.png)

The appraisal is the cornerstone of DSCR Loan underwriting. It’s the independent, professional opinion of the property’s current market value, and in DSCR lending, in contrast to DTI-based alternatives (conventional or other non-QM loans), includes a critical estimate of market rent as well. The market value and market rent estimates determined by the third-party appraisal are critical to the all-important LTV and DSCR ratio metrics that play an outsized role in qualification, eligibility and pricing of DSCR Loans. In addition, the appraisal’s determination of market classifications (i.e. if rural, declining) or condition (if it has significant repairs needed) can also be critical factors for eligibility and price (rate and fees). For these reasons, the appraisal’s results are often a moment of truth in DSCR lending, a document that can make or break the loan in many ways. As such, it’s critical for the well-informed DSCR borrower to understand how these appraisals work and how to be best prepared for how to deal with and potentially adjust and pivot to the findings in the appraisal report.

While the borrower does not “shop” for the appraiser (and cannot legally influence their opinion), you will almost always be responsible for paying for the appraisal and coordinating access to the property. For investors, that means working with tenants, property managers or sellers to ensure the appraiser can enter on the scheduled date.

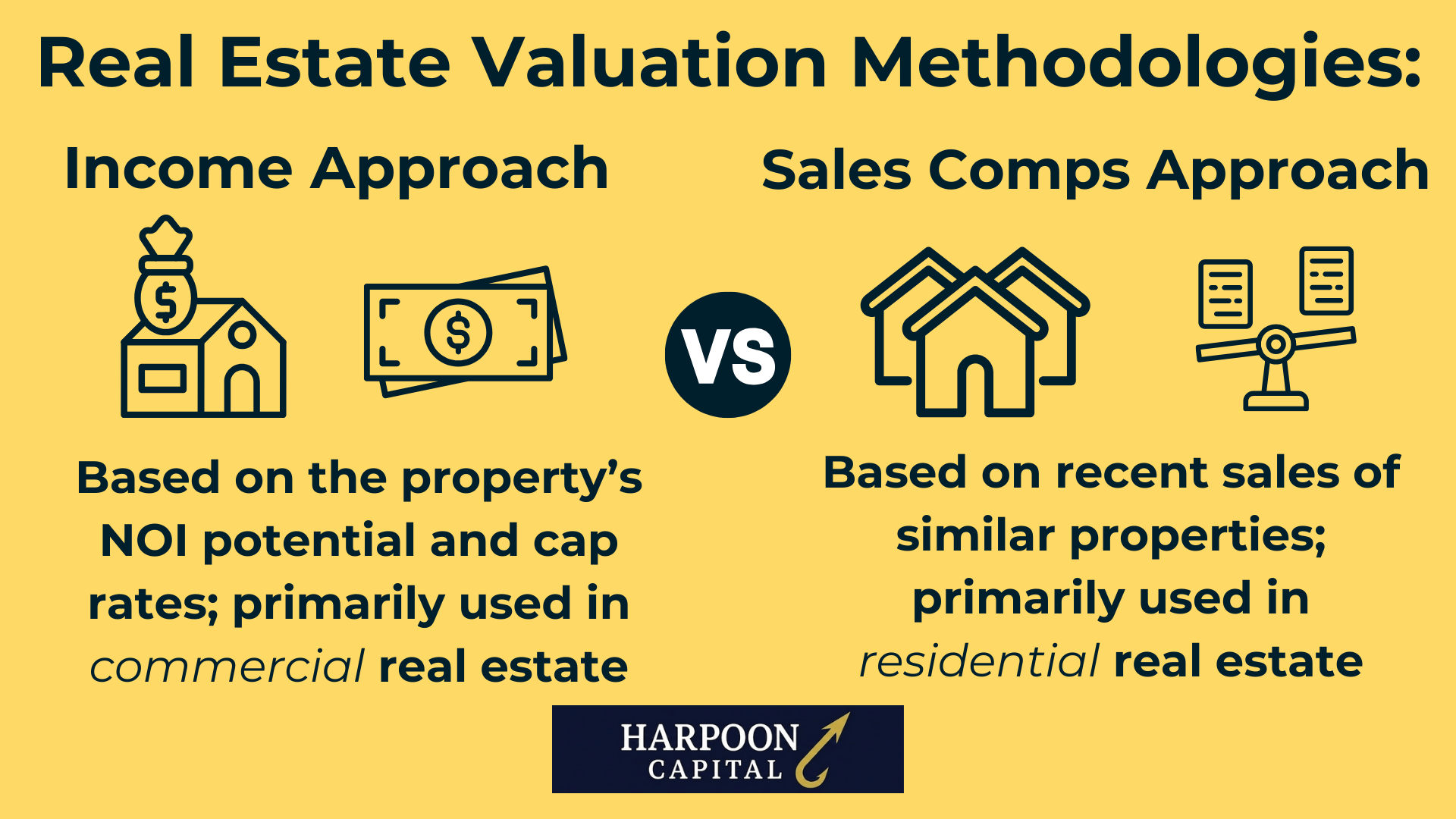

When a DSCR Lender orders an appraisal, they’re typically ordering the same type of standard residential appraisal that would be used for a conventional mortgage or an owner-occupied single-family home. The appraiser’s job in both cases is to produce a credible and well-supported opinion of market value for the property as of a specific date. The foundation of almost all residential appraisals is the sales comparison approach; a valuation method built on the principle that a property’s value is best indicated by recent sales of similar properties in the same market.

Note that this is the approach for residential real estate appraisals which are utilized by lenders for loans secured by properties between one and four units, regardless of whether they are being used for owner-occupancy or rental purposes. Investors experienced or more familiar with larger multi-unit residential properties or commercial real estate sometimes get confused with this valuation approach for residential rental properties since larger or commercial real estate have market values primarily derived from the income capitalization approach. This is a different valuation method that’s based on the income generated by the property (rents and net operating income) and the property’s profitability versus other similar property’s risks and earning potential in similar markets (through using capitalization rates). While these valuation analyses (appraisals for larger multifamily properties or commercial real estate) also can include sales comparable approaches, the driving valuation mechanism is much different.

This difference again is rooted in market value, i.e. how much the market will bear for a given real estate asset is willing to pay for the property. While DSCR Loans are made strictly for rental properties only, the market for such properties - residential real estate with four units or fewer - is still overwhelmingly dominated by owner-occupant users. Thus, market values are going to be primarily determined by this market, and as such, market value will be based on sales comparables since vast majority of the “market” for residential real estate are potential owner occupants that will determine how much they are willing to pay for a property based on factors such as how much they like living in the property and personal tastes, and they have no care or interest in “how much it would rent for.”

