.png)

Rate Locks for DSCR Loans are very different, and far more confusing, than what most real estate investors expect, particularly if they are used to funding deals with conventional lenders or other DTI-based loan programs. In consumer lending, a “lock” generally means the borrower has secured a specific interest rate number for a set period. For DSCR Loans however, a lock (if offered at all) applies to a day’s rate sheet or base pricing stack, not to a single guaranteed rate.

That distinction matters because DSCR Loan pricing is built from multiple moving parts, including loan-level pricing adjustments (“LLPAs”) that are known upfront in the process. Examples include property type and qualifying credit score, as well as the “base rate” stack tied to overall market rates, and LLPAs that can change later on in the process when more information, chiefly the appraisal, comes in, such as LTV and DSCR. Additionally, there are multiple LLPAs and loan provisions that can be changed throughout the process, even for borrower preference or changing minds, such as adjustments for loan amount, loan structure and even prepayment penalty choices. If any of those terms change during underwriting, or if the borrower decides to tweak the structure (say, trading higher closing fees for a lower rate, or switching prepayment penalty provisions), the “locked” DSCR Loan is re-priced against the locked rate sheet and base stack, not the exact interest rate number originally discussed.

The result is that many borrowers sometimes feel blindsided. They think “locking” secures their interest rate, only to learn later that restructuring the deal or updated underwriting numbers can still move the final rate and points. Because this is often very confusing and/or poorly explained, and many DSCR Lenders avoid offering locks altogether (unless sometimes through experienced mortgage brokers who can manage borrower expectations), confusion and frustration are common when rates and terms change for the worse midway through a DSCR Loan deal.

In volatile rate environments like the past few years, this issue is magnified. Over the 30–45 days it typically takes to close a DSCR Loan, the base rate stacks can shift significantly. A deal penciled tightly at application, with DSCR ratios hovering around 1.00x or 1.10x, or cash-out sized right up to program limits, may suddenly require more points, a higher rate or even a full restructuring when repriced. Borrowers, unfamiliar with how DSCR Loan rate sheets truly work, often interpret this as a “bait and switch” when in reality it’s simply the nature of the product.

