to plan ahead. Move your closing funds and reserve capital into the account you’ll use for underwriting at least 60–90 days before starting a DSCR Loan application. DSCR Lenders generally only review the two most recent months of statements, so if your funds are already sitting in the account, steady and untouched, they’ll be considered “seasoned,” meaning no explanation or paper trail is required. This isn’t about hiding sources; it’s about avoiding the chaos of last-minute transfers that trigger documentation requests. Investors who routinely move cash between projects, partnerships, or businesses should designate a single account for DSCR Loan transactions. When the lender reviews statements, what they see should be a straightforward story: money in place, stable, and clearly yours.

When large deposits are unavoidable, documentation is your best friend. If you’re selling a property, liquidating an investment or receiving a partner distribution, save every supporting document, wire confirmations, HUD or closing statements, contribution agreements, or brokerage settlement reports. The key is to connect the dots between where the money came from and when it arrived. Underwriters don’t assume wrongdoing; they just need to prove the funds weren’t borrowed or part of another party’s assets. Having a neatly labeled digital folder ready to send eliminates the scramble of tracking down old records or waiting on title companies to reopen archived files. The few minutes it takes to organize paperwork upfront can save weeks of delays and hundreds, or even thousands, of dollars in rate-lock extension fees later.

For active investors juggling multiple projects, it’s tempting to pull DSCR Loan capital from the same business account used for renovations, payroll or rental income. Unfortunately, those irregular inflows and outflows can make DSCR Lenders nervous, especially when unexplained transfers resemble short-term loans. The solution is simple: use a clean account, personal or dedicated to investments, for closing funds and reserves. Keep it quiet in the weeks leading up to underwriting: no incoming wires from other entities, no big outgoing transfers. When your bank statements look stable and self-contained, the underwriter has no reason to question them. A tidy, isolated account tells a reassuring story: the money is yours, it’s seasoned, and it’s ready to close.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.