And since they have no intention or desire to earn income at the property – they just want to live there - then the income approach or earning potential won’t be and shouldn’t be a major factor in valuation. Thus, capitalization rates are not a factor for residential real estate rental properties and valuations are not based on NOI or the income approach.

In contrast, since the “market” of buyers for multifamily properties with five or more units or commercial real estate is pretty much 100% investors, who care overwhelmingly about return on investments and net operating income, the valuation of these assets – market value – will be based on that. Additionally, even properties that are short term rentals and operate as true businesses generating income (and even attract and are marketed to buyers looking for turnkey operating airbnbs) must still be valued with a residential appraisal based on the sales comparison approach, because the market for these properties, even if the properties are best used as STRS, is still likely going to be mostly potential owner-occupants.

Most real estate investors utilizing DSCR Loans should thus be most familiar with the sales comparison approach to value of residential properties, since this is the method that appraisers will be utilizing in valuing their properties (outside of the small subset of situations involving Multifamily DSCR Loans or Mixed Use DSCR Loans). The sales comparison approach is a method built on the principle that a property’s value is best indicated by recent sales of similar properties in the same market.

The process starts with an inspection where the appraiser visits the property, inside and out, to document size, layout, quality, condition, site features and any unique attributes. Following the in-person inspection, the appraiser will then make a selection of comparable sales (“comps”). These are properties similar in size, style, and utility, ideally located nearby that have sold recently in arm’s-length transactions. Then, the appraiser will make adjustments for differences, such as if a comp is superior in a feature (e.g., has a pool), the appraiser will subtract value from that comp to “equalize” it to the subject property; if inferior (e.g., smaller lot), the appraiser adds value to it. Finally, the appraiser will perform a reconciliation, where they weigh the adjusted sale prices of the best comps and reconciles them into a single, supported opinion of market value.

While appraisers have professional discretion, there are general standards and methodologies for selecting comps. Most important is distance to the subject property, as comparable properties should generally be within one to three miles in urban/suburban areas while in rural markets, up to five miles may be accepted. Typically, anytime a comparable property is over five miles from the subject property, flags will be raised by a DSCR Lender. Next is similarity, as the top three comparable properties should be close enough in features that net adjustments (adds/subtracts) do not exceed 20% of the comp’s sale price. When a net adjustment for property differences is over 20%, this also raises flags for most DSCR Lenders, as it indicates quite a different property.