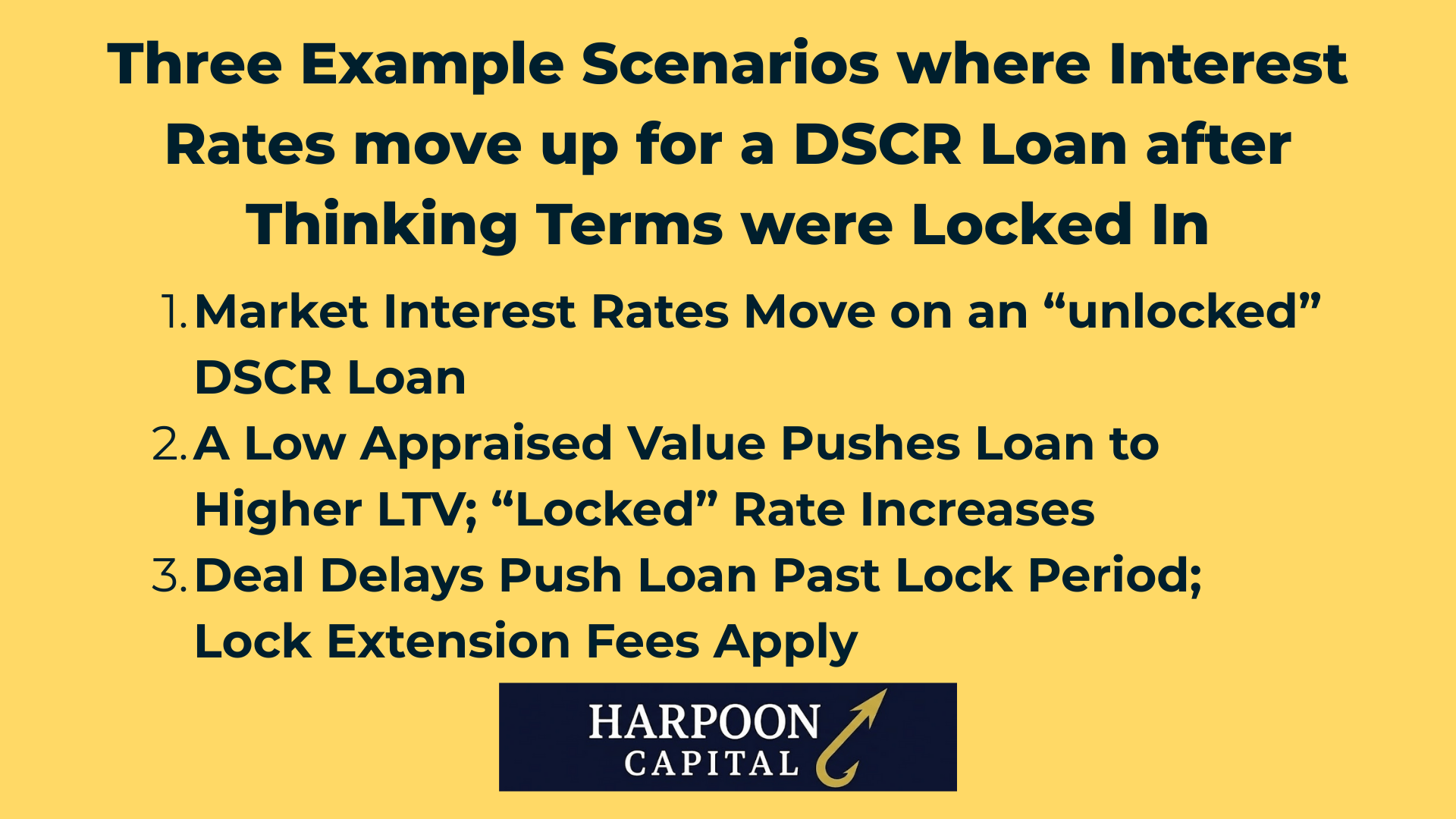

Because DSCR loan locks don’t operate like conventional mortgage locks, a moving interest rate, “locked” or not, is a common issue that causes frustration and puts DSCR Loans in jeopardy, especially in recent years where market interest rates frequently “spiked” and moved higher in short periods of time. The below are three examples of how confusion on DSCR Loan locks, or rapid changes in market rates can cause trouble with DSCR Loans trying to get across the finish line.

An investor has used conventional loans to build a portfolio of four rental properties to provide cash flow to supplement their income. However, after going under contract with a fifth rental property, he realizes that with four mortgages to his personal name and tax strategies lowering his income, he can’t qualify for another conventional loan with his current DTI. He researches other options online, and finds a direct DSCR Lender to provide a DSCR Loan for this purchase, his first time using this financing option. He signs a term sheet with an interest rate of 6.25% and after plugging in the loan terms to his trusty Excel tool, he is confident the deal is a winner.

However, over the course of the next month, while he gets used to the different documents he needs to provide (he creates his first LLC to vest the property in), market rates spike because of an unfavorable CPI report. The week before closing, his DSCR Lender informs him that his rate is now 7.25% since market rates moved. The DSCR Lender doesn’t offer locks because it finds that it’s too confusing to explain the concept of “rate sheet” locks versus “rate locks” and doesn’t want to create friction in finding borrowers, especially those new to DSCR Loans. The investor, used to knowing and “locking” the rate upfront with his conventional lender, is blindsided and enraged, and wants to move to another lender, but other DSCR Lenders are dealing with the same market rate moves, and are all quoting him above 7%. Unfortunately, the 6.25% rate he assumed he was getting is gone.

An experienced real estate investor specializing in duplexes has owned a two-unit property for several years and online sources indicate that it has significantly increased in value since he purchased it five years ago, estimating it now worth $1,000,000 versus the $600,000 at which he bought it. He works with a mortgage broker who sells him on the idea of doing a cash-out refinance DSCR Loan on the property, to access some of the capital “trapped” in the property in order to continue expanding his portfolio. This investor has been around awhile and seen different real estate cycles, so he makes sure to get a rate lock on his DSCR Loan when deciding on quoted terms, which include an interest rate of 6.75%, a number which will still allow the tenanted property to cash flow post-refinance into a larger loan. He has a low leverage loan now, and he chooses to balance accessing equity via cash-out with maintaining cash flow (instead of maximizing leverage), planning for a 65.0% LTV ratio ($650,000 loan amount).

