.png)

.png)

Accessory Dwelling Units (ADUs) are rapidly growing in popularity across residential real estate and are becoming an increasingly important strategy for real estate investors. An ADU, sometimes referred to as an accessory apartment, casita, or in-law suite, is a smaller, secondary dwelling located on the same parcel as a primary single-family home. According to conventional definitions (e.g. Fannie Mae), a qualifying ADU is a self-contained unit with its own 1) Private Entrance (ingress/egress) 2) Kitchen (sink with running water, cabinets, working stove or hookup), 3) Sleeping Area and 4) Bathroom (including shower facilities). To qualify as a true ADU, the secondary unit must also be subordinate in size to the main home and offer independent access and functionality.

There has been a recent surge in ADU adoption, likely driven by two key forces: housing shortages in high-growth and land-constrained metro areas (e.g. Austin, Texas and Los Angeles, California) and stubbornly high home prices and interest rates, which make every incremental dollar of rental income more valuable to investors seeking positive cash flow and stronger returns

DSCR Loans are well-positioned to support this evolving strategy. Unlike conventional lenders bound by rigid agency underwriting (Fannie Mae, Freddie Mac), many DSCR lenders adapt more quickly to investor needs, especially for newer and emerging strategies such as single-family homes with ADUs. Most DSCR Lenders allow financing for single-family residences (SFRs) with one legal ADU. However, properties with multiple ADUs, or 2–4 unit buildings with an added ADU, are typically ineligible for DSCR Loans.

Where DSCR Lenders vary significantly is in how the ADU is treated during qualification and underwriting, particularly in the specific methodology used to calculate key metrics such as the DSCR and LTV ratios as well as property type classification (i.e. SFR or Duplex), all of which can significantly affect eligibility, qualification and pricing (i.e. rates and terms).

Generally, a property with two full units, one a main residence and one an ADU, will actually be treated as a Single-Family Residence (SFR) and not a duplex (i.e. two-unit) for DSCR Loan qualification purposes. Even if the property is rented out to multiple tenants under multiple leases, investors can access DSCR Loan terms based on SFRs, which have the most favorable loan terms, including lowest rates and highest leverage limits.

There are however, a few rare exceptions where a DSCR Lender may classify a property with an ADU as a 2-unit instead of an SFR. This typically occurs if the property has a separate legal postal address, independent utility meters and a formal zoning reclassification by the municipality. However, these are uncommon, and in the vast majority of cases, the property will be classified as an SFR by DSCR Lenders.