Additionally, appraiser comparables are evaluated for Recency, with comps ideally sold within the last six months. If the sale was more than 12 months earlier, this will also typically be flagged, since market conditions and prices are often stale when comparing to a year or more ago. The Number of Comps is also important. While the main valuation analysis emphasizes the top 3 comps (most similar and weighted most heavily), additional comps (up to 6 total) are often included to provide context or show market trends, even if less similar. Generally, the more relevant and similar comparables, the better, because they can give a more accurate valuation picture.

When appraisers are performing the sales comparables approach to determine a property’s market value, each of the comparable properties will be different and never a perfect twin to the subject property. Determining an accurate value requires making several “adjustments” to the prices of the comparable properties. There are different labels for these adjustments that can sometimes leave investors confused. Key to truly understanding the appraisal methodology is understanding the differences between Gross Adjustments and Net Adjustments.

Gross Adjustments are the sum of all absolute value changes to a comp, ignoring whether they’re positive or negative. Then, the Net Adjustment is a sum of all adjustments after accounting for direction (positive or negative). While most DSCR Lenders require (or strongly prefer) net adjustments to not exceed 20%, many also have limits on gross adjustments as well. Even if a net adjustment is low, a comparable property that has significant gross adjustments in both directions that happen to “net out” to a low total number can be problematic too; as this arguably indicates that the low net adjustment was a fluke and the comparable property is not like the subject property at all! For that reason, most DSCR Lenders will also not want to see total gross adjustments to exceed 25-30% as well.

Here’s an illustrative example of how the adjustment process might work in an appraisal utilizing the sales comparison approach for a property secured by a DSCR Loan:

Look at the below table for how an appraiser may adjust a similar property that was sold for a price of $1,875,000 four months prior to the subject property:

When all adjustments are totaled, the Net Adjustment equals –$23,850 (1.3% of the sale price) and the Gross Adjustments total $163,950, or about 8.7% of the sale price.

This results in an Adjusted Sale Price of $1,851,150, which is used as an estimate for the subject property’s value, along with the adjusted sales price of the other (at least two) comparable properties. Note that this adjusted sale price, or value, is slightly less than the comparable property, primarily due to the subject property not having a pool and a smaller garage, partially offset by the subject property’s brand-new status and large square footage. Also note that since this comparable was sold relatively recently (within the last four months) and is close by (around a mile away), it shows all the hallmarks of a solid comparable for the subject property in this example.

While this example is illustrative, there is tremendous variation among residential real estate properties and markets in the United States that can secure DSCR Loans. As such, the types of items and number of adjustments can differ significantly, especially based on market. For example, while a pool might be of great importance in sunny climates like Florida and Texas and have a large impact on valuation (like in our example), that same factor might not be nearly as impactful in a northern climate like New England. Additionally, distance factors can vary in importance as well; a few miles in an otherwise cookie cutter suburb might not matter much at all, whereas half a mile, separating true “beachfront” from an arduous path to the shoreline can result in significantly different values in some beach markets.

Even condo units with the exact same size and exact same layout – two twin units – in the same building can have vastly different value adjustments based on view, including how high up the unit is or even just which side of the building it’s on. For these reasons, appraiser’s adjustments are far more art than science. That being said, there are somewhat predictable guardrails and methodologies and “typical adjustments” and treatments most investors can come to expect (and smart investors know the quirks and unique factors of the markets that they invest in anyway), and some are outlined in the table below.

For DSCR Loans, the appraisal not only provides a “market value” but also a “market rent,” which is often utilized when evaluating and underwriting the expected revenue (i.e. the numerator in the DSCR) for the property. To get that number, the lender requires the appraiser to complete a Fannie Mae Form 1007 Comparable Rent Schedule alongside the main appraisal. The methodology here mirrors the sales comparison approach, except instead of evaluating sale prices of comparable properties, the appraiser is evaluating the rental rates for comparable properties. Note that the Form is the “1025” for 2-4 unit properties, but works the same way, just for multi-unit properties, and the term “1007” is typically used interchangeably to describe this appraisal-determined market rent process.

For determining a market rent for the 1007 report, the appraiser follows a very similar approach to valuation. First, the appraiser will typically list key features of the property relevant to rental value: bedroom/bath count, gross living area (GLA), year built, parking and special amenities. Then, the appraiser will make a selection of comparable rentals. This will also typically include three leased properties that are as similar as possible and located nearby. The appraiser looks for recent leases (within the past 12 months), matching unit type, and comparable size/features. After selecting the comparable leases, the appraiser will make rental adjustments, just like in the sales comparison approach. For example, if a comp rents for $2,100/month but has a garage and the subject doesn’t, the appraiser might subtract $50–$100 from that comp’s rent to make it “equal” to the subject.

