.png)

While FICO, LTV, and DSCR are the three core inputs most directly tied to your DSCR loan pricing, they aren’t the only ones. Once those primary risk-based metrics are determined, DSCR Lenders apply additional pricing considerations that include what are known as “Loan-Level Price Adjustments (LLPAs)” and “Overlays. These adjustments can also significantly impact a rate and/or fees and understanding them is essential for optimizing DSCR Loan terms.

In this section, we’ll explore six key non-core pricing factors:

Each of these elements can also significantly influence the final rate and terms. Also, importantly, they can be adjusted in most cases based on investor preferences. That flexibility is one of the reasons DSCR Loans are such a powerful tool for scaling a real estate portfolio.

Believe it or not, the purpose of a DSCR loan - whether it’s an acquisition or refinance (and within refinances, whether it’s a cash-out refinance or rate-term refinance) can have a meaningful impact on the rate and fees offered. But why does the lender care why a borrower is borrowing?

The answer has less to do with intent and more to do with valuation certainty, specifically, how confident the lender is in the accuracy of the property’s market value. That value forms the denominator of the all-important Loan-to-Value (LTV) ratio, which is arguably the most important pricing factor.

Essentially, the more confident the DSCR Lender is in the appraised market value, i.e. the price the property would reasonably sell for in an open market, the more friendly they can be with pricing (i.e. loan terms). Conversely, if the value may be inflated or is more difficult to validate, lenders will adjust pricing upward (i.e. higher rates and/or fees) to compensate for the increased risk.

This is why DSCR Loans for acquisitions tend to have the best pricing. Since DSCR Acquisition Loans are by definition loans in a transaction where a seller is presumably selling a property to the highest bidder on the open market (a pure “market value”), the lender has the highest confidence in the market value, or “V” in the LTV calculation. Caveats aside (such as over- or under-market deals or fraudulent sales), the vast majority of acquisition transactions will more or less substantiate the market value through the transaction itself, allowing the lender to have top confidence in the value of the property they are financing (and their evaluated LTV ratio). Because of this, not only will acquisitions tend to have the lowest rates and fees for DSCR Loans, they will always be eligible for the maximum leverage options the DSCR Lender has to offer (i.e. highest LTV limits).

Conversely, refinances have worse pricing because the valuation is based on an appraiser estimate since no market transaction is happening (there are no buyers or sellers), so the value is less certain. While DSCR Lenders have robust processes and methodologies to estimate value for refinance loans through independent appraisers and secondary valuation reviews (including typically both internally and through a third party), nothing quite emulates market value like a live-market sale that occurs in acquisition transactions. For this reason, refinances tend to have worse pricing (higher rates / fees) than acquisitions.

Further, cash-out refinances tend to have worse rates and terms than both acquisitions and rate-term refinances. In addition to higher rates and/or fees, cash-out refinances will typically have lower LTV limits (such as 5% to 10% lower maximums than DSCR Loans for otherwise equivalent acquisition or rate-term refinances) as well as other restrictions such as seasoning requirements.

However, many investors tend to ask: Why do cash-out refinances have worse rates and loan terms than rate-term refinances when valuation methodology is the same?

At first glance, this doesn’t appear to make much sense, since whether the investor walks away with cash or not shouldn’t seem to have an effect on terms if everything else is the same – same value, same credit score, same valuation methodology, etc. The answer is, chiefly, lender fraud-avoidance, investor psychology and data from past performance.

First, fraud avoidance: the sad fact is that real estate investing does attract many dishonest actors who attempt to utilize the industry for ill-gotten gains though fraud. And lenders, including DSCR Lenders, are common targets. One of the typical ways that fraudsters in real estate will target lenders is through attempting to access cash through fraudulent cash-out refinances, where the value of a property is significantly overstated so a loan – and cold, hard cash – is gained on a property when true value is less than the money extended. In these cases, the fraudulent “investor” can walk away with the cash and the lender has no recourse through foreclosure, since the true market value is less than the cash that has already walked out the door. Without going into the details of how these schemes can occur, cash-out refinances are a preferred method for real estate fraud, as opposed to rate-term refinances where the borrower doesn’t actually access any cash to walk away with). More conservative terms for cash-out refinances are a defense DSCR Lenders use to counteract this type of mortgage fraud.

