.png)

In the elevated interest rate environment of recent years, DSCR ratios are often razor-thin. Many deals hover right at or just above key thresholds like 1.00x, 1.10x, or 1.15x, meaning even small deviations from initial estimates can wreak havoc on pricing, terms or even eligibility. A DSCR Loan that seemed to fit perfectly at application can suddenly require restructuring once final numbers are in. The DSCR ratio can move down in multiple ways late in the process, including on the revenue side, the numerator in the equation, or the expense side, the denominator in the equation, and within expenses, from the final property tax numbers, insurance numbers or even HOA dues.

On the revenue side, even though the rise of short term rentals have made them a significant portion of properties securing DSCR Loans, a sizable majority of DSCR Loans are still the classic “long-term single family rental,” or a single family residence rented out, or planned to be, to one tenant. Most DSCR Loan acquisitions involve the buyer, or the borrower on the transaction, purchasing a property that is unleased, either fully vacant or with the previous occupant moving out with the sale. In these situations, when the plan is not for STR usage, the rental revenue number, or the numerator in the DSCR ratio used by the DSCR Lender, is going to be the “market rent” as determined by the appraiser. While there are varying sources available to estimate this number, many times investors are optimistic and appraisers are more conservative, resulting in an appraised market rent lower than expected, and thus a final DSCR ratio lower than what was planned for.

The same thing can happen on the expense side, or the denominator in the DSCR ratio formula. While listings and many easily accessible online sources like Zillow contain estimated property taxes, insurance and HOA dues for properties, these are almost always estimates and can be lower than the final, confirmed and underwritten version used by the DSCR Lender. Furthermore, listing agents have an incentive to list properties optimistically to attract buyers, and since these figures are estimates, have been known to understate some of these projected expenses, either through shady salesmanship or even just error. In these cases, an even slightly higher than estimated figure in one of the expense figures in PITIA can push a DSCR ratio down, resulting in an unaffordable set of new loan terms (i.e. much higher rate or leverage cut) or even ineligibility at previously hoped for balances.