After adjustments, the appraiser arrives at a single monthly “Opinion of Market Rent” for the subject property. The appraiser will then sign the 1007 as part of the overall appraisal, confirming the data sources and adjustments, with the 1007 typically not a separate document from the appraisal, but rather included as all-in-one.

%20Market%20Rents.png)

Traditionally, the Form 1007 (or 1025 for 2–4 unit properties) is designed to report long-term market rents, with “long-term” defined typically as rents for 12-month leases. In most cases, appraisers complete the 1007 by surveying comparable long-term rentals, even if the subject property operates or is intended to operate as a short-term rental.

Historically, a minority of DSCR Lenders have allowed appraisers to prepare a 1007 using STR-based market rents. When they do, it is almost always limited to true vacation rental markets where year-round long-term rental comparables simply do not exist, and where the local market is dominated by short-term rentals. These are markets such as Outer Banks, North Carolina; Ocean City, Maryland and Block Island, Rhode Island. By contrast, in metro markets like Austin, Texas or Scottsdale, Arizona, where STRs are common but there is also a robust year-round long-term rental market — appraisers are typically still required to base the 1007 on long-term rents, not STR figures.

Another important note is that in June 2024, Fannie Mae issued guidance stating that the “1007 was not designed for appraising single-family properties that are used as STRs,” which caused several DSCR Lenders to begin moving away from the practice. Even though DSCR Lenders are private lenders not beholden to Fannie Mae guidelines, many times they will follow guidance and trends emanating from conventional lenders, and this announcement spurred more lenders away from instructing appraisers to utilize the 1007 form in this fashion.

STR-based 1007s started to significantly fall out of fashion in the early 2020s as more and more DSCR Lenders began to trust AirDNA and integrate it into their underwriting (i.e. utilize AirDNA projections directly for the rental revenue number when calculating DSCR). The 1007 form is still a conventional form and has remained designed for long-term rental comparisons, not short-term rentals, and many appraisers either struggled to complete them based on short-term rents or refused to do so entirely.

However, AirDNA wasn’t always a perfect solution, and doesn’t work as a substitute for an appraiser’s market rent in every scenario. AirDNA uses a high-level data-driven technological algorithm, and part of the reasons it’s trusted by so many DSCR Lenders is that it provides neutral data-based analysis and projections, free from human bias or thumbs on the scale. The flip side of this strength however is the cases where human judgment is needed, instances where appraisers can make a better judgment. Properties that are primed for STR success may have nuanced details, like a specific location or particular amenity that isn’t picked up on by the AirDNA algorithms. In these cases, the appraiser’s judgment can be superior, and a detailed human analysis, taking into account special factors is key to accurate STR projections. Something that drives a lot of real estate investing success and separates real estate investing from other areas of finance is the ability to spot things in “real” life that don’t show up on screens.

In response, in mid-2025, some DSCR Lenders worked to develop a new solution for these cases, adding what is called a “Narrative Short Term Rental Rent Analysis” section to appraisals for DSCR Loans on intended short term rentals to replace a 1007 form, STR-based or not. This analysis requires the licensed appraiser to evaluate the property’s Local STR Market Trends, commenting on current STR market conditions and including any factors driving rental demand, such as proximity to tourist attractions, corporate hubs or seasonal events. It also requires the appraiser to comment on Regulatory Risks and identify any potential risk affecting the property’s legal or zoning ability to operate as an STR. For refinances or properties already in use as an STR, it also asks the appraiser to comment on any Historical STR Data and utilize that recent performance history.

In addition to these analytical factors, the appraiser then selects three comparable STR properties that “closely match the subject property in size, location, utility, appeal and condition. The appraiser then analyzes the comparable properties’ Gross Rate and Occupancy Percentage in “peak season,” “shoulder season” and “off-season” and the month range or number of days expected in each. From there the appraiser calculates an Estimated Gross Annual Nightly Rate (GANR) and an Estimated Annual Occupancy Days, or number of days per year it would be expected to be occupied as an STR. Then, by multiplying those two figures together (GANR * Estimated Occupied Days), finally arrives at the Estimated Gross Monthly Income, which would then be multiplied by 12 to reach the estimated annual short-term rents.

This form and methodology for short term rentals and DSCR Loan appraisals is still extremely new, but looks promising, and will likely increase in use among DSCR Lenders, especially those more open to STRs and change in general.