Second, investor psychology matters. When an investor pulls cash out of a deal, it subtly shifts the nature of the investment from "equity skin in the game" to "house money." Lenders know that borrowers with substantial equity tend to behave more conservatively and are more likely to fight to protect their investment. Conversely, when equity is reduced, especially through a cash-out, borrowers have less at stake, and that correlates to higher rates of delinquency, default, and foreclosure in historic data sets. While logically, it shouldn’t matter if the equity in the property is “house money” or not (like in a rate-term refinance), humans aren’t totally logical, and real estate investors are no exception (until perhaps AI investors take over the market, but that is a question for DSCR Lenders in the future). Psychology is another reason why cash-out refinances have worse pricing and more restrictions.

Lastly, there’s data-driven performance history. DSCR Lenders (and the secondary market investors who ultimately buy these loans) have years of performance data, and the numbers are consistent: cash-out refinance loans default more often than purchases or rate-and-term refis, even when borrower credit, DSCR ratios and other risk factors are identical. This isn’t just theory, it’s actuarial reality, measured extensively by bond investors and rating agencies that track these loans closely. So even if a particular cash-out refinance is perfectly clean on paper, it’s being priced in a system that has learned (sometimes the hard way) to treat cash-out scenarios as a higher-risk class.

All that being said, the pricing isn’t actually that much worse for cash-out refinances versus acquisitions or rate-term refinances. Typically, it will be an interest rate of 0.25% or 0.50% higher and/or a slightly higher closing fee. The biggest difference would be reduced loan term options, chiefly lower LTV maximums and seasoning requirements (or a minimum number of months of ownership required prior to being able to do a cash-out refinance). Generally, the LTV maximums will be 5-10% lower for cash-out refinances depending on the situation; which while not a huge “pricing hit” (i.e. interest rate or fees), lower LTVs can be less than ideal for high-leverage minded investors. At the end of the day, the biggest reason DSCR Lenders penalize cash-out refinances is fraud avoidance and the pairing of potential fraud with overstated value, so LTV limits are the main response.

Loan size plays a surprisingly important role in DSCR loan pricing. DSCR Lenders also care quite a bit about the amount of the loan. Most DSCR Lenders have a defined “sweet spot” when it comes to loan size where the best rates and terms lie. Like the famous Goldilocks and the Three Bears fable, the ideal loan size for DSCR Lenders is typically between the extremes, not too big and not too small.

On the lower end of the spectrum, very small loans, like those under $125,000, can have higher rates and fees, even when the property and borrower profile are strong. The reason is largely economic: the fixed costs associated with originating and closing a loan (appraisals, underwriting, legal, title, servicing setup) don’t scale well on smaller balances. From the lender’s point of view, a $95,000 loan takes nearly as much effort to close as a $500,000 loan, but with far less margin (especially since closing fees typically represent a percentage of the loan amount, so on small loans, that’s a small number comparatively). As a result, most DSCR Lenders set a minimum loan size of $100,000, and only a small handful go lower, occasionally to $75,000 or in rare cases even $55,000, usually in markets where property prices are significantly lower. These smaller loans may also be viewed as higher risk as they can signal ultra-rural markets, distressed assets, or economically challenged neighborhoods.