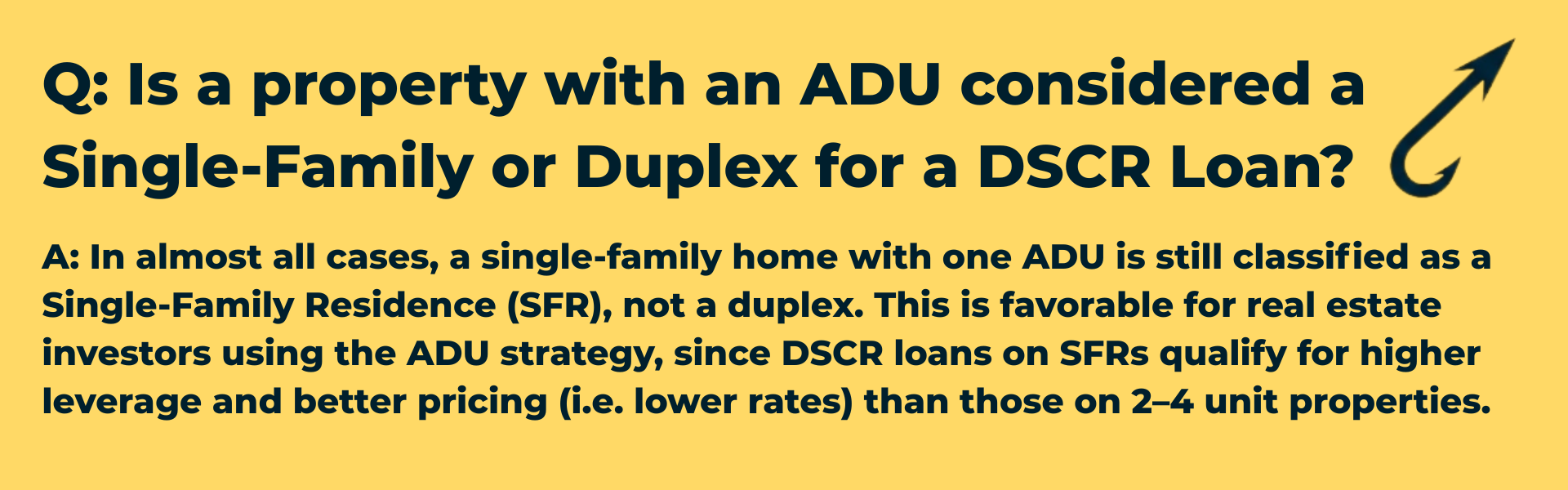

Q: Is a property with an ADU considered a Single-Family or Duplex for a DSCR Loan?

A: In almost all cases, a single-family home with one ADU is still classified as a Single-Family Residence (SFR), not a duplex. This is favorable for real estate investors using the ADU strategy, since DSCR loans on SFRs qualify for higher leverage and better pricing (i.e. lower rates) than those on 2–4 unit properties.

The valuation, or the applicable value utilized in the all-important LTV ratio calculation, is a crucial aspect of DSCR Loan qualification, and is the primarily determinant of the total loan amount and leverage available to investors. Many investors targeting properties with ADUs likely need the value of the ADU to “count” in terms of qualification and underwriting by DSCR Lenders to secure the DSCR Loan terms available, so it becomes a crucial question for ADU investors seeking financing.

Generally, for an ADU to be included in the valuation DSCR Loan qualification, the ADU must be permitted, the design and location of the ADU must be consistent with neighborhood norms and the appraiser must use local comparable sales that include similar ADU configurations. If the ADU is unpermitted, it may still be allowed on the property (i.e. not preclude eligibility), but its value will not be counted in the LTV ratio and for DSCR Loan qualification purposes.