When the appraisal comes in a few weeks into the process, the appraised value is lower than expected, at $866,667 instead of $1,000,000. A $650,000 loan amount is still eligible for a cash-out refinance DSCR Loan since the lender goes up to 75.0% LTV on cash-outs ($650,000 ÷ $866,667 = 75.0%). The investor is disappointed in the value, but knows it’s just an appraiser’s opinion, and he can still get the same loan amount and proceeds. However, near closing, he is informed that his interest rate is now 7.50%, since the rate needs to be adjusted upwards for the higher risk LLPA of a 75.0% LTV versus the pricing at 65.0% LTV. He is shocked and confused, thinking his interest rate was locked, however his broker informs him that he is locked to a “rate sheet” not an interest rate number, and that sheet requires a much higher rate because of the newly calculated LTV ratio.

A real estate investor closely follows the market, watching Bloomberg News daily as well as his local housing listings to strategically make moves to purchase properties when everything lines up – falling mortgage rates and low-priced opportunities in his area. After a month of inflation and jobs data indicate that the Federal Reserve will likely be cutting rates aggressively in the near future moves general mortgage market rates down, he spots a great underpriced triplex in his market and goes under contract. He calls his DSCR Lender and locks in terms, and as a sophisticated investor understands he is locking to a sheet, not a specific rate, and already has “plan Bs” in mind in case the final numbers differ, such as a rate buy down plan or switching to a Partial-IO structure if needed.

The DSCR Loan process unfolds as expected, everything appears on track and he knows how to deal with unfortunate, but not uncommon, headaches such as it taking a few extra days to coordinate the property inspection, and then the appraisal on a turnkey triplex with each of the three units occupied with tenants. He diligently pushes the seller to coordinate, and patiently pushes for leases to be tweaked and altered, as the existing ones were poorly scanned and illegible, and one of the tenants was only on a “verbal” agreement, which also adds a week to the process. While dealing with this seller, he is delayed a little bit providing all of his “needs list” documents such as his LLC agreement and final insurance binder, but makes sure those documents are in a couple of days after the appraisal comes back, confirming value and giving the green light towards close, even though the whole process took a couple of weeks longer than expected.

Approaching the close date, the borrower is informed that he is required to pay an additional $5,000 for a “rate lock extension” because his lock period had expired after 30 days. He feels blindsided and upset from this fee, and angry because a lot of the delays were outside of his control, especially the seller’s lack of coordination with the tenants and inspector and appraisers and the issue with the leases. While he could have been quicker on his needs list, the final underwriting on the DSCR Lender’s side took a few extra days as well, since due to rates dropping and the market heating up, their underwriting team was a bit backed up. However, market rates had ticked up slightly during this period, and starting the process over with a new DSCR Lender would likely result in a higher rate than he signed up for, ruining the benefits of his perfect timing.