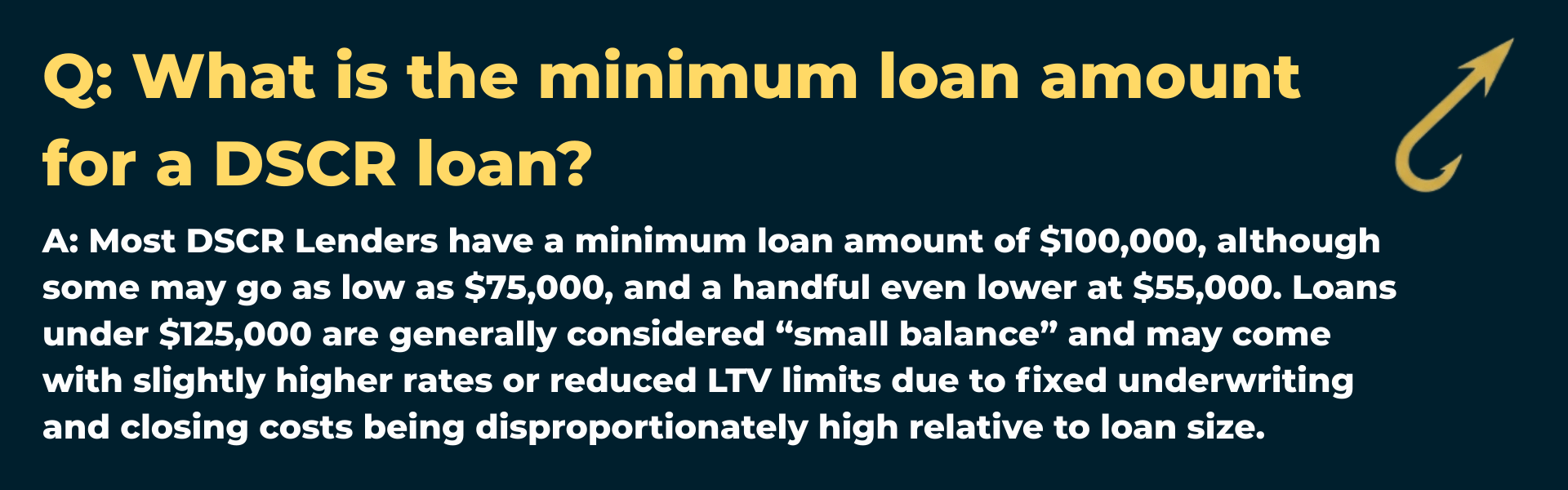

Q: What is the minimum loan amount for a DSCR loan?

A: Most DSCR Lenders have a minimum loan amount of $100,000, although some may go as low as $75,000, and a handful even lower at $55,000. Loans under $125,000 are generally considered “small balance” and may come with slightly higher rates or reduced LTV limits due to fixed underwriting and closing costs being disproportionately high relative to loan size.

On the flip side, very large loans, typically over $1.5 to $2 million, can also lead to worse pricing, but for an entirely different reason: market depth. There simply aren’t as many people who can afford to pay $10,000+ per month in rent, and even fewer who would choose to rent rather than buy if they could afford these rental rates! From a DSCR Lender’s perspective, this creates two layers of risk. First, if the borrower defaults, the property may sit longer on the market or sell for a steeper discount because of the limited buyer pool. Second, during regular operations, finding qualified renters at the needed rent levels can be much harder, and vacancies may take longer to fill. For these reasons, some DSCR Lenders cap their max loan size around $2,500,000, and DSCR Loans with original balances north of about $1,500,000 often come with higher rates and/or fees as well as lower leverage limits (i.e. LTV maximums) and other restrictions.

The ideal loan amount range for most DSCR Lenders falls between $250,000 and $750,000. Loans with these amounts strike the best balance of risk and liquidity. If a default or foreclosure were to occur, properties in this price band are the most marketable, i.e. there’s a much larger pool of potential buyers actively shopping in this segment, which improves recovery prospects in case of foreclosure. On the rental side, properties at these values also align with market rents affordable to a wider range of tenants, meaning the lender has greater confidence that the property will stay leased, the DSCR ratio will remain positive and monthly payments will be made.

If a DSCR Loan falls outside this range, either significantly smaller or larger, it’s still eligible with most DSCR Lenders. While it will have only slightly worse pricing, typically around 0.25% higher in rate, there will typically be much tighter LTV restrictions, similar to the treatment of cash-out refinances. In many cases, that means a maximum LTV that’s 5–10% lower than what would be allowed for a moderate-sized loan with otherwise identical terms.