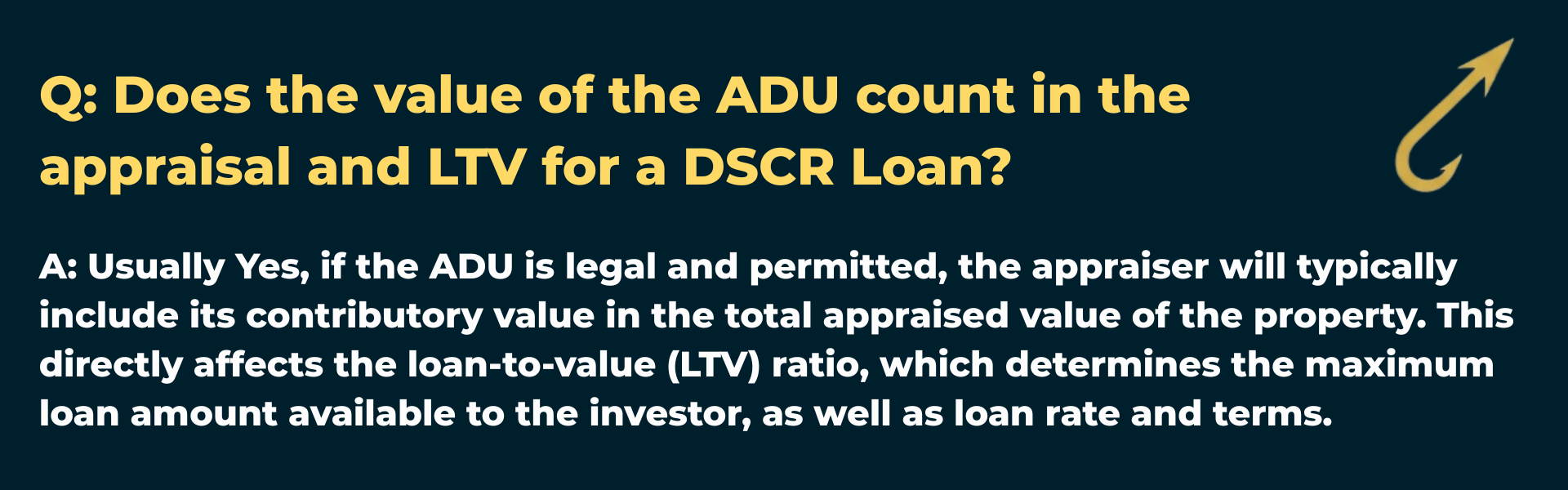

Q: Does the value of the ADU count in the appraisal and LTV for a DSCR Loan?

A: Usually Yes, if the ADU is legal and permitted, the appraiser will typically include its contributory value in the total appraised value of the property. This directly affects the loan-to-value (LTV) ratio, which determines the maximum loan amount available to the investor, as well as loan rate and terms.

The property’s rental income, or the numerator used in the important DSCR ratio, is also an important consideration for properties containing ADUs. Specifically, whether or not the rents from the ADU, whether from an in-place lease or STR operating history or market rent projection, will “count” in the DSCR ratio calculation. The good news for investors is that generally the rents from ADU units will be counted by DSCR Lenders if the ADU unit is properly permitted, with similar requirements to use the ADU’s value in the LTV ratio calculation.

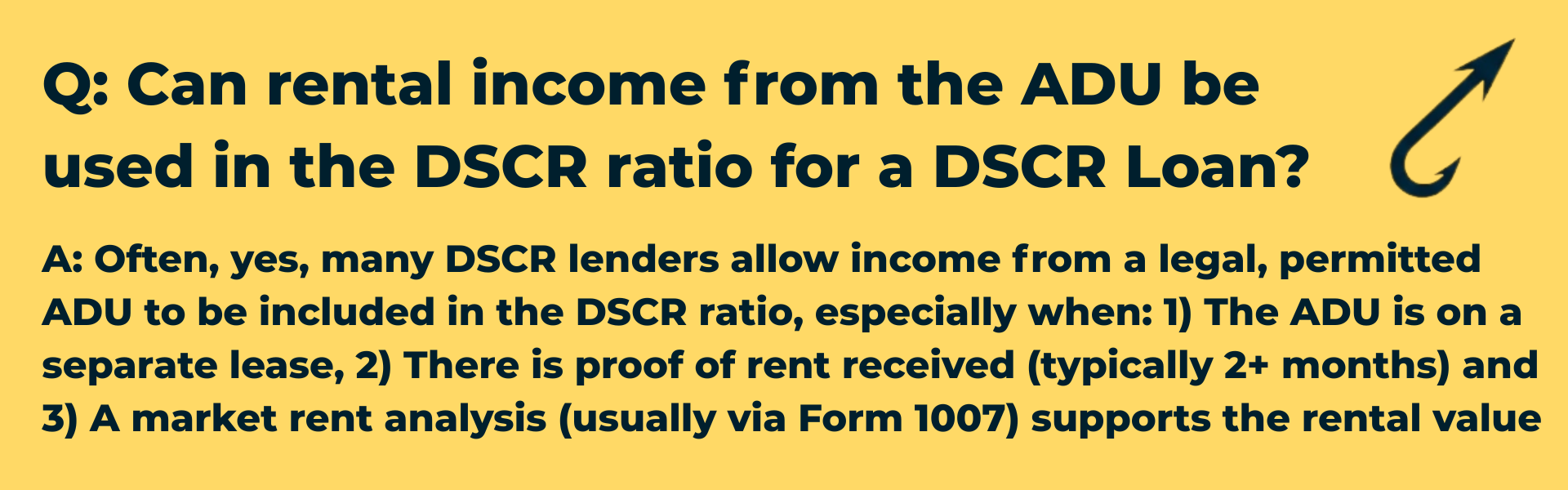

Q: Can rental income from the ADU be used in the DSCR ratio for a DSCR Loan?