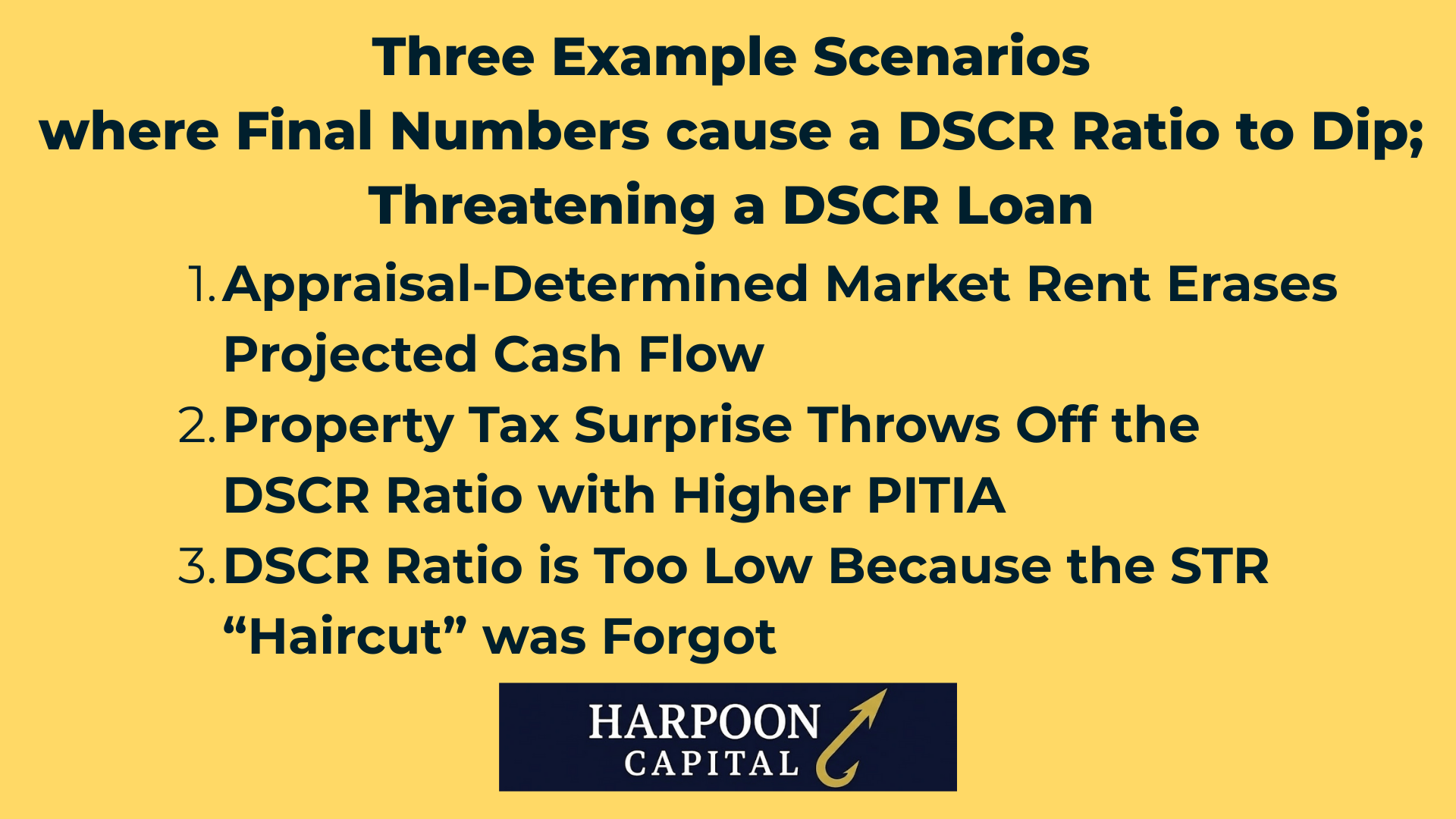

While this obstacle contains changes that almost certainly can’t be “rebutted” or “fixed” like through a reconsideration of value request or deferred maintenance fix, there are typically lots of options available when faced with a DSCR ratio change and needed adjustment. The below will cover three typical examples of when a DSCR ratio is thrown out of whack as well as three tactics DSCR Loan borrowers can use to solve the issue and get to close.

An experienced investor in single family rentals goes under contract for a vacant SFR in a new market, with online tools such as “rentometer” projecting market rents of $4,000 per month due to the location in a great school zone and a bedroom count of four, perfect for renting families. Their strategy is to focus more on appreciation than cash flow, with an investment thesis that large single family residences in good neighborhoods will rise in value over time, no matter the geographic region. By banking on this appreciation focus, the investor is comfortable with a high LTV (80.0%) and minimal down payment, and the estimated DSCR ratio of just 1.05x is okay with this investor, as essentially breaking even while building equity is the plan. However, the appraisal comes back with the 1007 market rent schedule showing a market rent of just $3,500 instead of the planned for $4,000. When substituting this new market rent number into the DSCR formula, the ratio drops below 1.00x, making the DSCR Loan now ineligible at this leverage point (80.0% LTV).

A homeowner and real estate investing novice has been interested in diving into the real estate investing game, and when one of his neighbors puts their property on the market, he decides to make an offer and make it his first rental property. He knows the area intimately, has good connections with local real estate agents and handymen, and this appears to be a perfect opportunity. While the projected DSCR ratio is relatively low at 1.02x, he has watched his own home appreciate significantly in recent years, and believes the neighborhood will continue to produce appreciation, this new property included. However, when the final numbers come in for the DSCR ratio, the property tax number is way higher than expected, as he didn’t account for the loss of the homeowner’s exception on the property that his neighbor enjoyed but he wouldn’t as an investor. This pushes the DSCR ratio down to 0.98x, and losing money every month on a first rental casts doubt about whether the deal will work.