While the 1007 is the defining DSCR-specific addition for 1–4 unit rentals, other appraisal forms come into play based on property type. The Form 1025, or “Small Residential Income Property Appraisal Report” is used for 2–4 unit properties. It incorporates both the property valuation and a built-in income approach showing gross rent, expenses, and net operating income for all units. The Form 1073, or “Individual Condominium Unit Appraisal Report” is used for condos. It is similar to the standard single-family report but adds condo-specific data like HOA dues, amenities, building size, and owner-occupancy rates. All in all, these different appraisal forms and templates don’t differ that much besides name and nuances for the slightly different property type, but they evaluate and determine market value and market rents essentially the same way.

.png)

For DSCR Loans, the process for selecting, assigning, and delivering that appraisal must be independent from influence by all the interested parties in the transaction, including both the borrower and the lender. Everyone involved in a real estate transaction, the borrower, the mortgage broker, any real estate agents (including both for the seller and buyer), the loan officer, even the seller, benefits if the property appraises at the highest possible value and rent levels.

Since the DSCR Lender relies on an accurate value, as they are the ones lending money and relying on the property – and its value – to cover the debt if things go wrong (i.e. through foreclosure), many might assume then that there is no incentive for the lender for any over-valuation or overstatement of rents. However, the vast majority of DSCR Loans are sold to institutional investors such as pension funds or insurance companies, i.e. “Note Holders,” either directly or through securitized mortgage-backed securities (MBS) transactions. These note holders then own the loans for almost their entire lives, and they are the party that holds the risk and recourse that is dependent on accurate valuations. As such, actual DSCR Lenders, who make their money overwhelmingly from upfront fees and quick loan sales (via premiums), are actually greatly incentivized to close loans and “get deals done” as much as, if not more so, than any other party. And in particular, loan officers or Account Executives, i.e. the sales staff for DSCR Lenders, who typically make most of their income through commissions, earned only when loans close, are even more incentivized to make sure appraisals, specifically appraisals that come back with lower than expected valuations or market rents, don’t kill their deals – and their paychecks.

Loan Buyers (i.e. eventual Note Holders), well-aware of all this, thus will only buy DSCR Loans from DSCR Lenders that have strict processes in place to prevent undue influence from any party, and particularly DSCR Lenders and their commission-centric sales team, from messing with independent and unbiased valuations. And this is where Appraisal Management Companies (AMCs) and formal Appraisal Independence Requirements (AIR) Policies come into play.

An Appraisal Management Company is a third-party entity that sits between the DSCR Lender and appraisers. Its job is to maintain a panel of licensed and qualified appraisers and assign appraisal orders on a rotational or blind basis to avoid favoritism. They also handle payment, delivery and quality control for appraisal reports and mostly serve as a firewall so that sales staff (or any other interested party) cannot directly influence which appraiser is chosen or how the report is written.

Q: What is an AMC in mortgage lending?

A: An Appraisal Management Company (AMC) is a third-party service that orders, assigns, and delivers appraisals on behalf of a lender. In DSCR loans, AMCs are used to ensure appraiser selection is independent from loan sales staff, reducing bias and protecting the credibility of property valuations.

Q: Why do DSCR Lenders use AMCs instead of picking appraisers directly?

A: DSCR Lenders use AMCs to comply with Appraisal Independence Requirements (AIR), which prohibit commission-based loan officers from influencing who completes the appraisal or how it’s written. This independence is critical because most DSCR Loans are sold to institutional investors, who demand unbiased valuations they can trust.

Additionally, every reputable DSCR lender should have a written Appraisal Independence Requirements (AIR) Policy that prohibits loan officers, account executives, and other commission-based production staff from selecting, contacting, or influencing appraisers and requires all appraisal assignments to go through an AMC or another compliant, centralized ordering process. This policy will also outline procedures for disputing an appraisal (reconsideration of value) without violating independence rules and documents staff training and enforcement measures.

.png)

Q: What are Appraisal Independence Requirements (AIR)?

A: Appraisal Independence Requirements are rules that prevent anyone with a financial interest in a loan’s outcome, like a loan officer or mortgage broker, from influencing the appraiser’s selection, compensation, or valuation. A written AIR policy ensures appraisals are credible, compliant, and accepted by secondary market investors.

Even though the DSCR Lender, through its AMC or centralized ordering process, is the one who selects and assigns the appraiser, there are still important steps borrowers can take to keep the process moving and ensure the appraiser has everything they need to do a thorough, accurate and quick job. First is to pay the appraisal invoice promptly.

Most DSCR Lenders will not release the order to the AMC until the appraisal fee is collected. Some DSCR Lenders will require the appraisal cost to be paid upfront as a separate invoice, while others collect it as part of a broader “deposit” or only order the appraisal after a processing fee is paid. While there may be occasional promotional programs where the lender covers the appraisal cost, these are rare. In most cases, the borrower is responsible for payment and prompt action avoids days of unnecessary delay in the scheduling process.