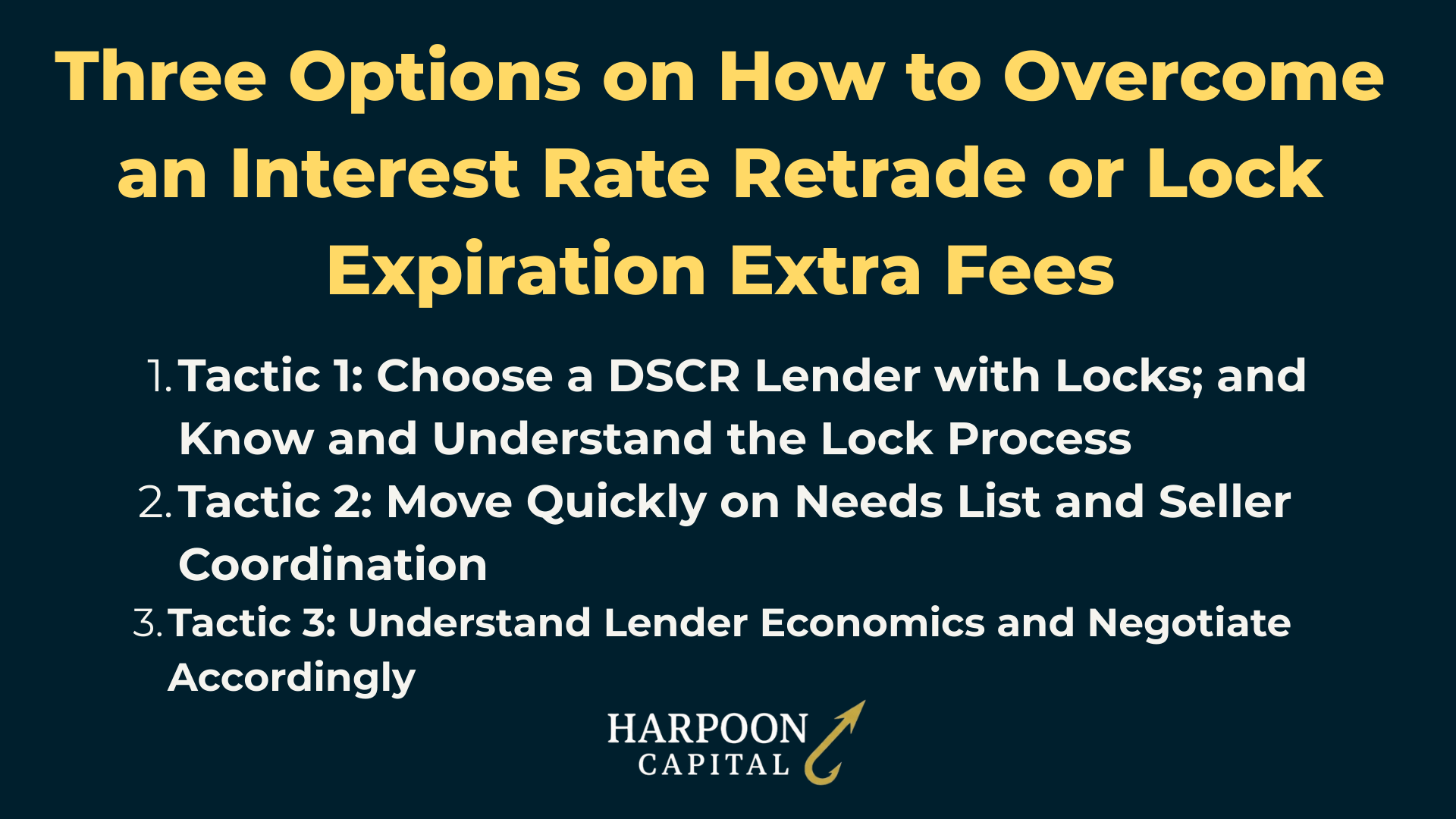

Additional fees or higher interest rates dropped on borrowers late in the game are one of the most aggravating aspects of DSCR Loans and are unfortunately fairly common due to many factors, including the confusion around and infeasibility of truly “locking rates” for these loans, as well as the reality that deals generally take longer than expected and as such, lock extension fees are an additional painful blow at the end of an already-delayed deal. However, there are several tactics best-informed borrowers can do to minimize the chances of landing in these frustrating and unfavorable situations.

While not all DSCR Lenders will offer rate locks (or really, locks to “rate sheets”), there are enough DSCR Lenders out there, or mortgage brokers with access to enough lenders, that with some minor shopping around and research, finding good DSCR Loan terms for your scenario with a lender that locks is very likely. What is harder, and far more important, is not just locking in your DSCR Loan, but fully understanding all of the terms of the rate lock and how the process works. This means understanding how or if the interest rate will change if final underwriting metrics change, such as if the appraised value comes in low resulting in a new LTV or if the DSCR ratio dips a couple of points due to higher than expected expenses or a lower than expected market rate. Also, it’s crucial to understand what flexibility is allowed, such as if the prepayment penalty provision can be changed or a switch to a Partial-IO structure is allowed, and critically, if done, what effect would that have on interest rate, points or other loan terms.