A real estate investor with an expertise in short term rentals spots a new property available in her favored market, knowing that the specific location near one of the area’s most popular beaches and a layout perfect for large groups and families should thrive as an STR. She goes under contract to purchase the property to add to her portfolio, checking AirDNA quickly to evaluate her estimates. While she thinks, based on her local market knowledge, and her expertise and systems in place that she will easily outperform the median “Rentalizer” projections, the conservative AirDNA estimates still show a solid DSCR ratio of 1.11x, enough to qualify at just 25% down. However, once the final numbers come in, her DSCR Lender informs her that they can utilize AirDNA, but must use a 20% “haircut” reducing the projected revenue, which pushes her DSCR ratio into a lower “pricing bucket,” which then requires a higher interest rate, which when applied, increases the PITIA through a higher debt service, which pushes the DSCR ratio down further, the dreaded “DSCR death spiral.” Forgetting that the AirDNA projections would be reduced by a “haircut” threatens to undo the entire deal.

This obstacle, while disruptive, is usually the most fixable of the big DSCR Loan challenges. The key is to know which levers can be pulled, and to prepare for them in advance during quoting and application, so that if your DSCR ratio dips after the appraisal or updated PITIA projections, you and your lender can pivot quickly.

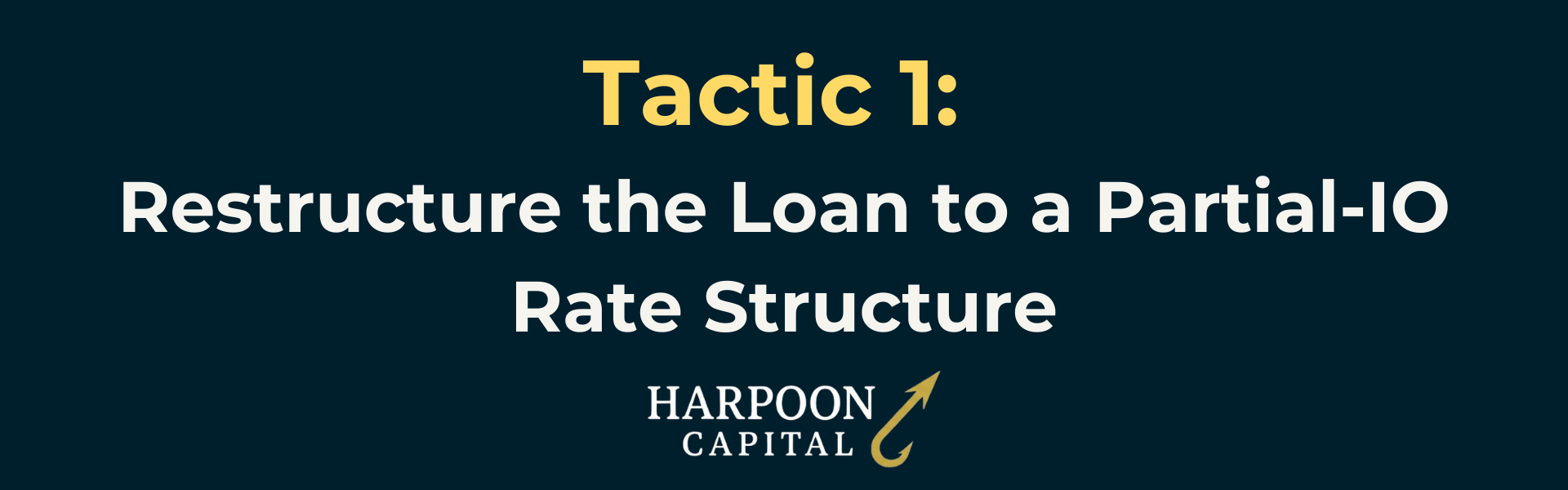

One of the first things to look at in situations where something has to be done to boost a DSCR ratio back to an eligible or needed tier is to explore if the option exists to switch to a Partial-IO option. While moving from a Fully Amortizing structure to Partial-IO often means a bit higher interest rate, the resulting monthly PITIA payment (when eliminating the “P” – principal) actually usually goes down significantly, improving the DSCR ratio (DSCR Lenders use the initial interest-only payment when calculating the DSCR ratio used to qualify).