Additionally, it’s a smart practice for borrowers to coordinate property access early, although the form of this coordination will vary depending on the transaction type, obviously in different forms if an acquisition (i.e. the borrower doesn’t own or control property access yet) and/or tenancy (i.e. if the property is vacant – easiest – or if tenants are in place or it’s actively operating as a short term rental, thus more complicated). Regardless, a quick and responsive plan towards communication with the appraiser and confirming details for the inspection (i.e. lockbox or access codes, alerting tenants, working around STR turnover times, etc.) can be key for a clean and speedy appraisal process. This can be especially important on condo properties, as instances where the information related to the condo project as a whole is inconsistent between what is on the appraisal and what is on the condo questionnaire, causing deal delays and headaches. While not always feasible, it could be best practice to see if the appraiser can have direct access to a representative from the HOA, including on the appraiser site visit. This can reduce discrepancies and delays on these DSCR Loans.

While borrowers can’t influence or “coach” the appraiser toward a target value or market rents, it is totally okay and beneficial to provide factual information that can be useful in the analysis, such as the most recent PSA and any amendments, clear and legible in-place lease documents or STR operating histories or even a list of recent renovations or improvements, like invoices and proof of work statements from contractors or specialists. While cooperation and readiness can’t increase a property’s appraised value beyond what the market supports, it can prevent unnecessary delays, miscommunications or overlooked features that could hold the report back from being as accurate and timely as possible, both typically crucial ingredients to a successful DSCR Loan close.

In some cases, a borrower may already have a recent appraisal from another lender when applying for a DSCR loan. Rather than ordering a brand-new report, many DSCR Lenders will allow what’s called an appraisal transfer, essentially reassigning the original report to the new lender, provided certain conditions are met. While details can vary by lender, industry standard among DSCR Lenders is that appraisal transfers are acceptable if a few key conditions are satisfied. One, the original appraisal must have been ordered through an AMC by a reputable lender. The prior lender can be a DSCR Lender, a conventional mortgage lender or another legitimate mortgage institution, but the key is that the appraisal must have been ordered through an AMC under that lender’s Appraisal Independence Requirements (AIR) Policy.

Second, there typically must be a handful of required transfer documentation that comes with the report, including an Appraisal Transfer Letter, which is a formal letter from the original lender reassigning the appraisal to the new lender’s name as well as an AIR Certification, or a statement verifying that the appraisal was completed in compliance with Appraisal Independence Requirements. Additionally, most DSCR Lenders require what’s called an “XML File,” which is the raw XML version of the appraisal, allowing the new lender to run it through the Uniform Collateral Data Portal (UCDP) in their own name alongside the normal PDF Copy of the full report itself.

Finally, Appraisal Age is a key consideration in appraisal transfers as most DSCR Lenders will require that the appraisal must still meet standard age requirements, typically with an as-is date no greater than 120 days prior to the new closing date. Note that a recertification of value is generally not allowed if the appraisal has expired. In these cases, a new full appraisal, ordered by the new DSCR Lender, will be required.

Additionally, while most DSCR Lenders are open to appraisal transfers that meet the above requirements, some will require a Letter of Explanation (LOE) from the borrower, or at least a short written communication explaining why the original transaction with the prior lender did not close. This step is primarily a fraud-prevention measure, ensuring the prior lender wasn’t declining the deal for an undisclosed reason that would also concern the new lender.

Q: Can I use an appraisal from another lender for my DSCR loan?

A: Often yes, most DSCR Lenders will accept a recent appraisal from another reputable lender if it was ordered through an AMC and meets their compliance rules. You’ll need the appraisal transferred into your new lender’s name, and it must be recent enough to meet standard age limits.

For properties above certain loan amount thresholds (often $2 million, but sometimes $1.5 million for particularly conservative DSCR Lenders), a second full appraisal is ordered. This is industry standard in the non-agency investor loan space and is designed to reduce valuation risk for large dollar, higher-risk transactions.

Both appraisals must be from independent firms, and the DSCR Lender will typically use the lower of the two for LTV calculations. In rare cases of material variance, an appraisal review or tie-breaker opinion may be ordered.

Q: When is a second appraisal required for a DSCR Loan?

A: Most DSCR Lenders require a second full appraisal on high-value properties — typically when the loan amount is above $2 million, or in some cases above $1.5 million. Both reports must come from independent sources (i.e. an AMC), and the lower value of the two used for loan-to-value (LTV) calculations.

