.png)

The vast majority of DSCR Loans are not held by your DSCR Lender; they are typically sold within weeks of the closing date in what’s called the “secondary market” to other companies that “securitize” the loans into mortgage-backed-securities (“MBS”) or bonds (this is why the loan “servicer” that collects your payments will typically change in the initial months following the loan closing). These bonds are investment securities that pay investors interest and are a common feature of investment portfolios across the spectrum – held by banks and financial institutions, pension funds, insurance companies, 401(k)s and retirement accounts and even found among hedge funds and in personal brokerage accounts. While the specific mechanics of these securitizations are beyond the scope of this guide, what is important for real estate investors and DSCR Loan borrowers to understand is that their DSCR Loans end up as part of the bond market, meaning they are held by bond investors, and influenced and tied to other bonds and the greater “fixed income” world.

Q: What is the secondary market for mortgage loans?

A: The secondary market is where most lenders sell the mortgages they originate rather than holding them long-term. DSCR Lenders in particular almost always sell their loans to institutional investors, who package them into securities or place them in investment portfolios. This is why it’s common for borrowers to see their lender or loan servicer change in the months after closing as the loan has been sold, but the terms remain the same.

Why is this important? Because DSCR Loans are a part of the bond market as a whole, they are one of many options for investors looking for yield, including large financial institutions like insurance companies or small individual brokerage accounts. DSCR Loans become one option, among many, including other mortgage-backed security bonds made up of conventional loans (often referred to as “Agency MBS”) or bonds issued by the Federal Government of the United States (“Treasury Bonds”). As such, when bond investors evaluate their options, they are evaluating buying MBS strictly made up of DSCR Loans only or MBS made up of all sorts of Non-QM Loans (including DSCR Loans) against many other alternatives including US Treasuries or conventional Agency MBS.

Bond investors, or “Secondary Market Investors,” will evaluate all these options through the lens of risk and reward, and invest accordingly. Many chartered banks hold MBS as part of their portfolios, and these banks have access to earning returns through interbank lending and earning interest on their balances held at the Federal Reserve. When you hear the Federal Reserve “setting interest rates,” this refers to the “effective federal funds rate” or what banks earn from lending to other chartered banks. These banks are required to hold reserves at the Federal Reserve if they are chartered as a national bank, and they earn interest on these holdings too – paid based on the Interest Rate on Reserve Balances or “IORB Rate.” While these interest rates aren’t directly connected to interest rates earned from Treasury bonds or MBS, they are another main alternative for institutional investors (i.e. banks)that affect mortgage rates.

Q: Does the Federal Reserve set mortgage rates?

A: Not directly, but they play a big role. The Fed sets the federal funds rate, which is what banks pay to borrow from the Fed and each other. Mortgage rates are primarily determined by investors buying mortgage-backed securities (MBS) and are influenced by alternatives like U.S. Treasuries. As a result, Fed policy affects mortgage rates indirectly and significantly, since investors in mortgage bonds demand a certain amount “spread” above key benchmarks, like the federal funds rate.

Remember, risk is not necessarily a “good” or “bad” thing, it must always be considered in investing in conjunction with its ‘partner in crime’: reward. For instance, earning a 10% return might be a fair trade-off if you’re buying a Class A single-family rental in a top-tier market with a reliable A+ tenant. But that same “reward” doesn’t look so appealing if it requires betting on a #16 seed making a Cinderella run all the way to the Final Four in March Madness. Bonds work the same way: all things equal, an investor would rather have a bond with the borrower being the full faith and credit of the United States Government than the credit profile of a typical DSCR borrower (no offense to financially responsible investors, but even the best borrowers are not a better bet than Uncle Sam!). However, when you introduce reward to the equation, where the US Government may be paying 3% interest and the DSCR borrower paying 6%, the increased risk of the DSCR MBS might be worth it for the reward; i.e. earning double the interest (6% instead of 3%).

Bond Investors generally consider how much of an interest rate they demand (the “reward” for the “risk” for buying a bond, or the chance that the bond buyer doesn’t get paid back) in relation to what is considered the “risk-free” rate, or yield (i.e. interest paid) by US Treasury Bonds, with the 10-Year US Treasury Bond the most commonly used “risk-free” standard. While the current fiscal trajectory of the country has some issues that make considering US Treasury bonds as “risk-free” a shaky proclamation, it is the current market standard on how rates are set for bonds in the US and likely will be for the considerable future.

A common quip for people piping up about the risks of “risk-free” bonds is that if the United States Federal government defaults on their bonds – investors will have much more to worry about than their coupon payments – the government and financial system itself would have likely collapsed, and would have bigger priorities such as navigating an apocalyptic hellscape rather than maximizing 401(k) payment schedules.

Q: What is the “risk-free” rate for bonds and mortgages?

A: The “risk-free” rate is based on U.S. Treasury yields, most often the 10-Year Treasury, which serves as the benchmark for bond and mortgage pricing. While calling Treasuries “risk-free” is debatable given U.S. fiscal issues, they remain the standard. As investors joke, if the U.S. ever truly defaulted, your bond coupon would be the least of your worries.