Additionally, it’s absolutely crucial to understand the lock term as well, including how long the lock is valid for (many DSCR Lenders offer different lock periods such as 30 days, 45 days and 60 days) and if different periods mean different fees. Also, it’s imperative to make sure you understand any “lock extension” fees that might be applied, such as how much it will cost if you need to extend the lock period by 15 days, for example. Even understanding the nuance of how the lock period is calculated is important, i.e. is it from the day of application to the day of close or something different, such as whatever day you want to secure the lock, or if the lock period is based on a “clear to close” declaration, rather than the pure closing date.

While this doesn’t solve this obstacle in every instance – locks may not be offered with your preferred DSCR Lender, or a lock period may expire because of items outside your control – having a full understanding of all of the details of the lock process goes a long way in avoiding getting blindsided by a higher rate and fee than you bargained for at the end of the DSCR Loan process. Bonus points for having “plan Bs” in hand can make all the difference when the rate sheet is locked, like knowing exactly how the pricing will adjust if needing to “buy down the rate” or switch to a Partial-IO structure to fix a low DSCR ratio.

While there are multiple issues that the rate locking system for DSCR Loans can create, one of the best tactics to avoid this obstacle, and most obstacles in general, is to be very proactive and provide any “needs list” items as quickly as possible. This has many benefits and no downsides. For “unlocked” DSCR Loans, moving as quickly as possible means the lowest interest rate risk, i.e. the lower risk market rates move up in between the initial term sheet and the finalized loan terms, simply because there are fewer days in between, and thus fewer days in which market rates can move. For “locked” DSCR Loans, moving quickly helps avoid costly rate lock extension fees. Proactive responsiveness and providing documents can also help prioritize your loan file with the DSCR Lender’s underwriting team, as lenders typically move more quickly on files that are complete and have responsive and helpful borrowers. While not a cure-all, minimizing any borrower-caused delays can help avoid a lot of negative situations with rate lock and rate movement.

The third tactic in this situation is arguably the most powerful, and makes being a well-informed borrower very worthwhile. It comes from not just an understanding of the complicated nuances of DSCR Loan locking, but also an understanding of the economics of a DSCR Lender, and how they make money and operate their business. The key concept to internalize is that DSCR Lenders make their money on closing loans not by denying or losing deals. While there may be some non-refundable fees collected by some, these amounts are a miniscule part of their total revenue. Indeed, when a DSCR Loan dies late in the process, most DSCR Lenders, even those that may have collected a processing fee or deposit up front, will likely lose money on the lost transaction, since they are in most instances on the hook for title costs, appraisal reviews and credit reports and other items. The vast majority of DSCR Lenders rely on making thin margins on closed loans through a combination of upfront closing fee and selling the loan for a premium on the secondary market, typically aiming for these two income sources to net to between 2 to 3 percent gross margin.

When faced with a situation where there is a negative rate move or additional fees required (whether to “buy down” rate or as lock extension fees), negotiating with the DSCR Lender is possible. This is because they are likely facing a situation where the bought down rate or extra fees are necessary for them to hit their needed “pricing hurdle,” such as 2.5%. or else they make nothing (or probably lose money on “eaten” deal costs) if the DSCR Loan dies before closing. Knowing this, a smart borrower can likely negotiate with the DSCR Lender, who might be willing to waive the fees or rate increase to a point where they might still make a 1.25% gross profit on the loan, not up to their typical margin requirements of 2.5%, but obviously better than zero!

The likelihood of success of this tactic depends on many factors, as some DSCR Lenders may have strict policies against negotiating in these scenarios, while others will only entertain it in certain scenarios. However, this is where knowledge and preparation come into play but also borrower behavior: it is much more likely for a DSCR Lender to offer these pricing concessions to borrowers that have been respectful and communicative throughout the process, and who can point to delays “not being their fault,” i.e. they were extremely prompt with the needs list items. A DSCR Lender is far more likely to waive a lock extension fee if the delays were not caused by the borrower. For example, if the borrower delivered all the needs list items neatly within a week, and the delay was caused by their own underwriting team being backed up on file reviews, or the appraiser not being available. This can be a powerful tool for negotiation. Knowledge matters, but being a model borrower to the point of the ask is key.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.