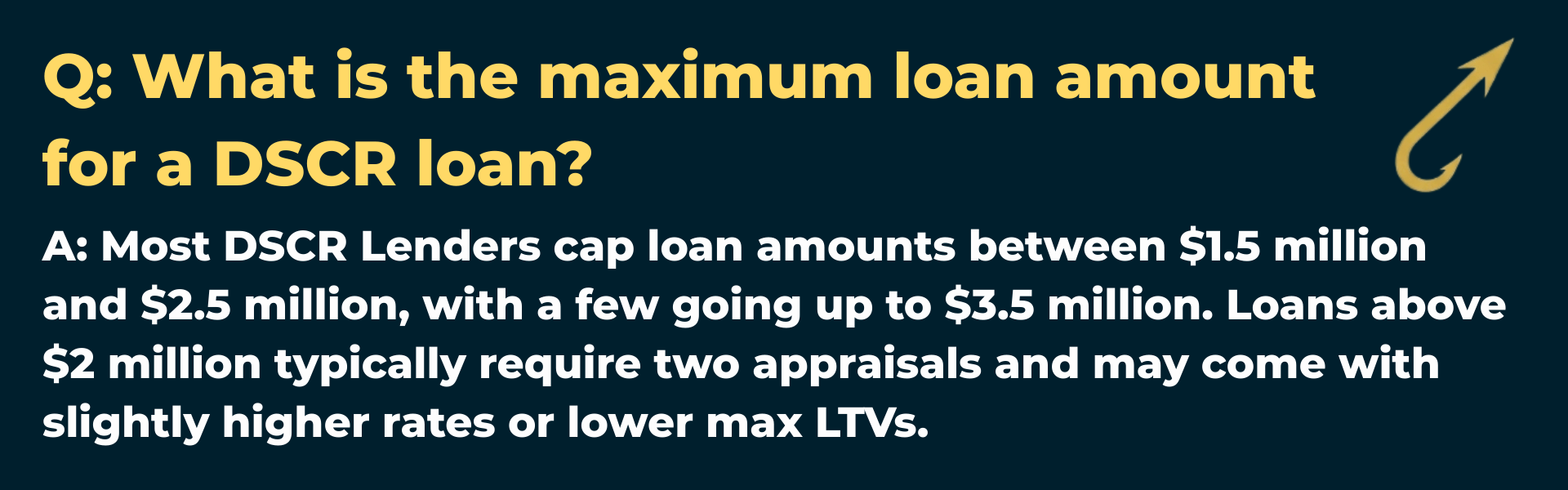

Q: What is the maximum loan amount for a DSCR loan?

A: Most DSCR Lenders cap loan amounts between $1.5 million and $2.5 million, with a few going up to $3.5 million. Loans above $2 million typically require two appraisals and may come with slightly higher rates or lower max LTVs.