In most DSCR Loan programs, an appraisal is considered valid for 120 days from its As-Is Date. Once that window expires, the DSCR Lender generally cannot use the report for underwriting unless the appraiser completes an allowed update, typically via the 1004D Appraisal Update/Completion Report, or a full new appraisal.

Two dates appear on most appraisal reports. One is, the “As-Is Date,” which is the effective date of value. This is the date the property’s value opinion applies and is almost always the date the appraiser inspected the property. There will also be an “Appraisal Date,” or “Report Date.” This is the date the report was signed and delivered, which can be days or weeks after the inspection, and is not typically important, only the “As-Is” Date really matters for DSCR Loans. This is because the 120-day validity clock starts from the As-Is Date, not the report date. For example, if the inspection was January 10 and the report was signed January 20, the expiration is still based on January 10.

A recertification of value, often called an “appraisal update,” is when the original appraiser confirms that the property’s market value from the initial report is still accurate as of a new date. For DSCR Loans, this is usually completed on the Fannie Mae Form 1004D (Appraisal Update/Completion Report). One of the most common reasons for a recertification request is when the appraisal identifies more than $2,000 in deferred maintenance, but the repairs are relatively minor, can be completed quickly within the transaction window, and either the seller (for acquisitions) or the borrower (for refinances) is willing to make the fixes. In this case, the appraiser can reinspect and confirm the deferred maintenance has been reduced to $0 or below the $2,000 threshold.

A 1004D may also serve as a completion report to verify that planned repairs or construction noted in the original appraisal are finished, such as if the appraiser’s initial visit to the property occurred while renovations or construction was just finishing up. This is typically not preferred, but can sometimes occur, particularly in cases where the borrower is racing against the refinance clock, for example if there is a soon-expiring construction or rehab hard money loan that must be paid off before maturity.

Note that 1004D Forms are generally not appropriate for “updating” appraisals that expired due to age (i.e. more than 120 days elapsed, and the loan still hasn’t closed yet for whatever reason). In these cases, a brand-new appraisal will likely need to be ordered.

Q: What if the appraisal expires before closing for a DSCR Loan?

A: Most DSCR Lenders consider an appraisal valid for 120 days from the As-Is Date (usually the inspection date). If your closing is delayed past that, the lender may be able to order an appraisal update using a Fannie Mae Form 1004D to confirm the value is still accurate, but if the report is too old or market conditions have changed, a full new appraisal will be required. Either option can add time and cost, so it’s best to close well before the expiration date.

Even with a strict appraisal independence process in place, there are times when a borrower or lender may believe the appraisal’s market value or market rent conclusions are inaccurate. For DSCR Loans, there is usually a formal and compliant way to challenge these conclusions, often called a Reconsideration of Value (ROV) or appraisal rebuttal.

Obviously, if an appraised value comes in lower than expectations, it can throw a DSCR Loan into jeopardy and cause a lot of frustration among everyone involved in the deal. While in many cases, the independent valuation from the appraiser is valid, no matter the hurt feelings – and wallets – of the incentivized parties on the transaction, but there are in fact situations when an appraisal rebuttal may be appropriate. Signs that a rebuttal may actually have a chance to “work” and change an appraiser’s estimates include when the appraised value appears significantly lower than recent comparable sales or contains factual errors about the property’s size, condition or features. Common factual errors that, when discovered, could indicate a true opportunity for a successful rebuttal include incorrect bedroom/bath counts, misreported lot size, missed upgrades, or inaccurate location mapping. Stronger, more recent, or more similar comps that are available but were not used in the report are also a good indicator of appraisal rebuttal success, as these can be sent directly to the appraiser for evaluation, and simply could have been missed.

Because DSCR Lenders follow Appraisal Independence Requirements (AIR), neither the borrower nor the loan officer can directly ask the appraiser to “fix” the value. Instead, the process typically follows a standardized process. It starts with submitting a written request, where the borrower or loan officer (or both, typically together, and potentially with the buyer’s real estate agent if an acquisition) prepare a written request outlining the specific issues, supported by evidence (e.g., MLS sheets, public records, photos, or rental data).

Before going directly to the appraiser, who is likely to be wary of critiques of their work, there will typically be a review process, where the DSCR Lender’s appraisal desk or AMC screens the request to confirm it meets compliance rules and is based on factual support and is not simply a disagreement with the number. Then the request is forwarded to the original appraiser through the AMC for an AMC/Appraiser Review, where appraiser reviews the new information and determines if a revision is warranted. The result is a “Final Decision” where the appraiser (who is still the deciding party, not the AMC, not the DSCR Lender) may: Agree and adjust the value or rent conclusion or decline to change the report, with written rationale.