Changing from Fully Amortizing to a Partial-IO structure should be the first step to consider for solving a DSCR ratio issue, as it can have a significant effect, especially with smaller loan amounts. It’s also relatively easy to calculate and compare, as the math to determine the new debt service payment that will be used for DSCR ratio qualifying will be simple: interest rate times loan amount.

Another area where DSCR Loans’ flexibility shines is when dealing with this obstacle is the relative ease (and borrower optionality) to toggle the tradeoff of interest rates and closing fees. Most borrowers should always have the option to lower the interest rate on their DSCR Loan by “buying it down,” i.e. paying more fees upfront for a lower interest rate. And the good news is that this can be done throughout the loan process, including after an appraisal or other document lowers the DSCR ratio, even if the rate is “locked” early on! This is because the DSCR Loan rate “lock” doesn’t really lock in an untouchable interest rate number, but locks a rate “sheet,” so the flexibility to buy down the rate late in the process typically will still be available, and the borrower won’t stand to lose the benefit of the lock if market interest rates had risen in the meantime either.

The flexibility to “buy down” an interest rate can solve a DSCR ratio issue many times, as the debt service payment is typically a big portion of the PITIA. While paying a couple more points upfront isn’t ideal for many borrowers, it will have the double benefits of fixing a DSCR ratio that dipped too low for qualification and will lower the monthly payment over the course of the loan.

While DSCR Loans have a higher likelihood of changes in qualification and eligibility late in the process than conventional loans, (since the appraisal affects qualification so much, versus qualification mostly known upfront for DTI-based mortgage loans), the added flexibility to tweak terms offsets this potential DSCR Loan downside. DSCR ratios that move slightly below eligibility tiers, like moving from 1.05x to 0.98x, and needing 1.00x to qualify, can be fixed in a lot of different ways, and often with small tweaks. For example, while the interest rate benefits for utilizing a Hybrid (Fixed to ARM) option rather than fixed rate are typically small, if the DSCR ratio only needs to be moved up slightly to qualify, like from 0.98x to 1.00x, this structure fix can make that crucially needed 0.02 difference.

Additionally, while most borrowers determine loan amounts by choosing the loan amount that correlates with the highest LTV available in a given LTV “bucket,” i.e. borrowing at 75.0% LTV when in the 70.1-75.0% LTV bucket, and at 70.0% LTV if in the 65.1-70.0% LTV bucket, it’s not necessary. While not ideal, if for example you start with an 80.0% LTV, but reducing the loan amount by a couple thousand dollars would result in a 79.2% LTV, it would fix the DSCR ratio issue. That would be an option. DSCR Lenders should always be amenable to tailored and non-standard loan amounts, and the corresponding LTVs needed to solve for a DSCR ratio of 1.00x.

Depending on the flexibility of the particular DSCR Lender, these small tweaks can also be done in terms of interest rates and buydowns. Some lenders might allow buy downs not just in one percent (i.e. “one point”) increments, offering carefully minimized adjustments, like paying an extra 0.3% in fee to get the exact minimum DSCR ratio needed. One of the great benefits of DSCR Loans is the ability to pull multiple levers to get deals to work, and there should be many options (used individually or in conjunction) to fix a DSCR ratio issue. Keeping these levers in your back pocket when running the initial numbers can be a great “Plan B” for if the DSCR ratio needs a slight boost late in the process.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.