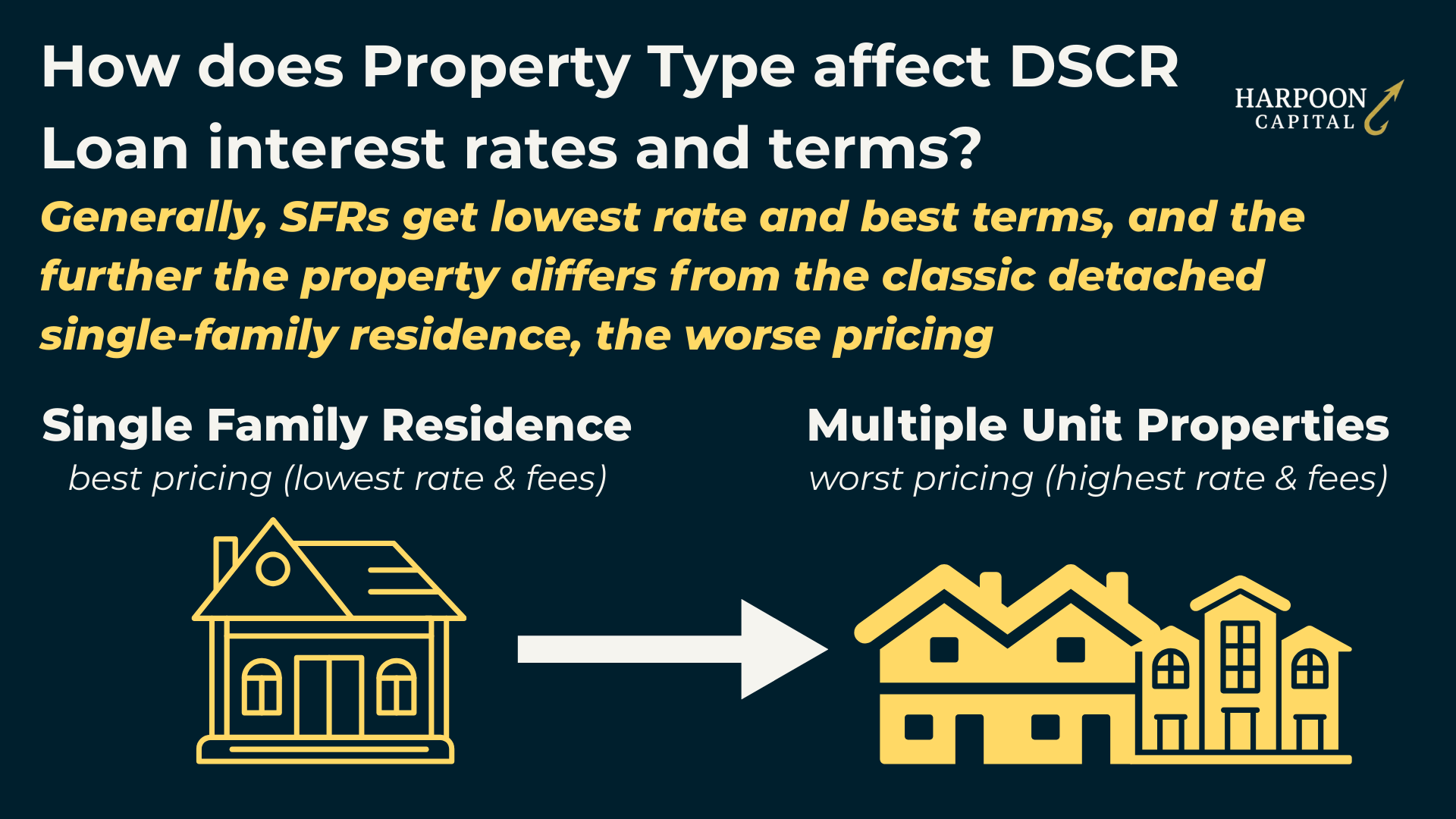

Another important factor that affects DSCR Loan pricing is the property type. At a high level, the primary risk for the lender: how easily the property could be resold if the borrower defaults and foreclosure is necessary and the type of property securing the DSCR Loan can significantly affects this area of risk.

Standard single-family residences (SFRs) are priced most favorably for DSCR Loans (i.e. lowest rates and least restrictions). These are the most common and easily valued type of residential property. SFRs have the most robust market values because they have by far the largest potential pool of buyers among all DSCR Loan-eligible property types by far. The number of people that are interested (and qualified) to buy a single-family residence includes the vast majority of the overall property buying market: people intending to occupy the property. This segment of buyer dwarfs the size of the market of people who are looking for a strict rental, even if buyers that are “house hackers” (or people open to living in one unit and renting the other) or “second home searchers” (or people that plan to use properties as part-time personal usage and part-time STR) are added. For this reason, DSCR Loans on SFRs get the best rates and terms, and DSCR Loans secured by multi-unit properties or condos have slightly higher rates and minor LTV restrictions, although the differences aren’t too significant.