The “base stack” or “base interest rates” that make up the macro half of mortgage loan pricing, or interest rate setting, is derived starting from these “risk-free” rates. The “base rates” for mortgage rates (i.e. the interest rate that lenders start with before adjusting based on risk factors or LLPAs – loan level price adjustments) are generally the current risk-free rate plus what is called a “spread” to account for the additional risk for borrowers that are less credit worthy than the US Federal Government. Spreads are larger or smaller based on how much riskier the borrower and type of debt is than the Federal Government Treasury Bonds benchmark, ranging from very small (such as state municipal bonds with high credit ratings) to agency MBS (which have an implicit guarantee from the Federal Government) to non-agency MBS or private corporate bonds, which are higher as they don’t have the credit or implied guarantee by the all-mighty Federal Government. The spread is a measure of the additional “reward” needed for the additional “risk” when buying bonds from riskier borrowers than the United States.

Q: What is a spread in mortgage loans?

A: A spread is the premium above the “risk-free” benchmark, such as U.S. Treasuries, that determines the actual mortgage rate borrowers pay. For real estate investors, this is the gap that turns a 5.0% Treasury yield into a 6.5% mortgage rate, roughly 150 basis points, compensating investors for the additional risk.

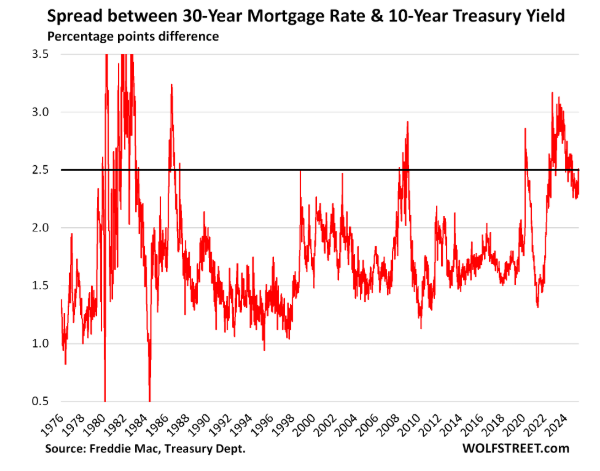

Typically, conventional mortgage loans (i.e. standard residential mortgage loans backed by government-sponsored entities) will have interest rates calculated with base equivalent to the US 10-Year Treasury Bond plus a spread, with conventional rates historically moving in concert with 10-Year Treasury yields. While the spread is not always static – i.e. the difference between the 10-Year Treasury Yield and Conventional Mortgage Rates isn’t always the same exact number, it is usually around 100 to 300 basis points, or 1% to 3% higher. Spreads generally go higher (i.e. “widen” in financial lingo) when there are higher overall economic and market risks – i.e. concerns about rising unemployment, stalling growth or other negative economic indicators since this increases the “risk” of mortgage bonds, which are tied to the housing market which itself is tied to the economy in general.

These changes in overall economic and market risks only affect the “spread” side of the equation, as the “risk-free” rate remains the same (i.e. risk can’t change on something considered immune to risk itself). The opposite effect is typically referred to as spreads “tightening,” which occurs when overall market economics improve, i.e. indications of increased growth, lower inflation or a better job market. When this happens, spreads go lower, as mortgage rates get closer to the risk-free rate.

Q: What is spread widening and spread tightening in mortgage loans?

A: Spread widening is when the gap between Treasury yields and mortgage rates increases, usually because investors see greater risk in the broader economy and demand higher returns. Spread tightening is the opposite: the gap narrows when conditions improve and risk premiums fall. For real estate investors, widening means higher mortgage rates, while tightening lowers them.

One interesting insight for real estate investors using DSCR Loans is that the benchmark for DSCR Loans and other “non-QM” loans in general is the US 5-Year Treasury Yield instead of the US 10-Year Treasury Yield. While this doesn’t make too much of a difference (10-year treasuries and 5-year treasuries generally have similar yields), it’s important nonetheless to truly track and understand current DSCR Loan interest rates. The reason is likely related to the fact that non-QM loans (including DSCR Loans) typically have a lower average duration (i.e. amount of time before the loan is paid off or refinanced). The vast majority of all mortgage loans won’t be outstanding – or have a duration for – the entire 30-year term.

A leading reason why non-QM Loans (including DSCR Loans) likely have shorter duration than conventional loans, and thus have rates tied more closely to the 5-Year Treasury Yield instead of the 10-Year Treasury Yield is that many non-QM borrowers are likely to refinance into conventional loans if and when they qualify to access the better rates, while conventional loan borrowers obviously already have the low conventional rates, and thus don’t have this accelerated refinance incentive.

The spreads between DSCR Loans and the 5-Year Treasury yields do not have as much of a long history as conventional mortgages (considering DSCR Loans have only been around in a material volume since around 2018), however they generally sit around the 300 bps range. As such, the “base stack” on DSCR lender rate sheets and pricing tools will typically correspond to whatever the current 5-Year Treasury Yield is plus 3% or 300 basis points or so.

An investor that has read this far knows there’s no simple answer to “What are the current DSCR loan interest rates?” as interest rates are based on several constantly changing things: spreads, Treasury yields and of course lots of loan-level loan-specific adjustments that are unique to each loan. However, a good “rule of thumb” around determining current DSCR rates is to look up the current 5-Year Treasury Yield and add 3%. That resulting number would generally give you a good idea of what a “generic” or vanilla DSCR Loan rate would be on a basic typical loan – like a 25% down acquisition of a rental property with a 1.10x DSCR ratio, solid qualifying credit (i.e. 740) and fairly standard loan terms. Note that this is similar to how “current mortgage loan rates” are generally reported in headlines and websites like Mortgage News Daily, which estimates a “standard going rate,” which generally refers to owner-occupied conventional mortgage loans with the standard 20% down and good credit and DTI.

Up Next: What Determines Mortgage Rates, including DSCR Loan Rates? Yes, It’s Mostly the Fed

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.