A: Often, yes, many DSCR lenders allow income from a legal, permitted ADU to be included in the DSCR ratio, especially when: 1) The ADU is on a separate lease, 2) There is proof of rent received (typically 2+ months) and 3) A market rent analysis (usually via Form 1007) supports the rental value

If an ADU doesn’t have all proper permitting, many investors are surprised (and delighted) to learn that the properties are likely still eligible for DSCR Loans. In these cases, most DSCR Lenders will qualify and underwrite the loan as if the ADU doesn't exist, solely evaluating and qualifying the property based on the primary residence on the parcel. That said, ADU eligibility and treatment still vary significantly across DSCR Lenders. Investors considering this strategy should review the lender’s specific policies and treatments as well as any local regulations or requirement wrinkles that may lead a DSCR Lender to evaluate a property with an ADU differently.

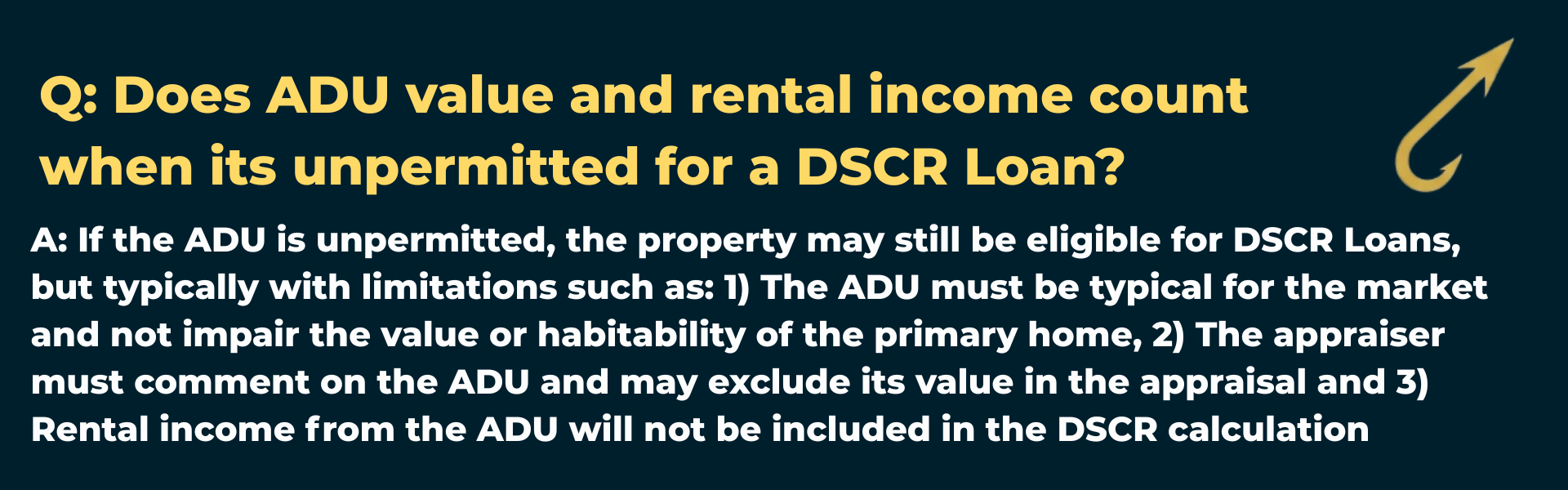

Q: Does ADU value and rental income count when its unpermitted for a DSCR Loan?

A: If the ADU is unpermitted, the property may still be eligible for DSCR Loans, but typically with limitations such as: 1) The ADU must be typical for the market and not impair the value or habitability of the primary home, 2) The appraiser must comment on the ADU and may exclude its value in the appraisal and 3) Rental income from the ADU will not be included in the DSCR calculation

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.