DSCR Loans secured by condo units also get slightly worse rates and terms than loans secured by single family residences for the same reason: generally, there is a much larger market for detached SFRs than condo units within buildings. Part of this is just buyer preference because many people want access to a full house with a yard and extra space versus shared living in a condo. Condos also compete with a larger rental apartment market, i.e. those that would be interested in buying a condo would also be more open to renting a nice apartment unit. But condos also come with higher risks too, since the individual unit is dependent on other owners and the HOA to make sure that parts of the building don’t go into disrepair or run into other problems, which can significantly affect the value and marketability of the individual unit. These reasons, primarily the latter, cause DSCR Loans on condos to be higher-risk for the lender, and priced accordingly (with higher rates and/or fees) as well as potentially some LTV or other loan structure restrictions.

The logic continues “up the spectrum,” with worse pricing (rates and terms) and more potential restrictions (i.e. LTV maximums) for DSCR Loans secured by properties the further it differs from the classic detached single-family residence. Triplexes and Quadruplexes for example, can sometimes carry worse pricing than duplexes because the potential buyers’ market shrinks, i.e. there are more people interested in two-unit duplexes that have more options for house hacking or to get a fully separate guest suite for non-rental purposes like au pairs or extended family; when entering three-plus unit territory, these properties are truly only suitable for investors interested and willing to become committed landlords, which is definitely a smaller pool.

This logic continues for multifamily (5+ unit) and mixed-use properties. When properties pass four units and include actual commercial tenants (with a whole additional set of needs and wrinkles), this shrinks the buyer pool even further with valuations based on a completely different set of metrics and methodology. This is why Multifamily DSCR Loans and Mixed Use DSCR Loans have by far the highest rates and fees among DSCR Loans and come with much lower LTV maximums and other requirements such as high DSCR ratios and low or no vacancies.

While property type is well-established in DSCR Loan pricing, property location and usage also play a meaningful role in how some DSCR Lenders evaluate risk and set terms. These adjustments are less universally applied, but when present, they can lead to notable differences in both interest rates and fees and LTV limits.

Properties located in rural areas or declining markets are a common example. Even if the property itself is a standard single-family home, lenders may apply more conservative underwriting due to limited market depth. Fewer potential buyers in the area means the property could take longer to sell in the event of a default, which increases the DSCR Lender’s risk exposure. To mitigate that risk, some lenders will impose a lower maximum LTV, often capped at 65.0% or 70.0%, and in some cases apply minorly increased rates like 0.25% to 0.50% higher compared to an identical property in a more liquid suburban or urban market.

Another key driver of pricing differences is whether the property is intended for short-term rental (STR) use. Even in stable metro areas, STRs are viewed differently from long-term rentals because the projected income stream is more variable and sensitive to seasonality, guest reviews, local regulations, and operator performance. Additionally, properties used as STRs are often subject to heavier wear-and-tear, and may appeal to a narrower buyer pool, particularly if they’re optimized for hospitality rather than traditional tenancy. As a result, lenders may apply higher rates (ranging from minor, like 0.25% to significant, like 1.00% or more depending on how “STR-friendly” the lender is) or reduced LTV ceilings to STR-backed loans, especially for ones secured by properties in non-core vacation markets where the use case is less established.

Importantly, these property location or usage pricing differences are not always disclosed up front or listed on DSCR Lender rate sheets or program marketing. Some DSCR Lenders may only apply them under certain conditions (e.g., low DSCR ratios, borderline credit, or higher leverage), while others build them directly into their baseline terms for rural or STR properties. For investors operating in these categories, it’s worth proactively asking about location- and use-based pricing adjustments during the quote stage. particularly if comparing DSCR Lenders or needing to structure a deal close to max LTV thresholds.

Even real estate investors with experience buying and refinancing rentals and the different financing strategies available can be surprised to learn how impactful prepayment penalty provisions can be for DSCR Loan pricing and their significant effect on interest rates.

In short: the longer and stronger the prepayment penalty, the better the pricing. That’s because lenders (and the institutional investors who ultimately buy the loans) place a high value on predictable, stable interest income. Without any prepay protection, borrowers would have a one-sided advantage: they could refinance anytime rates drop, instantly lowering monthly payments and long-term interest costs, while also having the ability to hold the loan indefinitely if rates rise. In that scenario, the lender (or more accurately, the investor buying the loan) takes on all the downside and none of the upside. If market rates fall, note holders lose yield as loans refinance early. If market rates rise, borrowers sit tight with below-market rates, locking in cheap debt for 30 years while the holder of the loan is stuck earning less than the new going rate.