Q: Can I challenge my DSCR Loan appraisal value or market rent?

A: Yes. Most DSCR Lenders have a formal Reconsideration of Value (ROV) process, sometimes called an appraisal rebuttal, that allows you to request a review of both the market value and market rent conclusions. You’ll need to submit specific, factual evidence such as better comparable sales, more accurate rental comps, or documentation correcting errors in the report. The request goes through the lender or AMC to the original appraiser for review, and changes are only made if the appraiser agrees that the new information supports a revision.

Q: How much does an appraisal cost for a DSCR Loan?

A: For most DSCR Loans, a standard single-family home appraisal costs between $550 and $850, while 2–4 unit properties typically range from $800 to $1,000. Condos often fall in the same range as single-family homes, with an added fee for the condo-specific form. Short-term rentals (STRs), complex properties, or rural locations (where there are fewer available appraisers) can run higher, sometimes more than $1,000, especially if specialized market rent analysis is required. Unlike conventional loans, DSCR Loan appraisals almost always include a 1007 Comparable Rent Schedule or 1025 income report, which can add to the fee, and borrowers nearly always pay this cost upfront before the order is placed.

Q: How long does a DSCR Loan appraisal take?

A: In most markets, a DSCR loan appraisal takes 5–10 business days from order to delivery, but complex properties, rural areas, or high-volume seasons can push this to 2–3 weeks. Delays often occur when tenant or seller schedules limit access, so arranging property entry quickly is one of the best ways to keep your loan on track. It also depends on how “hot” the real estate market is, i.e. when there is lots of transaction activity, the demand for appraisers is high and can outstrip availability, extending this timeline.

Q: Can I talk to the appraiser directly when qualifying for a DSCR Loan?

A: You can provide factual information, like recent upgrades, property features, or access details, but you cannot pressure, suggest a target value, or negotiate the outcome. Any communication should follow your lender’s AMC or AIR policy to preserve appraisal independence.

Q: How much is a rush fee for a DSCR Loan appraisal, and how much faster is it?

A: A typical appraisal rush fee for a DSCR loan runs between $150 and $300 on top of the standard appraisal cost. In most markets, paying for a rush can shorten the timeline by 3 to 5 business days. Rush orders work best when both the inspection and report write-up can be prioritized ahead of other assignments, but they still depend on factors like property access, tenant availability, and how quickly you pay the base and rush fees. Complex properties (2–4 units, short-term rentals, luxury homes) may have higher rush fees, and in peak seasons some appraisers may not offer rush service at all.

Q: Can I give the appraiser my purchase contract and renovation receipts?

A: Absolutely. While you can’t pressure the appraiser to hit a certain value, providing factual documents like your executed contract, scope of work, and proof of upgrades ensures they have complete information to evaluate the property accurately.

Q: Do DSCR Lenders ever waive appraisals?

A: No. DSCR loans always require a full appraisal (and sometimes even two appraisals for high balance loans); automated valuation models (AVMs) or “appraisal waivers” used in some conventional loans are not accepted by any mainstream DSCR Lender.

Q: Can I use my own appraiser for a DSCR Loan?

A: No. While federal appraisal rules for owner-occupied loans don’t technically apply to DSCR investment property loans, industry standard still requires lenders to follow strict appraisal independence practices. This means you cannot select or pay your own appraiser for the loan’s collateral valuation, the lender must order it through an Appraisal Management Company (AMC) or approved independent panel to ensure the valuation is unbiased and accepted by secondary market investors.

Q: What is the 1004D form in a DSCR Loan appraisal?

A: The Fannie Mae Form 1004D, also called the Appraisal Update and/or Completion Report, is used by the original appraiser to either (1) confirm that the value from the initial appraisal is still valid as of a new date, or (2) verify that planned repairs or construction have been completed. In DSCR lending, a 1004D update can sometimes be used if you’re still within the appraisal’s 120-day validity window and need to extend it to closing. However, if the appraisal has expired or the market has shifted, most DSCR Lenders will require a full new appraisal instead.

Q: Who owns the appraisal report in a DSCR Loan?

A: Even though you pay for the appraisal, the report is legally owned by the lender who ordered it, because they are the appraiser’s client and the intended user named in the report. That means you can’t take the same report and use it with another lender without a formal transfer or re-address. However, federal law requires your lender to give you a copy of the appraisal and most other valuation reports they use to make their decision, usually within three business days of receiving it or at least three business days before closing.

Up Next: Appraisal Reviews (CDAs) and Field Reviews for DSCR Loans

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.