Prepayment penalties give note holders the assurance that, even if rates fall and borrowers refinance early, they will recoup a portion of the lost return immediately—via the prepayment fee. In essence, prepayment penalties make the economics work for everyone involved. They give borrowers access to better rates and lower monthly payments, while protecting the institutions that own these loans from getting blindsided when market conditions change. And that’s exactly why lenders are willing to offer significantly lower rates in exchange for a few years of prepay protection: it keeps the system balanced.

How much lower? Depending on the structure, a prepay penalty can lower the interest rate on a DSCR Loan by as much as 1% or in some cases, even more! For example, a DSCR lender’s pricing may give the following quotes for a loan with everything the same except for the following prepayment penalty options.

These massive differences (and often borrower flexibility to pick and choose based on their needs) is one of the reasons many investors love DSCR Loans as they can participate in the tailoring of loan provisions to their needs (and a reason that states that restrict this flexibility misguidedly aren’t doing people favors with regulation).

And that rate difference translates directly into significant monthly savings. On an average-sized $400,000 DSCR loan (30-year fixed, fully amortizing):

That’s nearly $270/month in savings, or over $16,000 in the first five years alone—just for agreeing not to refinance or sell too soon (or even if prepaid early, paying a fee no more than 5% - which could be matched or even exceeded by future savings or gains from appreciation).

Prepayment penalties are a mix and match of duration (how long the prepayment period is, usually one to five years, or covering the first 12 payments to a max of the first 60 payments due) and fee (generally ranging from 1% to 5%). Options that are heavy on fee but short on duration (like 5% for 2 years) can be equivalent or similar to options that are long but carry lower, descending fees (like a Descending 4/3/2/1 structure). The chart below shows what an example $400,000 Fully Amortizing DSCR Loan might look like with an average lender depending on what prepayment structure is added:

As shown above, more protective structures (like the “5/5/5/5/5” or “5/4/3/2/1”) provide the lowest rates and payments, while shorter or looser penalties (such as “2/1” or “1 Year, 6 Mo. Interest”) have smaller pricing advantages. A loan with no prepay protection at all will nearly always carry the highest rate, and thus the highest monthly payment.

For most real estate investors planning to hold for the long term, accepting a prepay penalty is a strategic advantage, not a liability. And even if rates fall in the near term, the small penalty (typically 1–5% of the balance) is often outweighed by the rate savings and property appreciation, making a quick refinance still worth doing.

In short, if not planning to exit in the first 2–5 years of a loan term, a prepay penalty is one of the most efficient tools available to lower DSCR Loan rates and costs without giving up anything that impacts a long-term buy and hold strategy.

%20on%20DSCR%20Loan%20Pricing.png)

Another important pricing lever in DSCR lending is the choice between a Fully Amortizing loan and a Partial Interest-Only (IO) structure. While interest-only options are familiar to many investors from commercial or bridge financing, they’re often overlooked in DSCR Loans, even though they can be a powerful tool to improve monthly cash flow.

Here’s the tradeoff: choosing a Partial-IO structure (usually 10 years of interest-only payments before fully amortizing for the remaining 20 years) typically comes with a higher interest rate—but a lower monthly payment. That may seem counterintuitive at first, but it makes sense once you understand the math: in the IO period, only interest is due, not principal, so even with a slightly higher rate, the monthly obligation is lower.

From a pricing standpoint, the difference is modest but meaningful:

Still, the result is often a lower monthly payment overall. Also importantly, DSCR ratios are calculated based on the lower initial IO payment, so a pricing penalty for choosing a Partial-IO option may even be offset by moving into a higher DSCR ratio “bucket”!

Take a look at the difference in payments on $400,000 DSCR Loan. If structured to be Fully Amortizing with a rate of 6.875%, the loan will have a monthly payment of $2,628 for the first ten years of the term, while that same DSCR Loan, but with the Partial-IO structure utilized and thus a slightly higher 7.125% interest rate, will have a monthly payment of $2,375, a greater than $250 per month cash flow improvement, despite a higher interest rate!

It’s also worth noting that almost all DSCR loans are refinanced or paid off well before 10 years, or when a typical interest-only period would end. Since most DSCR loans include some form of prepayment penalty for the first 3–5 years, investors typically refinance around years five through ten. So while the loan technically shifts to amortizing after 10 years, few investors ever reach this point and thus never even end up paying any elevated amortizing monthly payments!

In short, Partial-IO structures are a smart tool for cash flow-focused investors. While the interest rate is slightly higher, the payment is lower, the DSCR ratio looks stronger and the long-term downside rarely materializes. For the right investor profile, that’s a pricing tradeoff well worth making.

Another structural feature that can influence DSCR loan pricing is the rate type—specifically, whether the loan is a 30-year fixed rate or a Hybrid (Fixed to ARM) structure. While adjustable-rate products may sound like a relic from the subprime days, they are still used today in DSCR lending—but their benefits are more limited than many investors expect.

Most Hybrid (Fixed to ARM) DSCR loans are structured with a fixed rate period (usually 5, 7, or 10 years) followed by an annual rate reset tied to an index, like SOFR, plus a margin. These loans almost always include a rate floor—meaning the rate can’t go lower than the original starting point, only higher.

From a pricing standpoint, Hybrid (Fixed to ARM) structures do typically carry a slightly lower rate, but not by much. In 2025’s environment, the difference is usually only about 0.125%, such as a rate of 6.750% versus a fully fixed rate of 6.875% for the same deal. For most investors, that tiny reduction isn't worth the added complexity and potential future risk, especially when fixed rates offer cost certainty and insulation from market movement.

That said, in a tough deal where every basis point matters, or for highly experienced borrowers who understand the mechanics of rate floors, index caps, and adjustment margins, the Hybrid (Fixed to ARM) complexity can be worth it, particularly if they’re confident they’ll refinance or exit within the fixed period.

For most DSCR investors though, the current benefit is small, the upside is capped, and the risk of future rate hikes is real. Unless especially comfortable modeling complex rate movements, a simple fixed-rate structure is usually the safer and more strategic choice for most investors, however the benefits of this structure may become more significant in future years, especially if interest rates move back down to historically low levels.

There are a handful of other factors that can affect the rates and terms on DSCR Loans. These factors, similar to property market or usage (rural, declining market or STR vs. LTR as covered above), may have a small effect on pricing, but typically these factors affect eligibility and loan restrictions such as LTV maximums or DSCR minimums rather than increased rate.

The most important additional factor that could significantly affect your rate and terms are significant credit report issues such as recent credit events like bankruptcies, foreclosures, short-sales or deed-in-lieus or mortgage lates (30+ day payments on real estate-related debt in the last couple years). While these events may not be a kiss of death in terms of eligibility (investors can still sometimes qualify for a DSCR Loan with these significant credit issues!), the DSCR Loans available will likely have significantly higher rates and/or closing fees and heavy LTV, FICO and DSCR restrictions. That being said, access to credit for real estate investing, even at unfavorable terms, can be invaluable for real estate investors working their way back from problems in the past and DSCR Loans can be an option when most other financing avenues are closed off.

Finally, believe it or not, agreeing to have the lender and their servicer handle property tax and insurance payments through escrows and monthly payments automatically drawn via ACH can both get you a lower rate on a DSCR Loan. While some DSCR Lenders will make these optional (i.e. allow borrowers to handle these themselves), the vast majority of borrowers will either choose (or be required through lender policy) to have these taken care of. DSCR Loans with these automatically handled by servicing will also have the bonus of slightly lower rate or fees, but likely around only 0.125% or .25% lower in rate, but hey, that counts and adds up!

Read Next: We peel back the curtain and reveal how a DSCR Lender will generate a set of quotes based on your DSCR Loan scenario with a comprehensive scenario!

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.